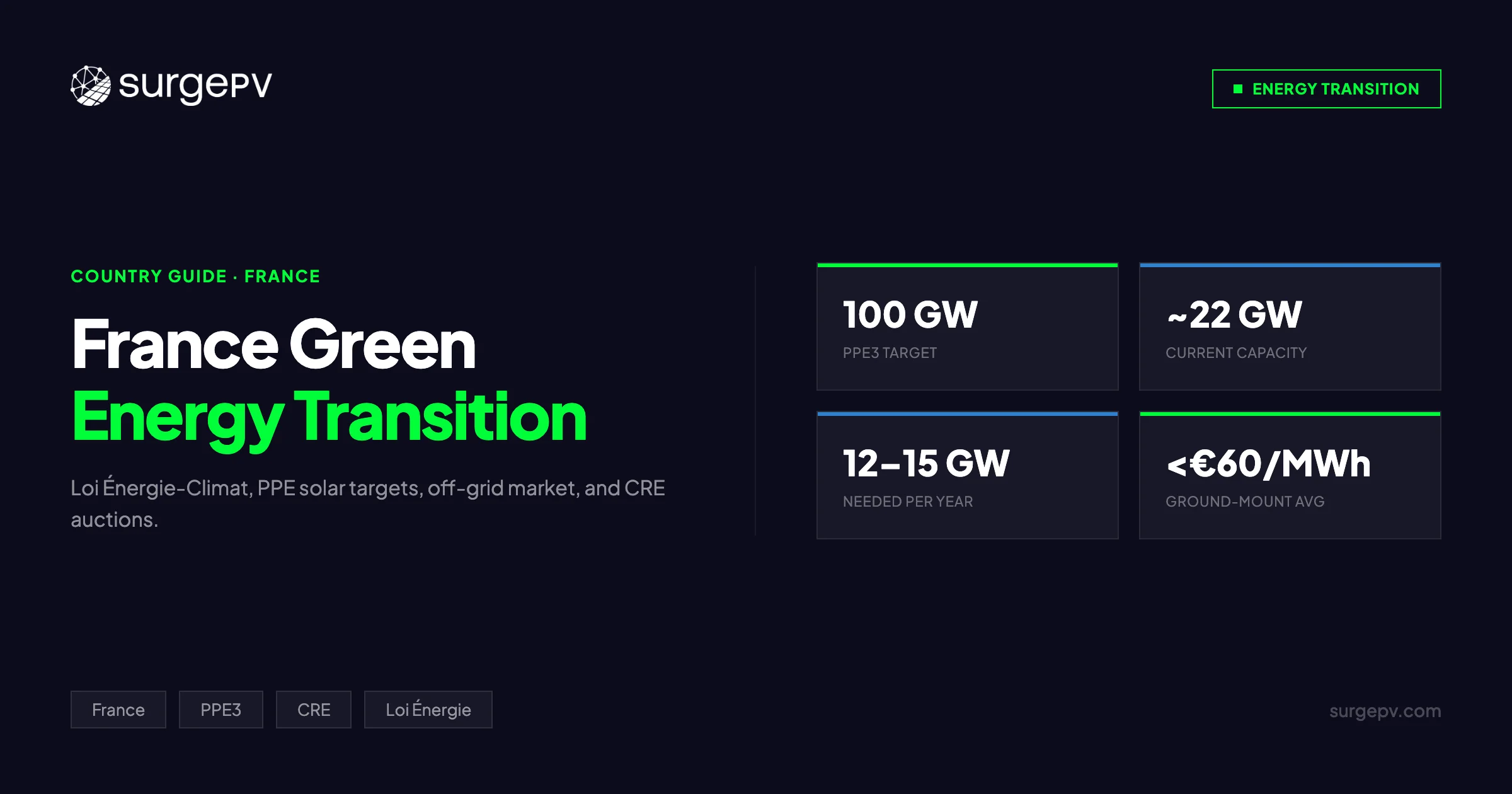

France faces one of the most ambitious solar acceleration challenges in Europe. Its Programmation Pluriannuelle de l’Énergie (PPE3) sets a 100 GW solar target by 2030 — yet at end-2024, installed capacity stood at roughly 22 GW. Closing that gap requires more than doubling the current annual deployment rate for six consecutive years.

France’s nuclear-dominated grid, its patchwork of overseas island territories, and its evolving regulatory framework under the Loi Énergie-Climat create a solar market unlike any other in Europe. Understanding it means examining federal policy, CRE auction dynamics, off-grid island economics, and regional irradiance patterns together.

This guide covers what solar professionals, investors, and policymakers need to navigate France’s green energy transition — from the legislative foundations to the mechanics of CRE tenders, autoconsommation policy, off-grid solar in Corsica and overseas territories, and what the 2026 market looks like for installers using solar design software to win projects.

TL;DR — France Solar Policy 2026

France targets 100 GW of solar by 2030 (PPE3) from ~22 GW installed today. CRE tender prices have fallen below €60/MWh for ground-mounted projects. Off-grid solar is growing rapidly in ZNI island territories (Corsica, La Réunion, Guadeloupe, Martinique, Guyane). Autoconsommation frameworks support individual and collective self-consumption up to 100 MW. Nuclear coexistence is a feature, not a bug — CFD contracts shield developers from wholesale price volatility.

In this guide:

- France renewable energy policy 2025–2026 — latest status table

- France solar capacity: installed GW vs 2030 target — the gap

- Loi Énergie-Climat and PPE framework — legislative foundations

- France photovoltaic market: growth trends, leading regions, and deployment rates

- France off-grid solar market — ZNI territories, Corsica, overseas islands, isolated farms

- CRE solar auctions — appels d’offres results, awarded capacity, how to bid

- Autoconsommation policy — individual and collective self-consumption framework

- Nuclear coexistence — how France’s baseload shapes solar economics

- Commercial and industrial solar in France

- Regional irradiance differences — Nord vs Sud deployment strategies

- 2026 investment outlook and policy updates

Latest Updates: France Renewable Energy Policy 2025–2026

Here is the current status of every active framework and program as of March 2026.

