Europe’s solar procurement market in 2026 is unlike anything the industry has navigated before. The Chinese module price crash of 2023–2024 — which saw module spot prices fall from over €0.30/Wp to below €0.15/Wp at peak oversupply — created a market where low headline prices coexist with genuine operational complexity. Installers and EPCs are caught between bargain-level module costs and a supply chain that has become harder, not easier, to manage.

The challenge is no longer simply “where do I source modules.” It is: Which manufacturer tiers actually ship on time? Which distributors are financially stable enough to honor forward contracts? What happens to my BOM when a component goes out of stock mid-project? How do I stay compliant with IEC 61215, CE, and MCS certifications across multiple EU markets simultaneously? And how do I avoid locking in €/Wp prices three months before delivery when the euro-dollar rate can move 8% in a quarter?

This guide addresses every layer of European solar procurement in 2026: module price benchmarks by tier, lead time data by equipment category, EU anti-dumping considerations, stocking strategies, quality certification requirements, preferred distributors, inventory financing, and how accurate solar design software reduces the BOM errors and specification drift that quietly inflate procurement costs on every project.

TL;DR — European Solar Procurement 2026

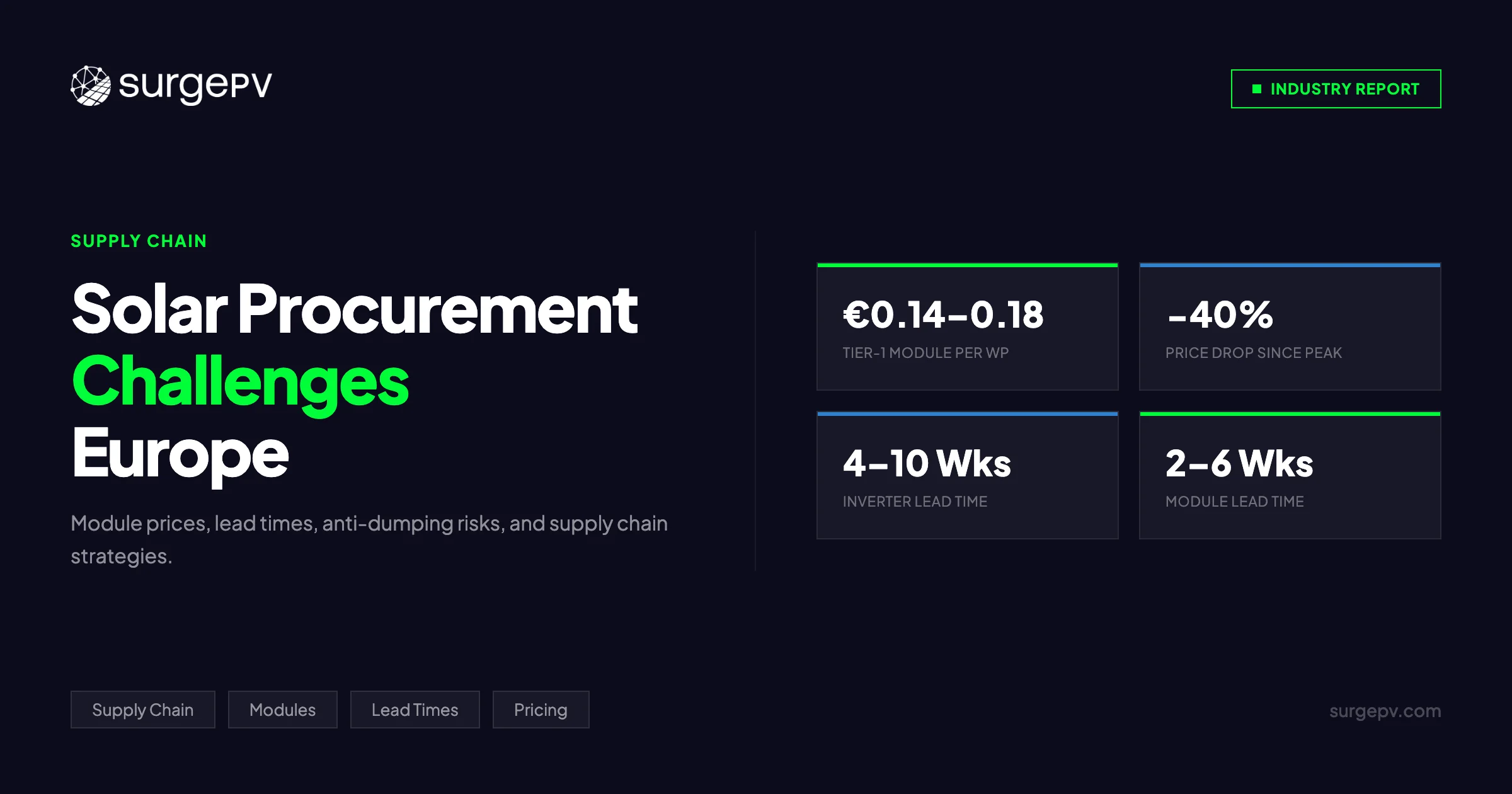

Tier-1 module spot prices: €0.14–€0.18/Wp ex-warehouse (large volume). Small EPC effective cost: €0.21–€0.28/Wp. Module lead times: 2–6 weeks. String inverter lead times: 4–10 weeks. Mounting system lead times: 2–5 weeks. EU anti-dumping decision pending — price floor risk exists for Chinese modules. IEC 61215 and CE marking are non-negotiable for grid connection. Accurate BOM generation from design software is the highest-ROI procurement improvement available to mid-size EPCs.

