Tax incentives are the most powerful financial lever available to solar installers, developers, and property owners across Europe in 2026. In a market where a residential 8 kWp system costs €9,000–€12,000 before incentives, the difference between a 7-year payback and a 10-year payback often comes down entirely to which tax relief programs you claim — and whether you claim them correctly.

This is not merely an academic point. Across Europe’s major solar markets, effective tax relief now routinely reduces net installation cost by 20–55% when structured properly. Germany’s 0% VAT eliminates €1,400–€2,000 in tax on a typical residential system. Italy’s 50% income tax deduction cuts net cost nearly in half over 10 years. France’s reduced TVA and MaPrimeRénov’ grants together make sub-5-year payback achievable in the south. And across all these markets, the solar installer who can walk a customer through the numbers — precisely, credibly, and quickly — closes more business.

That is where solar design software that integrates financial modeling earns its keep. Understanding the incentive frameworks is the foundation. Building them into a professional proposal is what converts the understanding into closed deals.

TL;DR — European Solar Tax Credits 2026

Nine or more EU member states now apply 0% VAT on residential solar panels under the 2022 EU VAT Directive amendment. Germany offers 0% MwSt plus income tax exemption for small systems. Italy’s Detrazione Fiscale 50% remains active. France applies TVA 5.5% and MaPrimeRénov’ grants. Spain’s autonomous communities offer 15–50% regional deductions. The Netherlands and Belgium apply 0% BTW. The UK applies 0% VAT on solar under its energy-saving materials rules. Poland offers PIT termomodernizacja relief. Stacking with grants and feed-in programs is possible but requires careful compliance.

In this guide:

- Latest 2026 update table: VAT rates and deduction rates by country

- EU-wide 0% VAT directive: which countries have adopted it

- Germany: 0% MwSt for residential PV + income tax exemption rules

- Italy: Detrazione Fiscale 50% — eligibility, claim process, and limits

- France: TVA 5.5% reduced rate + MaPrimeRénov’ crédit impôt interaction

- Spain: deducción autonómica — regional variations by community

- Netherlands: 0% BTW on residential solar + SDE++ feed-in support

- UK: 0% VAT on energy-saving materials — scope and limitations

- Poland: PIT termomodernizacja relief + heat pump integration

- How to claim: documentation requirements across jurisdictions

- How stacking tax relief with grants works — cumulation rules explained

- Worked example: 8 kWp residential system, net cost after credits

Latest Updates: European Solar Tax Policy 2026

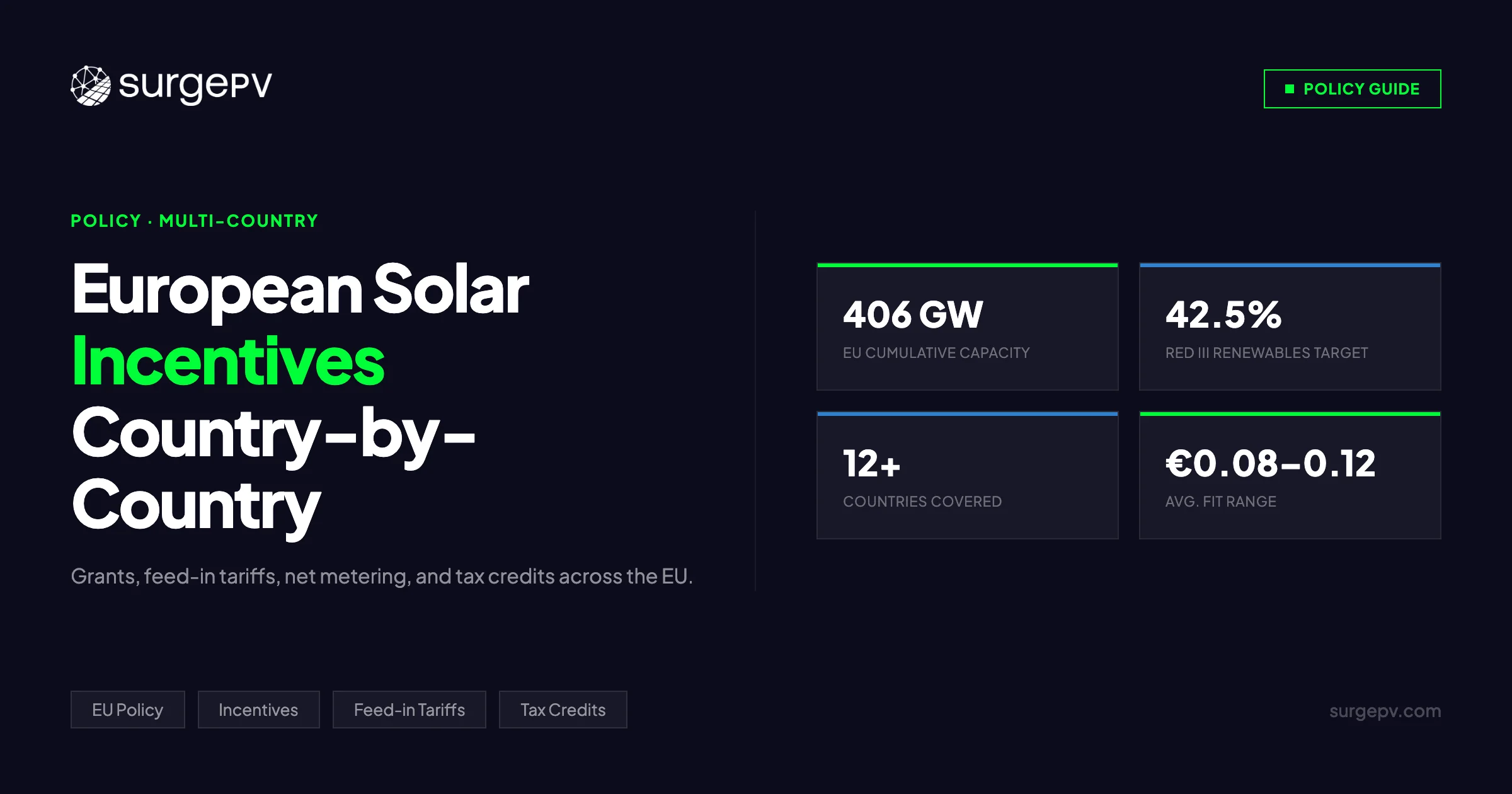

The European solar tax environment changed decisively between 2022 and 2024. The EU VAT Directive amendment of April 2022 gave member states explicit authority to apply 0% VAT to solar panels, heat pumps, and heat pump water heaters. Most major markets moved within 18 months. The result is the most favorable tax environment for solar in European history — but the specific rules, caps, and claim processes differ by country in ways that matter substantially to project economics.

European Solar Tax Credit & VAT Rate Summary — March 2026

| Country | VAT / GST Rate on Solar | Key Tax Deduction / Credit | Income Tax Relief | Status |

|---|---|---|---|---|

| Germany | 0% MwSt (from Jan 2023) | None additional | Vereinfachungsregelung (≤30 kWp exempt from profit tax) | Active |

| Italy | 10% IVA (residential install) | 50% Detrazione Fiscale | 10-year income tax deduction | Active |

| France | 5.5% TVA (residential) | MaPrimeRénov’ grant (not tax credit) | No direct income tax credit | Active |

| Spain | 21% IVA (standard) | Deducción autonómica 15–50% (varies by region) | Regional income tax deduction | Active (varies) |

| Netherlands | 0% BTW (from Jan 2023) | SDE++ feed-in premium | None additional | Active |

| Belgium | 0% TVA/BTW (from Apr 2023) | Flemish and Walloon grants | None federal | Active |

| United Kingdom | 0% VAT (Energy Saving Materials) | Smart Export Guarantee (tariff) | None additional | Active |

| Poland | 8% VAT (PV under 300 kW) | Termomodernizacja PIT relief | Up to PLN 53,000 deduction | Active |

| Austria | 0% MwSt (from Jan 2024, ≤35 kWp) | Investment grant (Investitionsprämie) | None additional | Active |

| Sweden | 20% reduced credit offset | ROT deduction 30% (labor costs) | 30% labor cost credit | Active |

| Portugal | 6% IVA (residential) | SERUP rebates (varies) | None direct | Active |

| Czech Republic | 0% DPH (from Jan 2024) | No direct tax deduction | None additional | Active |

Sources: European Commission VAT rules database, national tax authority guidance as of Q1 2026. Installer VAT rules may differ from product-only purchases — always verify with a local tax advisor.

Key 2024–2026 Changes at a Glance

EU 0% VAT expansion continues. Austria moved to 0% MwSt for PV systems up to 35 kWp from January 2024. Czech Republic implemented 0% DPH for solar in early 2024. As of Q1 2026, nine EU member states have adopted the 0% rate permitted under the 2022 directive.

Germany’s Vereinfachungsregelung simplified significantly. From 2023, residential PV operators with systems up to 30 kWp are fully exempt from income tax on solar production — no complex EÜR filing required. This resolves years of administrative burden and has been extended with no sunset date as of 2026.

Italy’s Superbonus is closed; Detrazione Fiscale 50% remains the primary vehicle. The phase-down of Superbonus (110% → 90% → 70% → 65%) ended new PV applications. The 50% deduction over 10 years remains fully active and is now the standard framing for all Italian residential solar financing.

UK 0% VAT extended beyond the original sunset. The UK government’s decision to make 0% VAT permanent on energy-saving materials (rather than reverting to 5% in 2027) provides long-term planning certainty for UK installers.

Key Takeaway — Incentive Landscape as of 2026

VAT reduction or elimination is now the baseline across most of Western Europe. The differentiating factor — and where real money is either captured or left on the table — is in the income tax deduction and grant stacking layer. A 6 kWp system that costs €7,200 in Germany at 0% VAT still has an additional income tax optimization pathway under the Vereinfachungsregelung. In Italy, the same system has a 50% deduction that reduces net cost to effectively €3,600 over 10 years. These second-layer incentives are where installers and financial advisors must spend more time.

EU-Wide 0% VAT Directive: Which Countries Have Adopted It

The 2022 amendment to the EU VAT Directive (Council Directive 2006/112/EC, as amended by Directive 2022/542/EU) created an explicit authorization for EU member states to apply a zero VAT rate to supplies and installation of solar panels. The relevant provision covers:

- Solar panels installed on, or in the vicinity of, private dwellings, housing, and public interest buildings

- Heat pumps

- Wind turbines for residential use

Critically, each member state must actively implement the 0% rate in its own national legislation. The EU directive only authorizes the rate — it does not mandate it. Implementation is therefore uneven across the bloc.