France Solar Policy Status — March 2026

| Framework / Program | Status | Key Update |

|---|---|---|

| PPE3 (2024–2033) | Active | 100 GW solar target confirmed; implementation decrees in force |

| Loi Énergie-Climat (2019) | Active | Carbon neutrality 2050 target unchanged |

| CRE Appels d’Offres — Ground-mount | Active | 2025 tenders awarded ~2.1 GW; 2026 Q1 round open |

| CRE Appels d’Offres — Rooftop | Active | Annual rounds; simplified track for 100–500 kWp |

| CRE ZNI Tenders (island territories) | Active | Dedicated rounds for Réunion, Guadeloupe, Martinique, Guyane |

| Autoconsommation S21 feed-in premium | Active | Up to 500 kWp systems; quarterly rate updates |

| EDF OA feed-in tariff | Active | For systems ≤100 kWp; rates updated quarterly |

| Agri-PV framework (décret 2023) | Active | Minimum 20% agricultural productivity maintained |

| ADEME Island Energy Fund | Active | ZNI battery + renewable project co-financing |

| RE2020 building regulation | Active | New buildings must demonstrate solar readiness |

Key 2025–2026 Policy Changes

PPE3 100 GW Target Confirmed (January 2024): France’s updated multiannual energy plan raised the 2030 solar target from 44 GW to 100 GW. The PPE3 covers 2024–2033 and includes intermediate milestones of 45 GW by 2026 and 75 GW by 2028. Current installation rates would need to triple to meet the 2028 milestone.

Accélération des Énergies Renouvelables (AER) Law — 2024 Implementation: The loi d’accélération des énergies renouvelables, passed in March 2023, established renewable energy acceleration zones (zones d’accélération pour les énergies renouvelables, ZAEnR). Municipalities must now designate acceleration zones, giving solar developers clearer land-use frameworks. Permitting timelines in designated zones are legally capped at 24 months.

Agri-PV Decree Refinement (2025): ADEME published updated technical guidance on agri-PV installation requirements. The minimum agricultural productivity standard — at least 80% of reference yield — is now assessed over three-year rolling averages, giving operators more flexibility in the first seasons of dual operation.

ZNI Renewable Targets Reaffirmed: All overseas island territories confirmed their 100% renewable electricity targets. La Réunion has set 2030 as its deadline. Guadeloupe and Martinique target 2035 for full transition. These timelines are driving accelerated off-grid and grid-connected solar investment.

Key Takeaway — The PPE3 Deployment Gap

France installed approximately 3 GW of solar in 2024. To hit 100 GW by 2030, annual additions must reach 12–15 GW from 2025 onward. This deployment gap represents a major investment opportunity — but also a policy execution risk that every solar developer in France must track.

France Solar Capacity: Installed vs 2030 Target

Current Installed Capacity — France Photovoltaic Market 2024–2025

France ended 2024 with approximately 22 GW of installed solar photovoltaic capacity, the fourth largest in the EU after Germany, Spain, and Italy.

| Year | Cumulative Installed (GW) | Annual Addition (GW) |

|---|---|---|

| 2019 | 9.4 | 0.9 |

| 2020 | 10.7 | 1.3 |

| 2021 | 13.2 | 2.5 |

| 2022 | 16.1 | 2.9 |

| 2023 | 19.3 | 3.2 |

| 2024 | ~22.2 | ~2.9 |

| 2026 target (PPE3) | 45 | — |

| 2028 target (PPE3) | 75 | — |

| 2030 target (PPE3) | 100 | — |

Sources: SER (Syndicat des Énergies Renouvelables), RTE, PPE3 official documents.

The Deployment Gap Is Structural

Reaching 100 GW by 2030 requires installing roughly 78 GW over six years — an average of 13 GW per year. France has never added more than 3.2 GW in a single year. This is a structural transformation of the country’s energy development capacity, not a minor acceleration.

The bottlenecks are well-documented:

- Permitting timelines: Even in AER-law acceleration zones, complex projects face 3–5 year cycles from application to commissioning

- Grid connection queues: RTE (the French transmission operator) has a backlog of connection requests exceeding 200 GW, creating multi-year waits for large projects

- Skilled labor shortfall: France has approximately 7,000 qualified solar installers for a market that requires 50,000+ to meet 2030 targets

- Financing bandwidth: France’s banking sector is adapting but project finance pipelines remain below the required investment rate of ~€15–20 billion per year

The AER law directly addresses some of these barriers, particularly permitting. Its practical impact on deployment rates will show up in 2026 data.

Pro Tip — CRE Backlog Opportunities

France’s grid connection backlog creates a two-speed market. Projects under 500 kWp on existing rooftops face the shortest grid queues. Solar professionals who focus on rooftop and agri-PV in the 100–500 kWp range can often commission projects 18–24 months faster than equivalent ground-mount developers. Accurate shade and yield modeling with solar shadow analysis software is critical for winning CRE bids in this size band.

France’s Green Energy Framework: Loi Énergie-Climat and PPE

The Loi Énergie-Climat (2019)

The Loi Énergie-Climat (LEC) of November 2019 is France’s primary climate legislation. Its key provisions:

- Carbon neutrality by 2050 (mandatory, not aspirational)

- Renewable energy at 40% of electricity production by 2030

- Closure of all coal power plants by 2022 (achieved)

- Phase-down of nuclear from 75% to 50% of electricity by 2035 (now under political review)

- Mandatory energy efficiency improvements in residential buildings

- Creation of the PPE as the primary planning instrument for energy transition

The LEC enshrines the PPE as a binding multiannual planning document, not just a ministerial guideline. This gives solar developers regulatory certainty over 9-year planning cycles.