In this guide:

- Latest 2026 European solar supply chain data — module price table, lead times by category

- Module price trends in Europe by manufacturer tier (€/Wp benchmarks)

- EU anti-dumping policy and the price floor risk

- Lead times: modules vs. inverters vs. mounting vs. BOS components

- Warehouse and stocking strategies for European EPCs

- Quality certification requirements: IEC 61215, CE, MCS, TÜV

- Preferred European distributors and their procurement models

- Financing procurement: inventory finance and supplier credit terms

- How accurate BOM software reduces procurement waste and redesign costs

- Supply chain risk mitigation strategies

- Domestic European manufacturing: Meyer Burger, REC, Enphase EU

- How solar design software integrates procurement planning

Latest Updates: European Solar Supply Chain 2026

The European solar supply chain in early 2026 is defined by three intersecting dynamics: historically low module prices, uneven component availability across non-module categories, and regulatory uncertainty around trade policy.

Solar Module Prices Europe — March 2026

| Module Type | Tier-1 Large Volume (≥500 kWp) | Mid-Market (50–499 kWp) | Small EPC (<50 kWp) |

|---|---|---|---|

| Mono PERC (standard) | €0.14–€0.16/Wp | €0.17–€0.21/Wp | €0.22–€0.27/Wp |

| TOPCon bifacial | €0.16–€0.19/Wp | €0.19–€0.24/Wp | €0.24–€0.29/Wp |

| HJT heterojunction | €0.22–€0.27/Wp | €0.26–€0.32/Wp | €0.30–€0.38/Wp |

| EU-manufactured (Meyer Burger, REC) | €0.28–€0.38/Wp | €0.30–€0.40/Wp | €0.33–€0.44/Wp |

| TÜV/IEC certification premium | +€0.03–€0.05/Wp | +€0.03–€0.05/Wp | +€0.03–€0.06/Wp |

Prices are ex-warehouse Germany/Netherlands. Freight, import duties, and local VAT add 5–12% depending on destination country and volume.

Lead Times by Equipment Category — Q1 2026

| Equipment | Standard Lead Time | Expedited (with premium) | Key Variables |

|---|---|---|---|

| Tier-1 Chinese modules | 2–5 weeks | 1–2 weeks | Port congestion, vessel schedules |

| EU-manufactured modules | 4–8 weeks | 3–5 weeks | Production allocation |

| String inverters (Fronius, SMA, Huawei) | 5–10 weeks | 3–6 weeks | Semiconductor availability |

| Microinverters (Enphase, APsystems) | 3–6 weeks | 2–4 weeks | Better than 2024 |

| Aluminum mounting systems | 2–4 weeks | 1–2 weeks | Stock levels improved |

| Flat-roof ballasted systems | 3–6 weeks | 2–4 weeks | Custom configurations |

| DC cables (6mm², 4mm²) | 1–3 weeks | In stock at major distributors | Widely available |

| AC protection/breakers | 2–5 weeks | 1–3 weeks | Brand-specific |

| Monitoring/optimizers | 3–7 weeks | 2–4 weeks | Varies by brand |

Key Takeaway — Lead Time Asymmetry

The most dangerous procurement assumption in 2026 is treating all components as equally available. Modules are plentiful; string inverters from European brands remain the most constrained category. A single delayed inverter shipment can idle a fully assembled rooftop system for 6–8 weeks, consuming carry costs and delaying commissioning revenue. Procurement planning must sequence inverter orders first.

Module Price Trends in Europe: Understanding the Tier System

The collapse in global solar module prices has not benefited all buyers equally. To understand why your procurement cost differs from the spot price quoted in industry news, you need to understand how the tier system works in European distribution.

What Drives Price Differences Between Buyers

The €0.14/Wp module price that Tier-1 EPC firms source directly from Chinese manufacturers (FOB Shanghai or DDP Rotterdam) is not available to an installer purchasing 80 panels for a 32 kWp residential project. The difference is not simply margin — it reflects genuine economics of logistics, financing, and minimum order quantities.

Volume aggregation: Manufacturers optimize production runs. A 40-foot container holds approximately 500–700 modules. Buyers who can commit to full-container-load (FCL) quantities receive substantially different pricing than those ordering less-than-container-load (LCL) quantities, which require consolidation and attract higher freight rates.

Payment terms: Large EPCs that can extend 90–120 day letters of credit get better pricing than smaller firms requiring shorter credit windows. Distributors absorb this financing cost and price it into their margins.

Certification and compliance costs: Modules destined for EU markets require CE marking, IEC 61215 type approval, and increasingly, specific national certifications. These certification costs are spread across volume. For smaller batches, the per-unit cost of compliance documentation rises.

Currency hedging: Chinese manufacturers quote in USD or EUR. When the EUR/USD rate moves, spot pricing shifts. Large buyers hedge currency exposure over 6–12 month windows; smaller buyers are fully exposed to spot rate risk.

Tier-1 vs. Tier-2 vs. Tier-3 Modules: What It Actually Means

The “tier” designation, popularized by Bloomberg NEF, is primarily a bankability rating — it indicates whether a manufacturer’s modules have sufficient project finance track record to be accepted by lenders. It is not a direct quality metric, though the two are correlated.

Tier-1 manufacturers (including JA Solar, LONGi, Trina Solar, Canadian Solar, Jinko Solar) have: 5+ years of consistent delivery, publicly available bankability reports, independent performance testing from Kiwa PVEL or similar labs, and established EU-market distribution infrastructure. Their modules command a price premium over lesser-known brands, but the premium is typically justified by reduced rework risk, bankability for commercial project finance, and reliable warranty administration.