Countries That Have Adopted 0% VAT on Residential Solar

| Country | Implementation Date | Cap / Conditions |

|---|---|---|

| Germany | 1 January 2023 | Systems up to 30 kWp (or 15 kWp per unit in multi-family buildings) |

| Netherlands | 1 January 2023 | Residential property owners only |

| Belgium | 1 April 2023 | Dwellings over 10 years old; professional installation required |

| Estonia | 1 May 2023 | All residential PV systems |

| Lithuania | 2023 | Residential; size conditions apply |

| Austria | 1 January 2024 | Systems up to 35 kWp |

| Czech Republic | January 2024 | Systems under 50 kW |

| Latvia | 2024 | Residential installations |

| Denmark | Partial (reduced rate) | Moved from 25% standard to reduced rate for labor |

Countries that have not yet adopted 0% (as of Q1 2026) include France (maintaining 5.5% TVA as a reduced rate rather than 0%), Spain (still applying standard 21% IVA at national level, with deductions handled at income tax level), and Italy (applying 10% IVA on installation, with the incentive delivered via deduction rather than point-of-sale tax relief).

Pro Tip — VAT Reclaim vs. Zero-Rating

In countries where 0% VAT applies, the benefit is immediate — the customer simply does not pay VAT at point of purchase. This is far more valuable from a cash-flow perspective than a deduction claimed over 10 years. When presenting project economics in Germany or the Netherlands, make sure your solar design software outputs reflect the 0% VAT gross system cost as the baseline, not a pre-incentive figure that includes 19% or 21% VAT. The difference can mislead customers into underestimating the attractiveness of the deal.

Germany: 0% MwSt for Rooftop PV + Income Tax Simplification

Germany is arguably the most consequential single solar market in Europe and has the cleanest incentive structure for residential systems as of 2026. Two separate mechanisms work in parallel.

VAT Relief: 0% MwSt Since January 2023

From 1 January 2023, Germany applies a 0% Mehrwertsteuer (MwSt) rate to:

- The supply of solar modules (panels)

- The supply and installation of essential components: inverters, battery storage systems directly connected to the PV system, mounting systems

- The supply and installation of EV chargers when installed in conjunction with a PV system

Qualifying condition: The system must be installed on or adjacent to private residential property, or on certain public interest buildings (hospitals, schools, municipalities). The total output of the system must not exceed 30 kWp (or 15 kWp per unit in buildings with multiple residential units up to a maximum of 100 kWp for the building).

How it applies: The 0% rate is applied automatically by the installer at the point of invoicing. No application, no claim form, no waiting period. The customer simply does not pay VAT on the invoice. For a typical 8 kWp residential system with a base cost of €9,600 (at €1,200/kWp), the savings at 0% vs. the standard 19% rate amounts to €1,824 in immediate VAT saving.

For larger systems (above 30 kWp): Standard 19% MwSt applies, but VAT is recoverable by VAT-registered businesses. Installers and solar businesses operating through a GmbH or UG structure can recover input VAT on procurement and installations, while charging output VAT on sales — effectively net-zero on a cash basis for compliant operators.

Income Tax: Vereinfachungsregelung (Simplification Rule)

Before 2023, German residential solar operators faced a labyrinthine decision: elect into Kleinunternehmer status (no VAT but no deductions), or register as VAT payers (input tax deduction on hardware, but administrative obligations). The 2023 Vereinfachungsregelung resolved this for small systems.

Under the current rules, income from operating a PV system with an output of up to 30 kWp (per unit) is entirely exempt from German income tax (Einkommensteuer) and trade tax (Gewerbesteuer). This applies regardless of the system’s actual annual electricity sales revenue.

Practical implications:

- Feed-in revenue paid by the grid operator (Netzbetreiber) under the Einspeisevergütung (feed-in tariff) scheme is not reportable as taxable income

- The operator does not need to file an EÜR (Einnahmen-Überschuss-Rechnung) for the PV system

- Capital cost depreciation is irrelevant for small systems since there is no taxable profit to offset

For commercial systems (above 30 kWp): The Vereinfachungsregelung does not apply. Commercial operators can claim accelerated depreciation — typically 50% in year one under §7g EStG for qualifying business assets, with the remainder depreciated over the standard 20-year linear schedule. The effective first-year tax shield on a €150,000 commercial system is approximately €37,500 at a 25% effective corporate rate.