The PPE (Programmation Pluriannuelle de l’Énergie)

The PPE is France’s multiannual energy program — the operational instrument that translates the LEC’s targets into capacity additions, auction volumes, and technology-specific objectives.

| PPE Version | Coverage Period | Key Solar Target |

|---|---|---|

| PPE1 | 2019–2023 | 20.1 GW by 2023 |

| PPE2 | 2019–2028 | 35–44 GW by 2028 |

| PPE3 | 2024–2033 | 100 GW by 2030 |

PPE3, finalized in early 2024, marks a sharp increase in ambition. The jump from 44 GW (PPE2 target) to 100 GW (PPE3 target) for the same 2030 endpoint reflects France’s belated recognition that solar deployment needs to accelerate dramatically.

Key PPE3 Solar Provisions

- Annual CRE tender volumes increased to 6–8 GW per year from 2025 (from ~3 GW historically)

- Agri-PV: Dedicated tender track with a target of 10 GW by 2030

- Floating solar: New tender category targeting 1 GW by 2030

- Building-integrated PV (BIPV): Simplified administrative regime for systems under 9 kWp

- Large ground-mount (>5 MW): Streamlined environmental assessment procedures in ZAEnR zones

Further Reading

For the broader European context, see our guides to EU solar energy policies and European solar incentives. For a detailed comparison of French and German policy approaches, the contrast in nuclear-solar coexistence is particularly instructive.

France Photovoltaic Market: Growth, Regions, and Deployment Patterns

Market Structure — Who Installs Solar in France

France’s PV market divides into three segments by project size and regulatory track:

| Segment | Capacity Range | Regulatory Track | Share of Market |

|---|---|---|---|

| Small residential/commercial | <100 kWp | EDF OA feed-in tariff | ~25% of volume |

| Mid-size commercial/industrial | 100–1,000 kWp | CRE rooftop tenders (simplified) | ~30% of volume |

| Large ground-mount | >1,000 kWp | CRE main tenders | ~45% of volume |

France Photovoltaic Market — Leading Regions by Installed Capacity

Regional solar deployment in France tracks irradiance, land availability, and local government support.

| Region | Installed Capacity (approx.) | Irradiance (kWh/m²/yr) | Key Driver |

|---|---|---|---|

| Occitanie | ~4.5 GW | 1,550–1,800 | High irradiance, agricultural land, early policy support |

| Nouvelle-Aquitaine | ~3.8 GW | 1,400–1,700 | Wine region agri-PV, logistics rooftop |

| Provence-Alpes-Côte d’Azur (PACA) | ~2.9 GW | 1,600–1,900 | Highest irradiance in metropolitan France |

| Auvergne-Rhône-Alpes | ~2.4 GW | 1,300–1,600 | Industrial rooftop, mountain agri-PV |

| Grand Est | ~1.8 GW | 1,100–1,300 | Logistics corridors, cross-border PPAs |

| Île-de-France | ~0.9 GW | 1,050–1,200 | Urban rooftop, carport solar |

France Solar Market 2026 — Key Indicators

- Annual new capacity (2025 est.): 3.5–4.5 GW

- CRE tender volume (2026): 6 GW targeted across all categories

- Average CRE price (ground-mount): €55–65/MWh

- Average CRE price (rooftop 100–500 kWp): €75–95/MWh

- Self-consumption installations: ~80,000 per year (residential + commercial)

- Average system cost (residential, 3–9 kWp): €1,800–€2,400/kWp all-in

- Average system cost (commercial ground-mount, >1 MW): €700–€950/kWp

Technology Mix

France’s installed PV is predominantly crystalline silicon. Emerging technology segments:

- Agri-PV: Growing rapidly — bifacial elevated structures over crops, east-west single-axis trackers above vines

- Floating PV: Pilot projects on reservoirs and quarry lakes; SolarDuck and Ciel & Terre active in French market

- BIPV: Small but growing for urban projects; incentivized under RE2020 building standards

- Carport solar: Fast-growing segment following the 2023 law mandating solar canopies on large parking lots

Key Takeaway — Parking Lot Solar Mandate

France passed a law in 2023 requiring parking facilities with more than 80 spaces to install solar canopies covering at least 50% of spaces. This applies to commercial, logistics, and public car parks. The mandate creates a large, compulsory market for canopy solar — estimated at 11 GW of potential capacity by 2028. Solar companies with solar design software capable of modeling canopy configurations and shading analyses will lead this segment.

France Off-Grid Solar Market

The france off-grid solar market is one of the most distinctive segments in European renewable energy, shaped by geography, regulatory isolation, and some of the highest solar irradiance values on French territory.