Tier-2 manufacturers offer reasonable quality at lower price points — typically 10–20% below Tier-1 at equivalent specifications. The risk is warranty enforcement: if a manufacturer shrinks or exits the European market, warranty claims become unenforceable regardless of the paper terms. This is not theoretical — several Chinese manufacturers that were active in Europe in 2021–2022 have since reduced their presence significantly.

Tier-3 and unbranded modules should be avoided for any commercial or grid-connected residential installation. The CE mark can be falsified, IEC 61215 test reports may cover different module variants, and resale value of systems using unverified modules is severely impacted.

Pro Tip

Before finalizing a module supplier, request the most recent Kiwa PVEL Product Scorecard or DNV GL Performance Ratio report for the exact model number you are purchasing. Reputable Tier-1 suppliers provide these without hesitation. If a supplier deflects or provides reports for different module variants, treat it as a red flag regardless of headline pricing.

EU Anti-Dumping Policy: The Price Floor Risk

The most consequential policy variable for European solar procurement in 2026 is the EU’s evolving position on anti-dumping and countervailing duties on Chinese solar modules and cells.

History: The 2013–2018 Measures

The EU imposed anti-dumping duties on Chinese crystalline silicon modules in 2013, following complaints from European manufacturers. These measures established a minimum import price (MIP) of approximately €0.56/Wp — well above prevailing Chinese manufacturing costs. The measures were renewed in 2017 and then allowed to expire in September 2018, following lobbying from downstream installers and EPCs who argued the duties increased installation costs and suppressed European solar deployment.

After the expiry, Chinese module prices fell sharply, European manufacturers lost market share, and several EU-based producers (including SolarWorld) went bankrupt or were acquired.

Current Status: The 2025–2026 Investigation

In late 2024, the European Solar Manufacturing Council (ESMC), representing Meyer Burger, REC Group, and other EU-based producers, filed a new anti-dumping complaint with the European Commission. The complaint alleges that Chinese manufacturers are selling modules below cost of production (dumping) and receiving state subsidies (countervailable), both prohibited under WTO rules.

As of March 2026, the Commission’s investigation is ongoing. A preliminary determination is expected in mid-2026. Key possible outcomes:

- No measures: Status quo maintained; Chinese module prices remain at current levels

- Minimum import price: A floor price per Wp established, similar to 2013–2018 structure

- Ad valorem duties: A percentage tariff applied on top of declared import value

- Undertaking agreement: Chinese manufacturers commit to minimum prices voluntarily

The uncertainty itself is a procurement risk. If measures are imposed, module prices in Europe could increase by 30–60% for Chinese-origin products within weeks of the determination. EPCs with forward contracts may be protected; those buying spot will face sudden cost increases.

Key Takeaway — Anti-Dumping Risk Management

Any European EPC with projects scheduled for H2 2026 or 2027 should evaluate procurement timing carefully. Forward contracts with reputable distributors that include duty-adjustment clauses are the cleanest risk mitigation. Alternatively, consider pricing EU-manufactured modules into project bids at a premium — if Chinese duties land, your margins are protected; if they do not, you can renegotiate at tender stage.

For broader context on how European solar policy is evolving in 2026, see our guide to solar energy policies Europe and the full breakdown of European solar incentives.

Lead Times by Equipment Category: What Is Actually Constrained

The narrative that “solar supply chains are fixed” understates the variability between equipment categories. Modules are abundant. The constraints that actually delay project commissioning in 2026 sit further down the BOM.

Modules: Supply Exceeds Demand

The global solar module manufacturing capacity in 2025 reached approximately 1,000 GWp/year — roughly three times projected global installation demand. Europe is awash in modules, and distributors have built substantial buffer stocks in Germany, the Netherlands, Spain, and Italy. For standard module specifications (mono PERC 400–450 Wp, or TOPCon 410–460 Wp), lead times from major European distributors are 1–3 weeks for ex-warehouse stock, 4–6 weeks for custom specifications or large quantities.

The practical implication is that modules should not be the item driving your project schedule. If your procurement is module-constrained, you are either ordering very large volumes, using an unusual specification, or working with an insufficiently diversified supplier base.

String Inverters: The Real Constraint

String inverters from European brands — Fronius (Austria), SMA Solar Technology (Germany), and ABB/FIMER (Italy) — have operated under more constrained supply than modules throughout 2023–2025. The core issue is semiconductor availability: modern string inverters use specialized power electronics components that are not immune to broader electronics supply chain dynamics.

Fronius Symo GEN24 (the dominant German/Austrian residential and commercial inverter) has carried lead times of 6–12 weeks at distributor level through most of 2024–2025. Availability improved in late 2025 but remains tighter than module supply. SMA Sunny Tripower leads similarly.

Chinese inverter manufacturers (Huawei, GoodWe, Growatt, Solis) have substantially better availability — typically 3–5 weeks — but face increasing scrutiny from EU cybersecurity regulators. The EU’s Network and Information Security Directive 2 (NIS2) and ongoing reviews of Chinese technology in critical infrastructure are affecting large-scale commercial and C&I inverter selection. Residential applications face less regulatory pressure.

Procurement implication: For commercial and C&I projects, order inverters at project award — not at permit approval. For residential projects using Fronius or SMA, maintain 4–6 weeks of buffer in your project schedule after permit clearance.

Mounting Systems: Improved but Category-Specific

Aluminum extrusion for rail-based mounting systems (Schletter, K2 Systems, IronRidge equivalents) has normalized significantly since 2021–2022 when aluminum prices spiked following energy cost increases in European smelting. Standard roof-mount rails, mid-clamps, and end-clamps are ex-stock at most major European solar distributors.