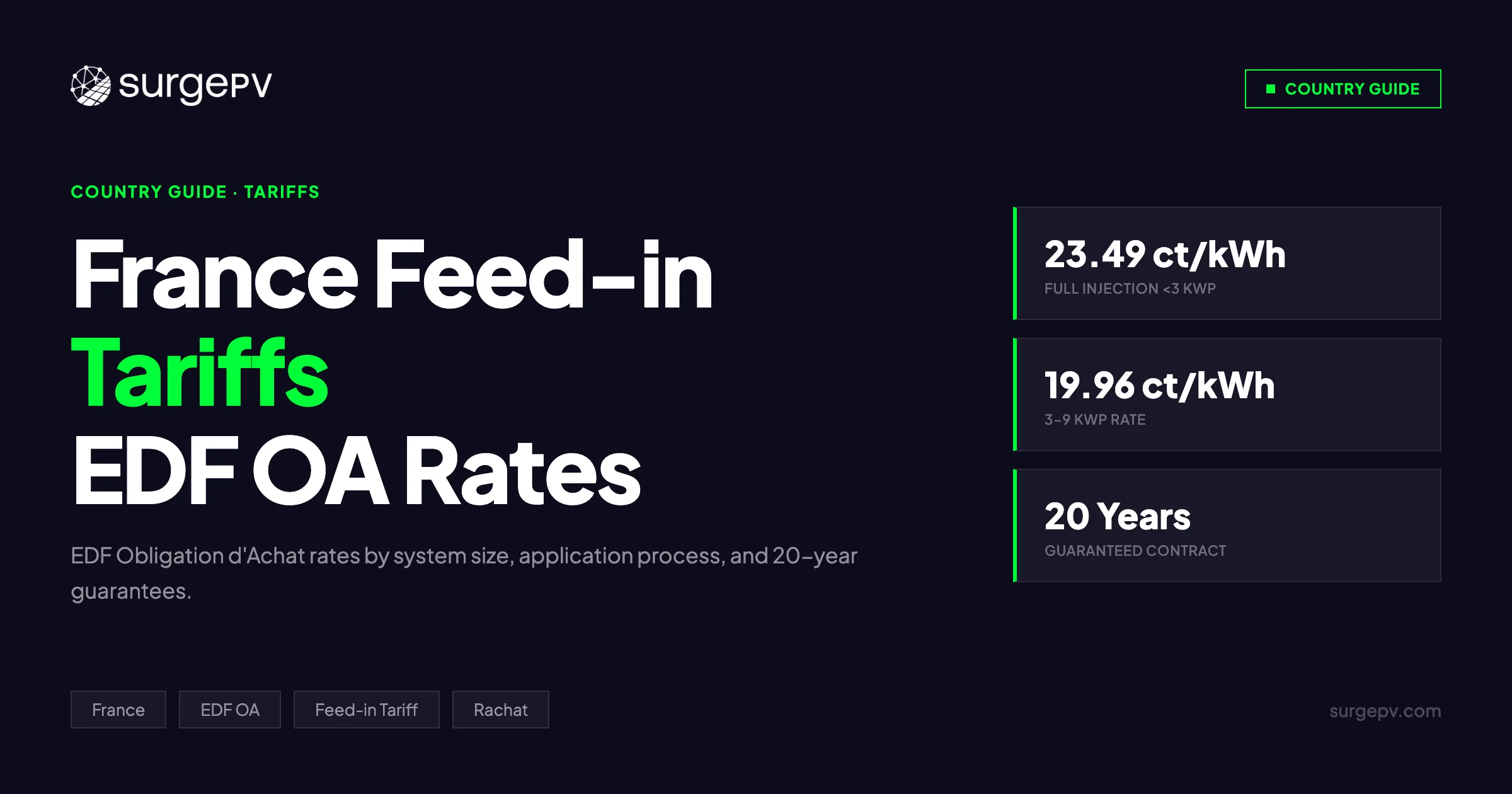

Einspeisevergütung: 2026 Feed-In Tariff Rates

Germany’s Erneuerbare-Energien-Gesetz (EEG) sets guaranteed feed-in tariff rates for systems connected to the grid. Rates are set semi-annually. As of Q1 2026:

| System Size | Full Feed-In Rate (kWp ≤ 10) | Partial Self-Consumption Rate |

|---|---|---|

| Up to 10 kWp | ~€0.082/kWh | ~€0.131/kWh |

| 10–40 kWp | ~€0.071/kWh | ~€0.110/kWh |

| 40–100 kWp | ~€0.057/kWh | ~€0.090/kWh |

Rates adjusted January 2026; check Bundesnetzagentur for current figures before quoting.

KfW Bank integration: Germany’s KfW development bank offers low-interest loans for solar and storage under the BEW (Bundesförderung für effiziente Wärmenetze) and renewable energy programs. Current rates (Q1 2026) are 3.05–4.25% fixed for 10-year terms — significantly below standard commercial lending rates. KfW financing can be combined with the Einspeisevergütung and the 0% VAT benefit simultaneously, without triggering cumulation restrictions.

For German installers and developers, having access to a solar software platform that models the Einspeisevergütung revenue correctly — by size tier, by year of commissioning, and accounting for self-consumption offsets — is essential for producing defensible ROI projections. See our generation and financial modeling tool for a worked example.

See also: Solar incentives and subsidies in Germany for a deeper dive into the BEW program and Länder-level grants.

Italy: Detrazione Fiscale 50% (Ecobonus)

Italy’s primary residential solar incentive in 2026 is the Detrazione Fiscale 50%, a 10-year income tax deduction on qualifying installation costs. The Superbonus 110% — once the headline program — is closed to new PV-only applications. The 50% deduction is the correct framework for any new residential solar project in Italy today.

See our full guide to solar incentives in Italy and the Superbonus phase-down for complete Superbonus history and transition rules.