What Drives Off-Grid Solar in France

Off-grid solar in France exists across three distinct contexts:

- Non-interconnected zones (ZNI) — overseas island territories where grid isolation makes conventional electricity expensive

- Isolated metropolitan farms and rural properties — locations where grid connection costs exceed solar system costs

- Temporary and mobile installations — agricultural irrigation, remote monitoring, rural telecoms infrastructure

The ZNI Framework — Overseas Island Territories

France’s overseas territories classified as zones non-interconnectées (ZNI) include:

| Territory | Status | Population | Renewable Target | Solar Irradiance |

|---|---|---|---|---|

| La Réunion | ZNI (DOM) | 880,000 | 100% renewable by 2030 | 1,800–2,100 kWh/m²/yr |

| Guadeloupe | ZNI (DOM) | 380,000 | 100% renewable by 2030 | 1,700–2,000 kWh/m²/yr |

| Martinique | ZNI (DOM) | 360,000 | 100% renewable by 2030 | 1,700–2,000 kWh/m²/yr |

| Guyane | ZNI (DOM) | 300,000 | 100% renewable by 2030 | 1,600–1,900 kWh/m²/yr |

| Mayotte | ZNI (COM) | 330,000 | 50% renewable by 2030 | 1,800–2,100 kWh/m²/yr |

| Corse | ZNI | 340,000 | 40% renewable by 2030 | 1,500–1,800 kWh/m²/yr |

| Saint-Pierre-et-Miquelon | ZNI | 6,000 | 100% renewable by 2030 | 900–1,100 kWh/m²/yr |

ZNI = Zone Non-Interconnectée. DOM = Département d’Outre-Mer. COM = Collectivité d’Outre-Mer.

ZNI Electricity Economics — Why Off-Grid Solar Wins

ZNI territory economics differ from metropolitan France. Island electricity is generated primarily by diesel and heavy fuel oil, making conventional grid power expensive:

| Territory | Average Grid Electricity Price | Comparison to Metropolitan France |

|---|---|---|

| La Réunion | €0.18–0.22/kWh (subsidized) | ~50% above metropolitan average |

| Guadeloupe | €0.17–0.21/kWh | ~45% above |

| Martinique | €0.17–0.20/kWh | ~40% above |

| Guyane (rural) | €0.22–0.35/kWh | Up to 2× metropolitan |

| Corsica | €0.16–0.20/kWh | ~35% above |

Prices reflect TURPE (grid tariff) + generation component. Rural and isolated areas in Guyane may pay significantly more.

The high cost of island electricity means off-grid solar + battery systems achieve payback periods of 3–6 years in ZNI contexts, considerably shorter than equivalent metropolitan installations.

La Réunion: France’s Most Advanced Island Energy Transition

La Réunion is the furthest along of any ZNI territory in its renewable transition:

- Renewable share (2024): ~42% of electricity

- Solar installed: ~600 MW

- Storage (grid-connected): ~180 MWh

- Target: 100% renewable by 2030 (all-source)

EDF SEI (the island operator) has deployed battery storage alongside solar to manage intermittency. Other ZNI territories are now following the same approach.

Pro Tip — ZNI CRE Tender Track

CRE runs dedicated tender rounds for ZNI projects. These tenders typically achieve higher strike prices (€100–180/MWh) than metropolitan rounds because they price in island generation costs. Solar developers who enter the ZNI market early face less competition than in metropolitan France — but must navigate EDF SEI grid integration requirements specific to each island’s electricity system.

Corsica (Corse) — A Distinct Off-Grid Ecosystem

Corsica occupies a unique position: it is geographically close to metropolitan France but operates as a ZNI due to limited submarine cable capacity. The island has a combination of grid-connected solar (CRE-tendered) and true off-grid installations serving isolated farms and villages in the interior mountain regions.

Corsica solar characteristics:

- High irradiance (1,500–1,800 kWh/m²/yr)

- Mountainous terrain limiting ground-mount development

- Strong agri-tourism sector driving rooftop + off-grid demand

- EDF SEI manages the island network with solar integration priority

- Isolated interior communes (villages) increasingly served by mini-grid solar rather than grid extension

The island’s renewable target is 40% by 2030 — conservative compared to other DOM-TOM territories, reflecting grid stability constraints and lower diesel dependence due to hydro resources.

Rural Metropolitan France — Isolated Farm and Agricultural Off-Grid

In metropolitan France, off-grid solar is driven primarily by economics of grid connection. The cost of extending the low-voltage grid to an isolated property in rural France typically runs €5,000–€15,000 per kilometer — sometimes more in mountainous terrain.

For isolated farms and rural residences more than 2–5 km from the nearest grid connection point, off-grid solar + battery systems are often the most cost-effective electricity supply solution:

| System Configuration | Typical Application | Cost Range |

|---|---|---|

| 3–6 kWp solar + 10–20 kWh battery | Isolated rural home | €15,000–€25,000 |

| 6–15 kWp solar + 20–40 kWh battery + generator backup | Working farm (low load) | €25,000–€50,000 |

| 15–50 kWp solar + 50–150 kWh battery + generator | Agricultural operation | €60,000–€150,000 |

| Custom mini-grid | Isolated hamlet (5–20 properties) | €200,000–€600,000 |

Off-Grid Solar Regulations in France

France’s regulatory framework for off-grid solar differs from grid-connected installations:

Metropolitan France (isolated installations):

- No grid connection = no CRE regulatory obligation

- No MaStR-equivalent registration required

- No feed-in tariff (by definition — no grid connection)

- Installations subject to standard building codes (permis de construire or déclaration préalable above certain sizes)

- Battery system safety standards: NF EN IEC 62619 for Li-ion batteries

- RGE-certified installer recommended but not legally mandatory for off-grid residential

ZNI territories:

- Grid-connected off-grid-capable systems (hybrid) fall under CRE ZNI tender framework

- True off-grid in rural ZNI areas is encouraged by ADEME through direct grants

- ADEME’s Fond Chaleur and island energy programs co-finance off-grid systems in underserved areas

- EDF SEI has preferential connection terms for hybrid systems that can island-operate

Key Takeaway — France Off-Grid Solar Opportunity

The France off-grid solar market is growing across two vectors simultaneously: ZNI island territories where government policy mandates renewable transition, and isolated rural France where grid extension economics increasingly favor standalone solar. Solar professionals using solar design software capable of off-grid and hybrid system modeling — including battery sizing and backup generator integration — have a structural advantage in both segments.