Flat-roof ballasted mounting systems for commercial rooftops present different challenges. Custom configurations — defined by roof load calculations, local wind and snow loading requirements, and module orientation — typically require engineering review and 3–6 weeks of production lead time. Generic ballasted systems without project-specific engineering can be sourced faster but carry liability risk if installed without formal load calculations.

Ground-mount systems for utility-scale and large C&I projects have 6–14 week lead times for tracker systems and 4–8 weeks for fixed-tilt, driven by project-specific structural design requirements.

Balance of System (BOS): The Hidden Delay Risk

DC cabling, junction boxes, AC protection equipment, monitoring gateways, and isolators are individually fast to source — but collectively represent the most common cause of commissioning delays. Why? Because no single BOS component takes long to source, but a project cannot commission if any single item is missing. A missing 4mm² DC cable entry gland, a wrong-specification AC isolator, or a delayed monitoring gateway can hold up commissioning for 2–3 weeks while the correct part is located and delivered.

This is precisely where accurate solar software creates measurable financial value. SurgePV’s generation and financial tool calculates project-level cost impact automatically when BOM components change. Software that generates a complete, specification-accurate BOM from the design — including cable lengths, connector types, protection ratings, and monitoring hardware — eliminates the “forgotten component” problem that costs EPCs significant margin in aggregate across the European market each year.

For a detailed breakdown of how BOM generation software works in practice, see our dedicated guide to solar BOM software.

Warehouse and Stocking Strategies for European EPCs

The optimal procurement strategy for a European EPC in 2026 depends heavily on project pipeline visibility, working capital, and geographic coverage. There is no universally correct approach — but there are clear patterns that distinguish profitable EPCs from margin-constrained ones.

Just-in-Time Procurement: Appropriate Only at Scale

Large EPCs with predictable pipeline (20+ MW/year, consistent project types) can operate effective just-in-time procurement because they have:

- Sufficient volume to negotiate framework agreements with distributors that include price protection and guaranteed allocation

- Established relationships enabling expedited shipments when schedules slip

- Internal procurement teams that track lead times continuously and adjust ordering schedules

For EPCs below approximately 5 MW/year, pure JIT procurement creates margin volatility. The inability to lock prices 60–90 days forward means project costs can shift materially between sale and delivery. A 3% module price increase on a thin-margin commercial project can eliminate the project’s profitability entirely.

Strategic Stocking: The Working Capital Trade-Off

Holding 2–4 weeks of module inventory eliminates spot price exposure for near-term projects, enables faster delivery timelines (a competitive advantage in markets where clients value speed), and reduces per-unit transport costs through consolidated ordering.

The cost is working capital. At current module prices of €0.17–€0.22/Wp for mid-market buyers, a 100 kWp stock position represents approximately €17,000–€22,000 in tied capital. For smaller EPCs, this is meaningful — it needs to be weighed against the cost of missed margin from spot procurement.

A practical middle path: maintain stock of fast-moving components (DC cables, common module specifications, standard mounting hardware) and order inverters and mounting systems project-specifically once permits clear.

Distributor-Held Stock Programs

Several major European solar distributors — Krannich Solar, IBC Solar, BayWa r.e., Memodo, and Enerpoint — offer “reserve stock” programs where EPCs can allocate future volume at today’s price without taking immediate physical delivery. These programs effectively provide price hedging without the working capital burden of physical inventory.

The trade-off is commitment risk: most reserve stock programs require minimum take-up within 60–90 days, with penalties or forfeitures for under-ordering. For EPCs with reliable pipeline visibility, these programs offer excellent value. For those with uncertain project flow, the commitment risk can exceed the price protection benefit.

Pro Tip

When evaluating reserve stock programs, calculate the cost of full forfeiture as a percentage of the total protected margin. If a 10% forfeiture penalty on a 100 kWp reserve represents €350, but price protection saves €800 in margin on a €0.04/Wp movement, the program has positive expected value even at 40% pipeline failure probability. Run the math rather than evaluating these programs on qualitative comfort alone.

Quality Certification Requirements: IEC 61215, CE, MCS, TÜV

Certification requirements in European solar procurement are more fragmented than most EPCs realize, particularly those operating across multiple national markets. A module that is fully compliant for installation in Germany may require additional documentation for the UK, and neither set of documents may satisfy the specific requirements of a Spanish utility interconnection agreement.

IEC 61215 and IEC 61730: The Foundation

IEC 61215 (Design Qualification and Type Approval for Crystalline Silicon PV Modules) is the global baseline standard for module testing. It covers thermal cycling, humidity freeze, damp heat, UV exposure, mechanical load, hail, and hot-spot endurance testing. Any grid-connected solar installation in Europe should use only IEC 61215-certified modules.

IEC 61730 covers safety qualification — specifically, fire safety classification, electrical isolation, and protection against electric shock. Both IEC 61215 and IEC 61730 certification are prerequisites for CE marking, which is in turn required for any product sold in EU member states.

The critical procurement implication: do not accept a supplier’s claim of certification without documentation. Request the test certificate from the certifying body (TÜV Rheinland, TÜV SÜD, Bureau Veritas, or equivalent) specifying the exact module model number and version. Module variants (different cell count, different glass specifications) require separate certifications — a certificate issued for a 144-cell module does not cover a 132-cell variant, even from the same manufacturer and model family.

CE Marking and EU Declaration of Conformity

CE marking is a declaration by the manufacturer that the product meets EU health, safety, and environmental protection standards. For solar modules, this encompasses the Low Voltage Directive, the RoHS Directive (restricting hazardous substances), and the WEEE Directive (waste electrical and electronic equipment).