How the Detrazione Fiscale 50% Works

The Detrazione Fiscale 50% allows homeowners to deduct 50% of qualifying solar installation costs directly from their Italian IRPEF (income tax) liability, spread equally over 10 consecutive tax years.

Qualifying expenses include:

- Solar PV panels (modules)

- Inverter (string or hybrid)

- Mounting and racking system

- DC/AC cabling and switchgear

- Battery storage (if installed together with the PV system)

- Labor costs for installation

- GSE registration fees

- Energy performance certification (APE), where required

Eligible parties:

- Natural persons who own (or have beneficial use of) the property where the system is installed

- Co-owners (deduction split proportionally)

- Tenants with landlord written consent

- Family members (coniuges, figli) resident in the property

Cap: The eligible cost is capped at €48,000 per property unit (unità immobiliare). The maximum deduction is therefore €24,000 per unit (50% of €48,000), spread as €2,400/year over 10 years.

IVA (VAT) on installation: Residential solar installations in Italy are subject to 10% IVA (reduced from the standard 22%). This IVA is included in the taxable base for the deduction — meaning the 50% deduction applies to the VAT-inclusive invoice total.

Claim Process — Step by Step

- Hire a certified installer. The installer must hold appropriate certifications under D.Lgs. 28/2011 and be registered with CCIAA. Request their fiscal code (codice fiscale) and certification number.

- Pay by bank transfer. Payment must be made exclusively by bonifico bancario or postale with the causale: “Detrazione spese ristrutturazione edilizia / efficienza energetica ai sensi dell’articolo 16-bis del TUIR” or equivalent ENEA reference. Cash payments invalidate the deduction.

- Obtain and keep invoice documentation. The invoice must specify the nature of work, address of installation, installer details, and VAT breakdown.

- Upload to ENEA (for Ecobonus route). If claiming under the Ecobonus pathway (which applies for energy efficiency improvements), submit a comunicazione to ENEA within 90 days of completion via the official ENEA portal.

- File deduction in annual IRPEF return (730 or UNICO). Enter the annual deduction installment (1/10 of 50% of eligible costs) in Quadro E (730 form) or the equivalent UNICO section.

Transferability: Unlike the Superbonus at its peak, the standard 50% deduction is not transferable to third parties (no cessione del credito) as of 2026. It must be used by the taxpaying property owner against their own IRPEF liability. This means it is only useful to homeowners with sufficient annual IRPEF liability to absorb the deduction.

2026 Detrazione Status — Will It Continue?

As of March 2026, the Italian government has not announced any plans to reduce or eliminate the 50% Detrazione Fiscale for solar and energy efficiency. The measure has existed since 1998 and has been continuously renewed in annual budget laws (Legge di Bilancio). A reduction to 36% for years from 2027 onwards was discussed in the 2025 Legge di Bilancio but was not enacted for PV systems. Monitoring the 2026 budget law (expected October–December 2026) is advisable.

Key Takeaway — Italy 50% Deduction

The Italian 50% deduction is powerful but slow — it delivers the benefit across 10 years, not immediately. For a homeowner with a €24,000/year IRPEF liability, the annual €2,400 deduction is straightforward. But for lower-income households, the deduction may exceed annual tax liability in early years, creating unused credit. Unlike the Superbonus, unused deductions cannot be carried forward indefinitely — excess over 10 years is lost. Model this carefully before advising clients.

France: TVA 5.5% + MaPrimeRénov’ Crédit Impôt

France takes a different approach: rather than a zero-rate VAT, France applies a reduced TVA of 5.5% on residential solar installations. The headline income tax credit (crédit d’impôt pour la transition énergétique, CITE) was phased out in 2022 and replaced by the MaPrimeRénov’ grant program, which is a direct subsidy rather than a tax credit.

TVA 5.5% — Reduced Rate for Residential Solar

The 5.5% TVA rate applies to the supply and installation of solar panels and solar thermal systems on residential properties. Standard TVA in France is 20%. The reduced rate applies when:

- The property is a completed residential building (over 2 years old — logement achevé depuis plus de 2 ans)

- The installation is carried out by a professional installer (auto-installation is not eligible)

- The work is for renewable energy generation or energy efficiency purposes

For a residential installation costing €8,000 net of TVA, the TVA at 5.5% is €440, compared to €1,600 at the standard 20% rate — a saving of €1,160 at point of purchase.

New builds (constructions neuves) are subject to the standard TVA rate of 20%, not the reduced rate. This distinction matters significantly for developers building residential properties with integrated solar systems.

MaPrimeRénov’ — Grant Program (Not a Tax Credit)

MaPrimeRénov’ is France’s flagship residential energy renovation grant, administered by ANAH (Agence nationale de l’habitat). Despite being described colloquially as a “crédit impôt,” it is actually a direct cash grant paid to the property owner (or directly to the installer in some cases). It is not offset against tax liability.

For solar PV specifically: as of 2026, MaPrimeRénov’ does not cover standalone PV installation in the same way it covers insulation, heat pumps, or solar thermal water heating. PV panels for electricity generation were historically excluded from MaPrimeRénov’ as a standalone measure. Solar thermal (chauffe-eau solaire) and combined solar systems (CESI) do qualify for MaPrimeRénov’ grants.