CRE Solar Auctions: France’s Appels d’Offres Framework

The Commission de Régulation de l’Énergie (CRE) manages France’s primary solar support mechanism for projects above 100 kWp. Any solar developer operating in France needs to understand how it works.

How CRE Tenders Work

CRE auctions operate as contract for difference (CFD) tenders. Winning projects receive:

- A 20-year contract with a fixed “strike price” — the reference tariff

- If wholesale electricity prices fall below the strike price, the state pays the difference

- If wholesale prices exceed the strike price, the developer repays the excess to the state

This provides revenue certainty regardless of wholesale market volatility — a protection that proved its value during the 2021–2023 energy crisis when wholesale prices swung from €50/MWh to over €500/MWh.

CRE Tender Categories — 2025–2026

| Tender Category | Eligible Capacity | 2025 Volume Awarded | Avg. Strike Price |

|---|---|---|---|

| Ground-mount (AO Sol) | >1 MWp | ~1.3 GW | €58/MWh |

| Rooftop large (AOTPV) | 500 kWp – 10 MWp | ~0.6 GW | €78/MWh |

| Rooftop small (simplified) | 100–500 kWp | ~0.8 GW | €88/MWh |

| Agri-PV | Any size (CRE track) | ~0.4 GW | €102/MWh |

| Floating solar | Any size | ~0.1 GW | €95/MWh |

| ZNI (island territories) | Territory-specific | ~0.25 GW | €120–175/MWh |

| Total 2025 | ~3.5 GW | — |

Sources: CRE official tender results, SER, 2025 data.

CRE Tender Price Trend — Ground-Mount France

| Year | Average Awarded Price (Ground-Mount) |

|---|---|

| 2019 | €87/MWh |

| 2020 | €76/MWh |

| 2021 | €68/MWh |

| 2022 | €62/MWh |

| 2023 | €60/MWh |

| 2024 | €58/MWh |

| 2025 | ~€56/MWh |

Awarded prices have fallen every year, tracking module cost declines, better project finance terms, and more competition. Ground-mount solar is now approaching grid parity in southern France — projects with high irradiance and low construction costs can compete as merchant plants without CRE contracts.

Winning a CRE Bid — Key Requirements

Documentation requirements:

- Environmental impact assessment (étude d’impact) for projects >5 MWp

- Building permit (permis de construire) or development authorization

- Grid connection offer from RTE or local DSO

- Technical plan certified by a bureau de contrôle

- Financial guarantee (caution bancaire) — typically 5–10% of project value

- Land lease or ownership documentation

Scoring criteria:

- Price (primary factor — lowest bid wins, within a price cap)

- Carbon content of equipment (bonus for European-manufactured panels)

- Environmental quality (biodiversity impact scoring)

- Social criteria (local employment commitments)

The carbon content scoring, introduced under the AER law, gives a competitive advantage to projects using European or high-transparency-certified modules. Factor this into procurement strategy and proposal development.

Pro Tip — CRE Bid Accuracy

CRE bids are binding price commitments for 20 years. Errors in yield projections directly affect project economics over two decades. Using bankable solar shadow analysis software that accounts for seasonal shading, terrain effects, and module degradation is not optional for CRE-tender projects — it is due diligence. A 5% yield overestimation on a 10 MW project represents €1–2 million in revenue shortfall over 20 years at €60/MWh.

Autoconsommation: France’s Self-Consumption Policy Framework

France’s autoconsommation (self-consumption) framework differs from Germany’s or Italy’s. Solar producers consume their own generation and sell surplus to the grid through specific administrative and metering structures.

Individual Autoconsommation (Autoconsommation Individuelle)

Individual autoconsommation applies to a single producer consuming solar electricity at the same grid connection point.

Key features:

- Available for all system sizes

- Surplus injection to grid is automatic and metered

- Feed-in premium (S21 tariff) available for systems up to 500 kWp

- No net metering — physical injection only

- Bidir metering (compteur bidirectionnel Linky) required

S21 Feed-in Premium Rates (Q1 2026):

| System Size | S21 Premium (€/kWh) | Duration |

|---|---|---|

| ≤3 kWp | €0.1374 | 20 years |

| 3–9 kWp | €0.1186 | 20 years |

| 9–36 kWp | €0.0800 | 20 years |

| 36–100 kWp | €0.0770 | 20 years |

| 100–500 kWp | €0.0730 | 20 years |

Rates as of Q1 2026. Updated quarterly by the Ministry of Energy. Source: DGEC (Direction Générale de l’Énergie et du Climat).

Collective Autoconsommation (Autoconsommation Collective)

Collective autoconsommation allows a group of producers and consumers to share solar generation within a defined geographic perimeter. It applies to:

- Multi-unit residential buildings

- Industrial parks and business campuses

- Rural communes sharing a mini-grid solar installation

Operational framework:

- Maximum total production capacity: originally 3 MWp, extended to 100 MWp under the AER law (2023)

- Geographic perimeter: within the same low-voltage or medium-voltage network area

- Legal structure: requires an organisateur (organizing entity) responsible for distribution keys

- Surplus export: permitted at S21 rates

- Administrative registration: with the regional network operator (Enedis in most of France)

Key Takeaway — Autoconsommation Collective Expansion

The AER law’s expansion of collective autoconsommation to 100 MWp opens significant opportunities for community solar and industrial campus projects. A 5 MW solar farm shared across a business park of 30 companies can qualify for collective autoconsommation — combining S21 premium revenue with direct electricity cost reduction for all participants. This is a growing commercial solar segment in 2026.