As a procuring EPC, your responsibility is to verify that CE documentation is valid and covers the specific products you are installing. Grid operators and building inspectors in Germany, France, the Netherlands, and other EU markets increasingly scrutinize CE compliance during commissioning inspections. A failed inspection due to documentation gaps can delay grid connection by 4–8 weeks while paperwork is corrected.

MCS Certification: UK-Specific Requirements

For EPCs operating in the United Kingdom (post-Brexit), the Microgeneration Certification Scheme (MCS) is the dominant quality standard for residential and small commercial solar installations. MCS certification is required for:

- Eligibility for the Smart Export Guarantee (SEG) — the UK’s current solar export payment mechanism

- Compliance with building regulations in England, Wales, and Scotland

- Insurance coverage under most specialist solar installer policies

MCS certification covers both the products (modules, inverters) and the installation company. A module with IEC 61215 and CE marking is not automatically MCS-certified — the manufacturer must separately apply for MCS product listing. When procuring for UK projects, always verify MCS product listing for each module and inverter model at the MCS product database, updated regularly.

TÜV and VDE Certification: German Market Standards

Germany remains the largest single solar market in Europe. German grid operators, particularly regional DSOs (distribution system operators), have specific requirements beyond EU-minimum standards.

VDE-AR-N 4105 governs the technical requirements for grid connection of generation systems in low-voltage networks. Inverters installed in Germany must be certified to this standard — it covers anti-islanding protection, reactive power capability, and remote control interfaces. Huawei, SMA, Fronius, and GoodWe all maintain VDE-AR-N 4105 certification for their current residential and commercial product lines.

TÜV certification (from TÜV Rheinland or TÜV SÜD) carries significant market weight in Germany, Austria, and Switzerland. While not always legally mandated beyond CE requirements, TÜV-certified products are preferred by commercial clients, lenders financing solar assets, and building insurers. For commercial and C&I projects, TÜV module certification is effectively a commercial necessity even where not legally required.

Key Takeaway — Certification Documentation Management

Create a digital certification file for every product line you regularly procure. Include IEC 61215 test reports, CE Declaration of Conformity, TÜV certificates, and MCS product listings (for UK projects). Update these files when manufacturers release new module variants — certificates are model-specific, not brand-specific. A single procurement team member maintaining this library saves 2–4 hours per project in documentation assembly and eliminates commissioning delays from documentation gaps.

Preferred European Solar Distributors and Their Procurement Models

The European solar distribution market has consolidated significantly since 2020. A handful of large-scale distributors now control the majority of module volume into Germany, Italy, the Netherlands, Spain, and the UK. Understanding how each distributor operates helps EPCs select the right procurement relationships.

Pan-European Distributors

Krannich Solar (Germany-headquartered, 17+ country presence): One of Europe’s largest independent solar distributors, with warehouses in Germany, Italy, Spain, France, and the UK. Krannich operates a multi-brand model, stocking modules from JA Solar, Canadian Solar, Trina Solar, and others alongside inverters from Fronius, SMA, Huawei, and GoodWe. Their pricing is transparent for registered trade customers, with volume-tiered pricing that becomes competitive above 50 kWp. Krannich’s logistics are strong — they can deliver to most European locations within 3–5 business days from central warehouse stock.

BayWa r.e. Solar Trade (Germany): The solar distribution arm of BayWa AG, one of Europe’s largest agriculture and energy conglomerates. BayWa r.e. offers a full-service model including project financing, technical support, and logistics. Their pricing is typically 3–5% above pure-volume distributors, but their service offering makes them a preferred partner for EPCs entering new market segments.

IBC Solar (Germany): Strong in the DACH market (Germany, Austria, Switzerland) and expanding into Southern Europe. IBC Solar differentiates on technical quality — they maintain an in-house engineering team that evaluates products before listing them. Well-suited for commercial and C&I EPCs that need deep technical support.

Memodo (Germany): Newer market entrant with an e-commerce-first approach. Memodo’s online platform offers transparent real-time pricing, stock levels, and documentation downloads without requiring sales calls. Their model suits smaller EPCs that value procurement speed and transparency over relationship-based negotiation. Pricing is competitive at smaller volumes (10–100 kWp range).

Regional Specialists

Enerpoint (Italy): The dominant Italian solar distributor, with warehouses in northern Italy (Bergamo) and southern logistics hubs. Enerpoint’s strength is local market knowledge — they understand Italian grid connection requirements, regional incentive documentation, and GSE registration processes better than pan-European distributors. Essential for EPCs operating primarily in the Italian market.

Solarex (Spain/Portugal): Leading Iberian distributor with strong relationships with Spanish grid operators and understanding of Spain’s self-consumption regulations (Royal Decree 244/2019 framework). Their inverter stock of SMA and Fronius equipment is typically deeper than pan-European platforms in the Iberian market.

Solar 4 RCPs (Netherlands/Belgium): Specialist distributor for the Benelux market, with deep stock of components suited for flat-roof commercial systems — common in the low-pitched commercial building stock of the Netherlands and Belgium. Strong on ballasted mounting systems and Dutch DSO documentation requirements.

Distributor Selection Criteria

When evaluating a new distributor relationship, assess the following:

- Financial stability: Request trade references and check credit ratings. Several European solar distributors have faced financial difficulties as module prices fell and inventory written down in value. A distributor that holds significant inventory bought at 2023 prices and now worth 40% less carries balance sheet risk.

- Certification documentation support: Does the distributor maintain a document portal with current CE, IEC, and TÜV certificates for all listed products? This is a significant time-saver at scale.