For solar thermal systems (residential): grants of €1,000–€4,000 depending on household income category (très modeste, modeste, intermédiaire, supérieure). Work must be performed by a certified RGE (Reconnu Garant de l’Environnement) installer.

Energy efficiency renovation bundles: When solar is installed as part of a broader MaPrimeRénov’ Rénovation d’Ampleur project (substantial renovation involving at least two energy-saving measures that improve the DPE rating by two grades), the package as a whole may be eligible for higher MaPrimeRénov’ funding including subsidies of 25–70% of total renovation cost depending on household income.

Eco-PTZ (Prêt à Taux Zéro)

France’s Eco-PTZ is a zero-interest loan available for energy renovation projects, including solar thermal installation. Loan amounts up to €50,000 are available for comprehensive renovation projects (rénovation globale). The Eco-PTZ can be combined with MaPrimeRénov’ grants without triggering cumulation restrictions, provided the total public support does not exceed 100% of eligible costs.

Pro Tip — Solar PV vs. Solar Thermal in France

French policy in 2026 is more generous to solar thermal than to standalone photovoltaic. If you are advising a French client on a combined solar installation (hybrid thermal-PV), structuring the project to include a qualifying CESI solar thermal element can unlock MaPrimeRénov’ grants that would not be available for PV-only. Use your solar proposal software to model both configurations and show the client the total NPV difference — it often justifies the additional system complexity.

Spain: Deducción Autonómica — Regional Variations

Spain does not offer a federal (national) income tax credit for residential solar PV. Instead, solar tax relief operates through the autonomous community (comunidad autónoma) system, where individual regions have authority to create their own income tax deductions on the regional portion of the IRPF (impuesto sobre la renta de las personas físicas). The result is a patchwork of incentives that vary significantly by region.

Standard VAT (IVA): Spain applies the standard 21% IVA on solar panel supply and installation at the national level. There is no reduced VAT rate for residential solar at the federal level in Spain (unlike Germany, Netherlands, or France). Some autonomous communities have lobbied for a reduced rate but no national policy change has occurred as of Q1 2026.

Regional Deductions — Overview by Autonomous Community

| Autonomous Community | Deduction Rate | Cap | Eligible Expenses | Status (2026) |

|---|---|---|---|---|

| Andalucía | 15% | €1,000/year | PV installation costs | Active |

| Canarias | 15% | €1,500/year | PV and solar thermal | Active |

| Murcia | 20% | €1,200/year | PV installation | Active |

| Castilla-La Mancha | 20% | €500/year | Energy efficiency measures incl. PV | Active |

| La Rioja | 15% | €600/year | Renewable energy installation | Active |

| Extremadura | 30% | €800/year | Solar PV installation | Active |

| Comunitat Valenciana | 20% | €8,800 per installation | PV + storage | Active |

| Madrid (Comunidad) | 15% | €1,000/year | Renewable energy | Active |

| Cataluña | 15% | €1,500/year | PV installation | Active |

| Aragón | 15% | €500/year | Renewable energy | Active |

Regional programs are subject to annual renewal. Verify current status with the regional tax authority (Agencia Tributaria Autonómica) before advising clients. Conditions including property type, installer certification, and income limits vary by region.

How to Claim Spanish Regional Deductions

Regional solar deductions are claimed in Tramo Autonómico of the IRPF return (Declaración de la Renta), filed annually by June 30 for the previous fiscal year. The autonomous community portion of IRPF is approximately 50% of total income tax liability — the deduction reduces only this regional portion.

Documentation required typically includes:

- Installer invoice (factura) with full details

- Proof of payment (not cash — bank transfer or card)

- Municipal building permit where required

- Certificate of installation from a certified electrician (certificado de instalación eléctrica)

Self-consumption (autoconsumo) regulation: Since Spain’s landmark autoconsumo royal decree (RD 244/2019, still operative with modifications in 2026), residential solar self-consumption is legal and simplified. Surplus energy exported to the grid is compensated by utilities at a variable market rate (compensación simplificada). This is not a formal feed-in tariff but effectively reduces net electricity bills.

ICIO rebate — local property tax: Many Spanish municipalities offer a rebate on ICIO (Impuesto sobre Construcciones, Instalaciones y Obras) of up to 50% for solar installations. ICIO is normally paid when obtaining the building permit. Some municipalities also offer IBI (local property tax / Impuesto sobre Bienes Inmuebles) reductions of up to 50% for 3–5 years post-installation. These local incentives are independent from regional income tax deductions and can be stacked.

Netherlands: 0% BTW + SDE++ Premium

The Netherlands implemented 0% BTW (btw = belasting over de toegevoegde waarde, the Dutch VAT) on residential solar panels from 1 January 2023, one of the earliest EU adopters of the 0% rate permitted under the 2022 directive.

0% BTW: Scope and Conditions

The 0% BTW rate applies to:

- Supply and installation of solar panels on residential properties

- Private individuals (not applicable to businesses, which use standard 21% BTW input/output VAT recovery mechanism)

Important condition: The 0% BTW applies when the solar panels are installed by a registered BTW installer. Private self-installation does not qualify. The installer must clearly invoice at 0% BTW and maintain records for Dutch tax authority (Belastingdienst) audit purposes.