Nuclear Coexistence: How France’s Baseload Shapes Solar Economics

France is Europe’s most nuclear-dependent economy — nuclear supplies approximately 70% of electricity generation. That shapes solar market dynamics in ways that don’t apply anywhere else in Europe.

How Nuclear Affects Solar Pricing

France’s nuclear fleet produces approximately 300–360 TWh per year at marginal costs of around €10–25/MWh, which depresses average wholesale electricity prices. France’s EPEX Spot Day-Ahead price averaged €40–60/MWh in years of normal nuclear output (2015–2020), well below Germany or Italy.

Low wholesale prices compress merchant solar economics. This is why France’s solar market is built around CRE contract-for-difference support — the strike price protects solar developers from low-price environments without locking in high consumer costs.

The 2021–2024 Nuclear Disruption

France’s nuclear advantage became a vulnerability during 2021–2024. Stress-corrosion cracking in reactor cooling circuits led to simultaneous shutdowns of up to 32 reactors (out of 56), cutting nuclear output by nearly 40% and turning France from electricity exporter to importer.

French wholesale electricity prices peaked above €1,000/MWh in August 2022. The disruption had three concrete effects on solar economics:

- Merchant solar became highly profitable — uncontracted solar assets earned exceptional returns in 2022–2023

- CRE contracts clawed back the windfall — developers with 20-year contracts at €58/MWh missed the price spike because the CFD mechanism required repaying excess profits above the strike price

- The grid resilience case for distributed solar hardened — France’s concentrated nuclear production created systemic risk that decentralized solar does not

Nuclear Coexistence — The Complementarity Case

The technical case for nuclear-solar coexistence is straightforward. Nuclear provides stable baseload (7,000–8,000 full-load hours annually). Solar provides peak-demand midday power (4–5 peak hours daily in summer). The generation profiles complement rather than compete:

| Time | Nuclear Output | Solar Output | Combined Grid Effect |

|---|---|---|---|

| 06:00–08:00 | High | Rising | Morning ramp managed |

| 10:00–14:00 | Moderate (partial load) | Peak | Solar reduces nuclear dispatch |

| 16:00–20:00 | Increasing | Declining | Evening ramp — nuclear ramps up |

| 22:00–06:00 | Baseload (high) | Zero | Nuclear export / storage charging |

This reduces curtailment risk for solar, a real concern in markets with high renewable penetration such as Spain and Germany. France’s nuclear baseload absorbs nighttime and winter demand, letting solar fill peak hours without triggering grid stability issues at current penetration levels.

Looking ahead to 100 GW: At 100 GW of solar penetration (producing ~100 TWh annually), France will need storage — batteries, pumped hydro, hydrogen — to manage the midday generation surplus. This is a structural driver of the French battery storage market through 2030.

Win More France Solar Projects with Accurate Yield Models

SurgePV’s solar design and financial modeling tools are built for European solar markets — including France’s CRE tender requirements, autoconsommation S21 rate calculations, and off-grid battery sizing for ZNI territories.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

Commercial and Industrial Solar in France

The C&I Solar Opportunity in France

Commercial and industrial (C&I) solar is the fastest-growing segment in France’s PV market. Four factors drive this in 2025–2026:

- Energy cost pressure: Post-2021 crisis energy prices remain elevated and C&I buyers want cost certainty

- PPE3 carport mandate: Large parking operators must install solar canopies under the 2023 law

- Corporate PPA growth: French multinationals including Stellantis, Renault, Saint-Gobain, and Air Liquide have signed or are tendering solar PPAs

- RE2020 compliance: New commercial buildings must meet energy performance standards that include solar integration

C&I Solar System Economics — France 2026

| System Size | Application | All-in Cost (€/kWp) | Typical Annual Yield | Simple Payback |

|---|---|---|---|---|

| 100–500 kWp | Industrial rooftop | €900–1,200 | 950–1,400 kWh/kWp | 7–12 years (autoconsommation) |

| 500 kWp–5 MWp | Large logistics/manufacturing | €780–1,050 | 1,000–1,500 kWh/kWp | 6–10 years |

| 5–50 MWp (CRE) | Ground-mount with contract | €700–900 | 1,100–1,700 kWh/kWp | 8–15 years (CFD-backed) |

| Carport (100–1,000 spaces) | Parking canopy | €1,100–1,600 | 900–1,300 kWh/kWp | 8–14 years |

Payback assumes 60–75% self-consumption at €0.18/kWh avoided cost, surplus exported at S21 rates. Southern France assumptions for irradiance.

Corporate PPAs in France

The French corporate PPA market has grown rapidly since 2022. Core terms:

- Offtaker signs a 10–20 year fixed price contract with a solar developer

- Developer builds, owns, and operates the plant

- Electricity settled virtually (financial) or delivered physically via dedicated grid connection

- Typical PPA price: €55–80/MWh fixed over term, versus current market prices of €60–120/MWh variable

- No CRE contract required for projects without public support

Major signatories include LVMH (120 MW), Stellantis (500 MW multi-country), and Carrefour (rooftop portfolio). This segment bypasses CRE tenders entirely, making speed to market and bankable yield models the main differentiators for developers.

The Carport Solar Mandate

France’s loi relative à l’accélération de la production des énergies renouvelables (March 2023) includes a provision requiring solar canopies on parking facilities with more than 80 spaces by 2028:

- Car parks with 80–400 spaces: 50% coverage by 2028

- Car parks with 400+ spaces: 50% coverage by 2026 (already in force)

- Exemptions: historic buildings, archaeological sites, severe structural constraints

The mandate affects an estimated 130,000 car parks across France, representing approximately 11 GW of potential capacity.

Solar companies targeting mandatory compliance projects need solar proposal software that can generate detailed carport solar proposals — structural modeling and shading analysis included.