- Returns and defect handling: What is the returns policy for damaged goods and early-life failures? A distributor with a clear, efficient returns process reduces the administrative cost of warranty management.

- Logistics reliability: Track record for on-time delivery. Industry contacts are the best source — published delivery statistics are marketing materials.

Financing Procurement: Inventory Finance and Supplier Credit Terms

Procurement financing is an underutilized lever for European EPCs. Most smaller installers fund procurement from working capital, absorbing the full cost of materials 4–8 weeks before client payment. At current module prices, a 500 kWp project may require €90,000–€140,000 in material procurement before any revenue is recognized. This is a substantial working capital demand for a business running 3–5 projects concurrently.

Supplier Credit Terms: Baseline and Negotiation

Most European solar distributors offer standard credit terms of 30 days net from invoice date for registered trade customers with acceptable credit history. Volume customers above certain annual thresholds (typically €500,000+ annual spend) can negotiate 45–60 day terms.

The value of extended supplier credit is significant. At 60-day terms vs. 30-day terms, a company running €500,000 per month in procurement volume effectively has an additional €500,000 in working capital — equivalent to a low-cost revolving credit facility. Negotiating payment terms is one of the highest-ROI finance activities available to procurement managers.

Practical negotiation levers:

- Consolidate purchasing with fewer suppliers to increase individual relationship value

- Commit to annual volume targets in exchange for extended terms

- Offer earlier payment (e.g., 15 days) in exchange for 1–2% early payment discount, then evaluate whether the cash cost of early payment exceeds or is less than your borrowing rate

Inventory Finance Facilities

Specialist inventory finance facilities — offered by trade finance lenders and some specialist solar finance providers — allow EPCs to draw financing against physical solar inventory held in their warehouse or in transit. The facility is typically structured as:

- Up to 80% of invoice value financed

- 60–120 day tenor, aligned to installation and client billing cycle

- Interest rate 3–8% annualized, depending on credit quality and collateral

For EPCs that want to take advantage of stocking strategies without consuming working capital, inventory finance provides the bridge. The key requirement is that the lender must be able to verify and value the collateral — which requires organized inventory management and clear documentation of stock holdings.

Client Deposit and Stage Payment Structures

The cleanest working capital solution for small EPCs is client funding. A standard European residential solar contract structures as:

- 30–40% deposit on contract signing

- 40–50% on material delivery to site

- 10–20% on commissioning

This structure, if negotiated correctly, means the client’s deposit covers material procurement costs before the EPC has spent its own capital. Many EPCs underestimate their negotiating position on payment terms — clients who want the project done quickly are frequently willing to front-load payments in exchange for schedule priority.

How Accurate BOM Software Reduces Procurement Waste

Procurement waste — materials ordered but unused, or materials not ordered and needed urgently — is one of the most opaque cost centers in European solar installation businesses. The costs are real but rarely visible in financial reporting because they manifest as overhead (staff time chasing parts), margin erosion (expedited freight), and schedule delays (idle labor).

A study of mid-size European EPCs (50–500 projects per year) estimated that BOM errors and omissions — including wrong specifications, missed components, and quantity calculation errors — add an average of 2.8% to material costs per project. On a €100,000 material budget, that is €2,800 per project in avoidable waste. At 100 projects per year, it represents €280,000 in recoverable margin.

The Root Cause: Design-to-Procurement Disconnection

The most common procurement waste scenario is straightforward: a project is designed in one system (or on paper), and the BOM is assembled separately by a procurement coordinator who must interpret the design intent. This handoff creates error opportunities:

- Cable lengths calculated from memory or rough estimate rather than from the design

- String configuration changes during site survey not reflected in the procurement BOM

- Module substitution mid-project (because the originally specified model went out of stock) not triggering updated BOM calculation for mounting hardware

- AC protection sizing based on original design even after inverter was changed

Each of these errors generates real cost — either in wasted materials, expedited replacements, or labor rework.

How Design-Integrated BOM Generation Eliminates the Gap

Solar design software that natively generates a BOM from the completed design eliminates the translation error entirely. When the design changes — module quantity adjusted for roof space, string configuration optimized for shading, inverter upsized for future expansion — the BOM updates automatically. The procurement coordinator receives a current, accurate component list without manual reconciliation.

Critically, a well-designed solar proposal software connects the design and commercial proposal to the procurement BOM as a single data flow. The quoted system in the proposal is the designed system, and the designed system generates the procurement BOM. This is not a theoretical efficiency — it is the operational foundation of procurement accuracy.

The financial impact compounds at the project level. Fewer emergency orders mean less expedited freight. Accurate cable quantities mean less waste. Correct protection device specifications mean no failed commissioning inspections. Combined, these translate directly to higher per-project margin without requiring any price renegotiation with suppliers.

For EPCs evaluating how BOM software fits into their procurement workflow, the solar BOM software guide provides a detailed framework for tool evaluation and implementation.

Stop Losing Margin to BOM Errors

SurgePV generates a complete, specification-accurate BOM directly from your system design — so your procurement team always has the right component list, the first time.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

Supply Chain Risk Mitigation Strategies

A strong supply chain risk framework for a European EPC in 2026 addresses four categories of risk: price risk, availability risk, quality risk, and regulatory risk.

Price Risk Mitigation

Forward purchasing: Lock in component prices 60–90 days in advance for projects with signed contracts. The procurement certainty is worth a small premium over spot pricing.

Dual supplier relationships: Maintain active relationships with at least two distributors for each equipment category. This provides competitive tension in pricing negotiations and fallback availability when one supplier is constrained.