Business owners with residential solar systems can opt to register the PV system as a business asset, recover 21% BTW on input costs, and apply 21% BTW to deemed self-supplies. In practice, the 2023 Belastingdienst guidance simplified this: small producers generating under 10,000 kWh/year can use a simplified annual correction rather than quarterly BTW filings.

SDE++ (Stimulering Duurzame Energieproductie) — Commercial Scale

The SDE++ is the Netherlands’ primary support scheme for commercial-scale renewable energy, including solar PV. It is not a tax credit but a production premium that tops up the market electricity price to a predefined floor price.

- Rounds: SDE++ is issued in twice-yearly bidding rounds (spring and autumn)

- Eligible systems: typically 15 kWp and above for solar PV (smaller systems covered by net metering — saldering — until its scheduled phase-out)

- Support period: 15 years from commissioning

- Rate: set competitively by tender; solar PV has been consistently among the lowest-cost technologies, with clearing prices well below wind in recent rounds

Saldering (net metering) phase-out: Dutch residential net metering (saldering) — where exported solar electricity is offset 1:1 against consumption from the grid — is being phased out. The phase-out schedule reduces the offset from 100% (2022) progressively. Solar installers in the Netherlands should model expected economics under the post-saldering regime, which replaces 1:1 offset with a feed-in tariff at the market rate (typically 0.04–0.08 €/kWh versus 0.22–0.30 €/kWh for retail electricity).

This makes self-consumption rate a critical variable in Dutch residential solar economics. Systems with high self-consumption (battery storage, EV charging integration, heat pump load management) retain far better economics than pure feed-in configurations. Dutch solar design software tools should model dynamic self-consumption rates rather than static averages.

United Kingdom: 0% VAT on Energy Saving Materials

The UK — outside the EU since January 2021 — operates its own VAT regime and has maintained a strong position on solar tax relief through the zero-rate VAT on energy-saving materials (ESM).

0% VAT: Energy Saving Materials (ESM)

Solar panels are classified as energy-saving materials under UK VAT law (Group 2, Schedule 7A, VATA 1994). Since April 2022, the UK government applied a 0% VAT rate (reduced from 5%) to the installation of energy-saving materials in residential properties. This was initially a temporary measure but was confirmed as permanent in the Autumn 2023 UK Budget statement.

What is covered:

- Solar PV panels

- Solar thermal panels

- Battery storage systems installed at the same time as solar panels

- Insulation, heat pumps, wind turbines (other ESMs)

What is not covered at 0% VAT:

- Standalone battery storage installed without concurrent PV installation (subject to 20% standard VAT)

- Commercial properties (standard 20% VAT applies)

- Off-grid systems without grid connection (varies)

Condition: The 0% rate applies only when installation is carried out by a VAT-registered installer. Supply-only (panels supplied without professional installation) does not qualify for 0%.

For a UK residential 6 kWp system costing £8,500 installed, the saving at 0% vs. the previous 5% rate is £425 — modest but meaningful. The saving versus the standard 20% rate (which applied before 2022) is £1,417.

Smart Export Guarantee (SEG)

The UK’s Smart Export Guarantee requires all larger electricity suppliers (those with 150,000+ customers) to offer export tariffs for small-scale generators (under 5 MW). Unlike the old Feed-in Tariff (FiT), which closed to new applicants in 2019, the SEG rate is set competitively by each supplier rather than centrally mandated.

Current SEG rates (Q1 2026) range from approximately £0.04–£0.15/kWh depending on supplier and tariff. The most competitive rates (Octopus Energy, E.ON Next) are typically offered as variable market-linked rates that can exceed £0.15/kWh at peak demand times. UK installers and developers should model SEG income at conservative base rates for bankable projections.

Poland: PIT Termomodernizacja Relief

Poland’s solar incentive architecture is anchored in the termomodernizacja (thermal modernization) PIT relief — an income tax deduction that applies to a broad range of energy efficiency investments, including solar PV.

How Termomodernizacja PIT Relief Works

Under Article 26h of the Polish PIT Act, individuals who own single-family residential buildings can deduct qualifying energy modernization expenditures from their taxable income, subject to a lifetime cap of PLN 53,000 per taxpayer (approximately €12,000 at 2026 exchange rates).

Eligible expenditures include:

- Solar PV systems (modules, inverters, mounting)

- Solar thermal collectors

- Heat pumps and geothermal installations

- Insulation and window replacement

- Biomass boilers

Key features:

- The deduction is from taxable income (not from tax liability), so the tax saving depends on the marginal rate: at 12% (standard rate), PLN 53,000 deduction saves PLN 6,360 in tax; at 32% (higher rate), the saving is PLN 16,960

- Unused deductions can be carried forward up to 6 subsequent tax years (no “use it or lose it” risk within the carry-forward window)

- No requirement to use certified installers, but VAT invoices (faktury VAT) are required as documentation

- The deduction can be claimed by both the property owner and co-owners (split proportionally)

VAT on solar in Poland: Solar PV systems under 300 kW installed on residential buildings are subject to 8% VAT (reduced rate). Standard rate is 23% in Poland. The 8% reduced rate is maintained in current legislation; Poland has not yet adopted 0% VAT for solar despite the EU directive authorization.