Regional Solar: Nord vs Sud — Irradiance and Deployment Strategies

Irradiance Map — Metropolitan France

Solar irradiance in metropolitan France varies by nearly 2:1 between the far north and the Mediterranean coast:

| Region | Annual Irradiance | Peak Sun Hours/Day | Best System Types |

|---|---|---|---|

| Hauts-de-France (Lille) | 1,000–1,100 kWh/m²/yr | 2.7–3.0 | Rooftop, east-west flat roof |

| Normandie | 1,050–1,150 kWh/m²/yr | 2.9–3.1 | Rooftop, carport |

| Île-de-France (Paris) | 1,100–1,250 kWh/m²/yr | 3.0–3.4 | Rooftop, BIPV, carport |

| Grand Est (Strasbourg) | 1,150–1,350 kWh/m²/yr | 3.1–3.7 | Rooftop, ground-mount |

| Bretagne | 1,100–1,300 kWh/m²/yr | 3.0–3.6 | Rooftop, agricultural |

| Centre-Val de Loire | 1,250–1,400 kWh/m²/yr | 3.4–3.8 | Ground-mount, agri-PV |

| Auvergne-Rhône-Alpes | 1,350–1,600 kWh/m²/yr | 3.7–4.4 | Agri-PV, ground-mount |

| Nouvelle-Aquitaine | 1,450–1,700 kWh/m²/yr | 4.0–4.7 | All types; agri-PV (wine/maize) |

| Occitanie | 1,550–1,800 kWh/m²/yr | 4.3–4.9 | Ground-mount, agri-PV, floating |

| PACA (Marseille, Nice) | 1,650–1,900 kWh/m²/yr | 4.5–5.2 | Ground-mount, BIPV, floating |

Nord Strategy vs Sud Strategy

Northern France (below 1,300 kWh/m²/yr):

- Prioritize high self-consumption rate — northern irradiance makes export economics weak

- Flat rooftop east-west arrays push more generation into morning and evening, matching commercial consumption profiles better than south-facing

- Autoconsommation collective aggregates small producers into economically viable projects

- Agri-PV with east-west configurations narrows the seasonal yield gap

Southern France (above 1,400 kWh/m²/yr):

- Ground-mount and agri-PV at scale work without S21 premiums in the best irradiance zones

- CRE ground-mount tenders at €55–65/MWh pencil out at system costs under €900/kWp

- Higher curtailment risk at midday peak — battery storage increasingly relevant

- Agri-PV bifacial tracking structures deliver high yield with agricultural flexibility

Pro Tip — Shading Matters Most in the North

In northern France where irradiance is already limited, shading losses from chimneys, dormers, and neighboring buildings have an outsized economic impact. A 15% shading loss in Hauts-de-France reduces annual yield by 150–165 kWh/kWp — meaningfully affecting S21 premium economics over a 20-year contract. Accurate pre-installation shading analysis using solar shadow analysis software is critical for northern France rooftop projects.

ROI Examples: France Solar With CRE and Autoconsommation

Example 1: Industrial Rooftop — Occitanie (300 kWp, Autoconsommation)

| Parameter | Value |

|---|---|

| System size | 300 kWp |

| Annual irradiance | 1,680 kWh/m²/yr |

| Estimated annual yield | 420,000 kWh |

| Self-consumption rate | 70% |

| Self-consumed kWh (annual) | 294,000 kWh |

| Surplus exported (annual) | 126,000 kWh |

| Electricity avoided cost | €0.18/kWh |

| S21 export premium | €0.077/kWh |

| Annual electricity savings | €52,920 |

| Annual S21 income | €9,702 |

| Total annual benefit | €62,622 |

| System cost (€1,050/kWp) | €315,000 |

| Simple payback | ~5.0 years |

Example 2: Ground-Mount CRE Project — Nouvelle-Aquitaine (5 MWp)

| Parameter | Value |

|---|---|

| System size | 5 MWp |

| Annual yield | 7,500,000 kWh |

| CRE strike price | €60/MWh |

| Annual CRE revenue | €450,000 |

| Annual O&M costs | ~€35,000 |

| Net annual income | €415,000 |

| Total project cost (€870/kWp) | €4,350,000 |

| Project finance (70% debt) | €3,045,000 |

| Equity invested | €1,305,000 |

| Equity IRR (levered, 20yr) | ~11–13% |

Example 3: Off-Grid Farm — Rural Corrèze (Metropolitan France)

| Parameter | Value |

|---|---|

| System size | 10 kWp solar + 30 kWh battery |

| Annual yield | 11,500 kWh |

| Grid alternative cost | €12,000 (grid connection estimate) + €0.20/kWh ongoing |

| Off-grid system cost | €28,000 |

| Annual diesel generator saving | €2,400 |

| Annual grid-equivalent saving | €3,800 |

| Total annual saving vs alternatives | ~€4,200 |

| Effective payback | ~6.7 years |

Modeling off-grid scenarios accurately — battery state of charge simulations, generator backup hours, load profiles — requires the detailed energy flow analysis built into purpose-designed solar software.