Anti-dumping scenario planning: Model project economics under two price scenarios — current pricing, and pricing 30% higher (a plausible anti-dumping duty scenario). Projects that remain viable under the higher scenario are lower risk to quote; projects that only work at current prices carry policy risk.

Currency hedging: For EPCs quoting in euros but sourcing modules priced in USD, consider simple forward contracts or currency options. Most business banks offer these products for trade-qualified customers.

Availability Risk Mitigation

Specification flexibility: Where possible, design systems to accommodate multiple module models at the same wattage class. This allows substitution if the originally specified module goes out of stock without triggering a full redesign.

Inverter buffer stock: Maintain 2–4 residential inverter units of your most common specification in stock. The carrying cost (typically €1,200–€1,800 per unit at residential scale) is manageable, and having inventory eliminates the risk of a 6-week wait blocking a commissioned project.

BOM completion review: Before finalizing any procurement order, run a component-by-component check against the design BOM. This is operationally simple when using integrated design and BOM software — the software flags any missing items before the order is submitted.

Quality Risk Mitigation

Approved vendor list: Maintain an internal approved vendor list for modules and inverters. Every product on the list must have current certification documentation verified by your procurement team. Do not allow project managers to source outside the approved vendor list without explicit approval.

Incoming inspection protocol: Implement a receiving inspection protocol for modules. Visual inspection for transport damage, serial number verification against delivery documentation, and spot-checking of carton labels for model and wattage consistency catches problems before installation that would be expensive to rectify afterward.

Performance bond requirements: For large commercial and C&I projects, require performance bonds from module and inverter suppliers — particularly for brands without an established European warranty administration history. A performance bond from a reputable European insurer provides meaningful protection if a manufacturer reduces its European presence.

Regulatory Risk Mitigation

Certification database maintenance: As described in the certification section above, maintain current certification files for every product line you regularly source. Audit these files quarterly.

Grid operator relationship management: In your primary markets, maintain direct contact with the local DSO technical department. Grid operator requirements change more frequently than published standards suggest — informal advance notice of coming changes is valuable.

Import compliance monitoring: Assign responsibility for monitoring EU trade policy developments affecting solar — specifically anti-dumping proceedings and any new product safety regulations — to a named team member. Set alerts for European Commission DG Trade publications.

Domestic European Manufacturing: Meyer Burger, REC, Enphase EU

The question of whether to source EU-manufactured solar modules has shifted from ideological to strategic in 2026. The potential for anti-dumping duties on Chinese modules has made EU-manufactured product a genuine procurement hedge, not merely a “buying European” premium.

Meyer Burger Technology

Meyer Burger (Switzerland-headquartered, manufacturing in Germany and the Czech Republic) produces high-efficiency HJT (heterojunction) modules under its own brand. After pivoting from equipment manufacturing to cell and module production in 2020, Meyer Burger has built significant EU-based capacity — approximately 1.4 GW annual nameplate capacity across its Bitterfeld-Wolfen (Germany) facility.

Meyer Burger modules carry a genuine performance premium: their HJT technology delivers higher temperature coefficient performance than standard PERC (better output in hot climates) and lower degradation rates over 30-year system life. Their modules are covered by a 30-year performance warranty — longer than the standard 25-year industry norm.

The price premium is real: Meyer Burger modules trade at €0.28–€0.35/Wp wholesale — approximately 60–80% higher than equivalent Chinese TOPCon. For projects where lifecycle performance, anti-dumping protection, and bankability for German commercial clients are valued, this premium is justifiable. For purely price-sensitive residential markets, it remains challenging to sell in volume.

Meyer Burger is also actively pursuing EU subsidy support under the Net-Zero Industry Act (NZIA), which designates solar manufacturing as a strategic technology. NZIA-backed support, if materially funded, could reduce the cost gap by 2027–2028.

REC Group

REC Group (Norwegian-founded, now owned by Reliance Industries) operates manufacturing in Singapore — not EU-based — but is considering European manufacturing capacity, and their modules are widely accepted as “bankable” European-branded product in the European market. REC Alpha series modules (EWT back-contact technology) deliver industry-leading efficiency and carry strong warranty terms.

For European EPCs seeking non-Chinese module supply without the Meyer Burger price premium, REC represents a practical middle ground. Their distribution in Europe is well-established through Krannich and IBC Solar.

Enphase European Manufacturing

Enphase Energy announced and has partially delivered on European manufacturing for its IQ8 microinverter series, with assembly in Romania. European-manufactured Enphase microinverters carry a “Made in EU” certification that is valuable in procurement frameworks requiring local content, and they are not subject to potential Chinese module-equivalent supply chain concerns.

The broader Enphase ecosystem — microinverters, battery storage, monitoring — remains the dominant choice for European residential installers who value the no-string-architecture advantage for complex roof designs and shading situations. Enphase’s lead times from European stock improved significantly in 2025, returning to 3–5 week standard after the 6–10 week delays of 2023–2024.

Key Takeaway — EU Manufacturing as Procurement Strategy

For EPCs that regularly quote commercial projects requiring project finance, or for EPCs with significant German commercial market exposure, EU-manufactured modules (Meyer Burger) or EU-assembled microinverters (Enphase Romania) offer anti-dumping protection and bankability advantages that justify the price premium on a project-economics basis. Run the blended cost analysis project-by-project rather than adopting a blanket sourcing policy.

How Solar Design Software Integrates Procurement Planning

The procurement function in most European EPCs is organizationally separated from the design function — a structural disconnect that generates the majority of procurement inefficiency. Design produces a system specification; procurement translates that specification into purchase orders. Every translation step introduces error opportunity and time delay.