France Solar 2026 Investment Outlook

Tailwinds for 2026–2028

- PPE3 tender volumes: CRE has signaled 6 GW of tender volume in 2026 across all categories, the highest in French history

- AER law implementation: ZAEnR zone designation is accelerating in municipalities, improving land access

- Module cost stability: Panel prices stabilized at historic lows (€0.10–0.15/Wp for commodity modules)

- Corporate demand: PPA market growing 40–60% annually as French companies pursue Scope 2 decarbonization targets

- Grid storage investment: RTE’s “Futurs Énergétiques 2050” scenario requires 10–20 GWh of storage by 2030, which supports hybrid solar+storage project economics

Headwinds and Risks

- Grid connection queues: RTE’s 200+ GW backlog is the largest single bottleneck

- Permitting complexity: Outside ZAEnR zones, permitting for large ground-mount projects runs 3–5 years

- Labor shortage: Installer capacity is the binding constraint for residential and C&I segments

- Module carbon content rule: AER law bonus scoring for European modules may disadvantage projects sourcing Chinese supply chains

Target Market for Solar Companies in France

| Segment | 2026 Opportunity | Key Requirement |

|---|---|---|

| C&I rooftop (100–1,000 kWp) | High — fastest CRE queue, strong S21 economics | Bankable design, S21 admin |

| Carport solar | Mandatory demand, ~11 GW pipeline | Structural + shadow modeling |

| Off-grid ZNI | High IRR, less competition | Island-specific system design |

| Agri-PV (20–500 kWp) | Growing CRE track, farm partnerships | Agricultural productivity modeling |

| Ground-mount (>1 MWp) | Large volume, grid queue risk | Environmental studies, CRE bid accuracy |

Conclusion

France’s green energy transition is real, ambitious, and operationally behind schedule. Closing the gap to 100 GW by 2030 requires solving three structural problems — permitting, grid connection, and installer capacity — at the same time.

The 2026 market is the largest opportunity in French PV history. Capturing it requires understanding the specifics: CRE bid precision, autoconsommation S21 optimization, off-grid ZNI economics, and agri-PV regulatory requirements all differ from other European markets.

Three priorities for France solar in 2026:

- Target the C&I and carport segment — shortest regulatory timelines, strong economics, mandatory compliance driving demand

- Explore ZNI off-grid market — lower competition, higher returns, aligned with island renewable mandates

- Invest in yield model accuracy — France’s 20-year CRE contracts make yield errors enormously costly over project lifetime

For European solar policy context, see our guides on EU solar energy policies and European solar incentives. For solar project financial modeling in France and across Europe, explore the generation financial tool at SurgePV.

Frequently Asked Questions

What is France’s solar capacity target for 2030?

France’s Programmation Pluriannuelle de l’Énergie (PPE3) sets a national solar photovoltaic target of 100 GW by 2030, up from approximately 22 GW installed at end of 2024. This represents a near five-fold increase over six years, requiring annual additions of 12–15 GW — significantly above the current deployment rate of approximately 3 GW per year. PPE3 includes intermediate milestones of 45 GW by 2026 and 75 GW by 2028.

What is the Loi Énergie-Climat and how does it affect solar in France?

The Loi Énergie-Climat (LEC), enacted in November 2019, commits France to carbon neutrality by 2050 and 40% renewable electricity by 2030. For solar, the LEC established the PPE as a binding planning instrument and underpins the CRE competitive tender framework. The updated PPE3 (2024) raised the solar target to 100 GW, making it the largest solar expansion program in French history.

What is France’s off-grid solar market and where is it most active?

The France off-grid solar market is concentrated in two areas: overseas island territories (ZNI — La Réunion, Guadeloupe, Martinique, Guyane, Mayotte, Corsica), where high electricity costs and strong irradiance make off-grid solar competitive; and isolated rural metropolitan France, where grid connection costs of €5,000–€15,000/km make standalone solar systems cheaper than grid extension. La Réunion (600 MW installed, targeting 100% renewable by 2030) is the most advanced ZNI market.

How do CRE solar auctions work in France?

CRE organizes competitive tender rounds for solar projects above 100 kWp. Winners receive a 20-year contract for difference — a fixed strike price supplemented by state payments when wholesale prices fall below the contracted level. 2025 tenders awarded approximately 3.5 GW across ground-mount (avg. €58/MWh), large rooftop (€78/MWh), small rooftop simplified (€88/MWh), agri-PV (€102/MWh), and ZNI tracks (€120–175/MWh).

What is autoconsommation (self-consumption) policy in France?

Individual autoconsommation allows solar producers to consume their own generation at the same grid connection point and sell surplus at S21 feed-in premium rates (€0.073–€0.137/kWh depending on system size). Collective autoconsommation — expanded to 100 MWp by the AER law — allows groups of producers and consumers within a geographic perimeter to share solar generation. Virtual net metering is not available; physical metering of production and injection is required.

How does France’s nuclear base affect solar economics?

France’s ~70% nuclear electricity share historically depressed wholesale electricity prices (avg. €40–60/MWh in normal nuclear years), making merchant solar economics challenging. This is why France’s solar market is built around CRE contract-for-difference support rather than merchant exposure. The nuclear disruption of 2021–2024, when corrosion issues shut down up to 32 reactors simultaneously, showed that CFD contracts protect solar developers on both sides: they cap upside windfall clawback while guaranteeing floor revenue.

What solar regions have the highest irradiance in France?

Provence-Alpes-Côte d’Azur (1,650–1,900 kWh/m²/yr) and Occitanie (1,550–1,800 kWh/m²/yr) are France’s highest-irradiance metropolitan regions. Overseas territories exceed these: La Réunion and Martinique reach 1,800–2,100 kWh/m²/yr. Northern France (Hauts-de-France, Normandie) averages 1,000–1,150 kWh/m²/yr — the lowest in metropolitan France but still viable for rooftop and autoconsommation-optimized C&I projects.

What is the PPE France solar framework?

The Programmation Pluriannuelle de l’Énergie (PPE) is France’s multiannual energy planning instrument, updated every five years. PPE3 (2024–2033) is the current framework. It sets capacity targets by technology (100 GW solar by 2030), defines annual CRE tender volumes (6 GW in 2026), and specifies technology-specific targets (10 GW agri-PV, 1 GW floating solar). PPE3 also integrates the AER law’s acceleration zone framework and island territory renewable targets.