The integration of solar design software with procurement planning collapses this distance. When a complete system design — including module layout, string configuration, inverter sizing, cable routing, and BOS specifications — is captured in a single platform, the procurement BOM becomes a direct output of the design, not a separate derivation from it.

What Design-Integrated Procurement Actually Looks Like

In practice, effective procurement integration means:

Automatic quantity generation: The design software calculates module count from roof layout. It calculates cable lengths from string-to-combiner-to-inverter routing. It generates mounting hardware quantities from panel layout and selected mounting system. The procurement team receives quantities, not a design they must interpret into quantities.

Component specification accuracy: A design that specifies a Fronius Symo GEN24 10.0 generates a procurement line item for exactly that model — not a generic “10 kW string inverter.” This specificity propagates to the certification check (is this model MCS-listed for a UK project?) and to the stock check (is this model currently ex-stock at Krannich?).

Change propagation: When the system design changes — roof area revised, shading analysis updated, client requests battery addition — the BOM updates to reflect all impacted components. Procurement is notified of changes rather than discovering them at delivery.

Supplier format export: The BOM exports in formats that distributors can directly import into their quoting systems — eliminating the manual re-entry of component lists into supplier portals. For EPCs running 50+ projects per year, this alone saves substantial administrative time.

Timeline integration: Knowing when each component is required (based on the installation schedule linked to the design), the software can alert procurement teams to order long-lead items (inverters) weeks before short-lead items (cables and connectors) to align delivery timing with installation sequence.

This is the operational model that distinguishes EPCs with 15–20% gross margins from those running 8–10% in the same market. Procurement accuracy, design consistency, and reduced rework are the margin levers that separate the best-run European solar companies from those that compete purely on headline price.

For EPCs evaluating proposal and design workflow improvements, the solar proposal software section of the SurgePV platform addresses the full design-to-sale-to-procurement data flow.

Frequently Asked Questions

What are the main solar procurement challenges in Europe in 2026?

The dominant challenges are oversupply-induced price volatility from Chinese manufacturers, minimum order quantity barriers for small EPCs, extended lead times for non-module components (inverters, mounting), quality certification compliance across multiple EU markets, and currency-driven cost uncertainty. Anti-dumping policy uncertainty from the EU further complicates long-term supplier contracts, as price floors could shift significantly depending on trade decisions expected in mid-2026.

What are current solar module prices in Europe?

As of early 2026, Tier-1 monocrystalline PERC and TOPCon modules trade at €0.14–€0.18/Wp ex-warehouse in Germany and the Netherlands for large-volume buyers (>500 kWp). Small EPCs purchasing below 50 kWp lots typically pay €0.21–€0.28/Wp through distributors. Premium bifacial TOPCon modules with TÜV certification command a €0.03–€0.05/Wp premium over base pricing. Prices have declined roughly 40% since the 2023 peak and remain at historically low levels.

How long are solar inverter lead times in Europe in 2026?

String inverter lead times from European brands (Fronius, SMA) remain the most constrained equipment category at 5–10 weeks standard lead time. Chinese brands (Huawei, GoodWe, Solis) offer 3–5 weeks. Microinverters from Enphase improved significantly in 2025 to 3–6 weeks. The key action for EPCs is to place inverter orders at project award rather than waiting for permit clearance — a 6-week delay on inverter delivery creates disproportionate schedule and cost impact.

What is the risk of EU anti-dumping duties on Chinese solar modules?

The European Commission is investigating a new anti-dumping complaint filed in late 2024. If measures are imposed, Chinese module prices in Europe could increase by 30–60% within weeks of the determination, expected in mid-2026. EPCs should evaluate forward purchasing with duty-adjustment clauses, or price EU-manufactured modules into project bids as a hedge — Meyer Burger modules at €0.28–€0.35/Wp are immune to any Chinese anti-dumping action.

What certifications are required for solar modules in European markets?

At minimum: IEC 61215 (design qualification), IEC 61730 (safety), and CE marking (required for EU sale). Germany additionally requires VDE-AR-N 4105 compliance for inverters. The UK requires MCS product listing for Smart Export Guarantee eligibility. TÜV certification (Rheinland or SÜD) is commercially expected for German, Austrian, and Swiss commercial projects even where not strictly mandated. Always request model-specific certificates — brand-level claims are not sufficient.

How does solar design software improve procurement outcomes?

Design-integrated BOM generation eliminates the most common source of procurement error: the manual translation of a design into a component list. When the design software auto-generates quantities, specifications, and cable lengths directly from the system layout, procurement receives an accurate BOM without interpretation risk. Changes to the design propagate to the BOM automatically. Industry data suggests BOM errors add approximately 2.8% to material costs for EPCs using manual processes — a recoverable margin loss that design software directly addresses.

Which European solar distributors are best for small EPCs?

For small EPCs (under 1 MW/year), Memodo’s e-commerce platform offers the most accessible pricing transparency and documentation access without requiring volume commitments. Krannich Solar is the best relationship-based option for EPCs growing into the 1–5 MW/year range, with strong logistics coverage across most European markets. Regional specialists — Enerpoint in Italy, Solarex in Spain — outperform pan-European platforms for market-specific documentation and technical support.

What is inventory financing for solar procurement?

Inventory finance facilities allow EPCs to borrow against physical solar equipment held in their warehouse or in transit — typically up to 80% of invoice value, for 60–120 day tenors, at 3–8% annualized interest. This enables EPCs to purchase and hold strategic stock without fully consuming working capital. The facility is particularly valuable for EPCs that want to protect against module price volatility or anti-dumping duty risk by holding pre-purchased inventory, but lack the free cash to fund that stock from operating cash flow.