Mój Prąd Program (My Electricity)

Poland’s government has run multiple rounds of the Mój Prąd (My Electricity) subsidy program, providing direct grants for residential solar installations. As of Q1 2026, Mój Prąd 6.0 is the current active iteration, offering:

- PLN 7,000 (approx. €1,600) for PV system installation (up to 10 kWp)

- Additional PLN 5,000–PLN 16,000 for battery storage (depending on capacity)

- Additional grants for EV chargers and energy management systems

Mój Prąd grants can be stacked with the termomodernizacja PIT relief, subject to the rule that the portion covered by the grant is excluded from the PIT deduction base. This is a standard de minimis interaction — the taxpayer deducts only the net cost after the grant.

How to Claim European Solar Tax Relief: Documentation Requirements

Claiming solar tax relief correctly requires preparation before installation begins, not after. Errors in documentation are the single most common cause of rejected or delayed claims across all European jurisdictions.

Universal Documentation Checklist

Regardless of country, you will typically need:

- Installer invoice (factura/Rechnung/facture/fattura): Must include installer’s tax registration number, property address, system specification (kWp, panel model, inverter model), and itemized costs

- Proof of payment by traceable means: Bank transfer, credit card, or direct debit. Cash payments invalidate claims in Germany, Italy, France, and Spain

- Building permit or notification: Where required by local authority (varies by system size and country)

- Installer certification: Proof that the installer holds required national certification (MCS in UK, RGE in France, D.Lgs. 28/2011 in Italy, FVSB or equivalent in Germany)

- Grid connection confirmation: Issued by the distribution system operator (DSO/Netzbetreiber/Enedis/Enel/etc.) upon commissioning

Country-Specific Submission Steps

Germany: No separate tax filing for the 0% MwSt — it is applied on the invoice. For the Vereinfachungsregelung income tax exemption, declare in Anlage EÜR (if filing) or simply do not report PV income on the Einkommensteuererklärung. For KfW loans, apply directly through your Hausbank before project start.

Italy: Submit ENEA comunicazione within 90 days of completion. Claim deduction installment annually in Quadro E of the 730 form. Retain all documentation for at least 5 years post-final claim.

France: TVA 5.5% is applied by RGE-certified installers. For MaPrimeRénov’ (thermal/bundled projects), apply through the ANAH online portal before work starts (pre-authorization required for most grant amounts above €7,000).

Spain: Claim regional deduction in Tramo Autonómico of the IRPF return. Apply for ICIO rebate at the local ayuntamiento when obtaining the building permit — the rebate is not automatic.

Netherlands: 0% BTW applied by installer. Verify the installer is BTW-registered (check Belastingdienst register). For SDE++, apply through RVO (Rijksdienst voor Ondernemend Nederland) in the relevant bidding round.

UK: 0% VAT applied automatically by MCS-certified installer. Register with your electricity supplier for Smart Export Guarantee to receive export payments — registration is typically handled by the installer.

Poland: Claim termomodernizacja deduction in PIT-36 or PIT-37 return, Załącznik PIT/O. Submit Mój Prąd application via the WFOŚiGW (regional environmental fund) portal, typically within 30 days of commissioning and connecting to the grid.

Pro Tip — Pre-Installation Financial Modeling

The single highest-leverage action for any solar installer or developer across European markets is to present a complete, incentive-integrated financial projection before the customer signs. This should cover gross system cost, VAT treatment, applicable income tax deductions or credits by year, grant amounts, and net NPV at multiple self-consumption scenarios. SurgePV’s generation and financial modeling tool is built to handle country-specific incentive inputs and produce presentation-ready output. Use it to close faster and eliminate post-quote price objections.

How Stacking Tax Relief and Grants Works

One of the most commercially significant — and most misunderstood — aspects of European solar finance is the interaction between different incentive layers. Can you combine 0% VAT with an income tax deduction? Can you take a government grant and still claim a deduction? The answer, in most markets, is yes — within defined cumulation rules.

Model Your Solar Financials Before You Quote

Build country-specific, incentive-integrated financial projections your customers can trust — in minutes, not hours.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

The Cumulation Rule: Why It Matters

Under EU State Aid rules and most national grant frameworks, the total amount of public support (grants, tax credits, VAT relief, subsidized loans) expressed as a percentage of eligible project cost must not exceed 100% of the cost. In practice, most residential systems are far below this threshold even when stacking multiple layers.

The second key rule is the grant-deduction interaction: if a grant is received that covers part of the installation cost, the deductible base for income tax purposes is typically reduced by the grant amount. This prevents double-dipping — a €3,000 grant and a 50% deduction on the same €3,000 would effectively mean the public sector paid for 150% of that portion of cost.

Stacking Scenarios by Country

Germany — Maximum Stack:

- 0% MwSt (immediate VAT saving on entire system cost)

- KfW low-interest loan (financing layer — not a grant, does not reduce deductible base)

- Einspeisevergütung feed-in tariff revenue (20-year guaranteed income, tax-exempt under Vereinfachungsregelung)

- Länder grant (e.g., Thuringia or Saxony grants for rural solar installations, subject to individual program rules)

In Germany, all four layers can typically be combined for a residential system under 30 kWp. The 0% VAT and EEG tariff do not interact — they operate on different axes. KfW financing does not constitute a grant. Länder grants must be declared in the EEG registration but do not affect the VAT treatment.

Italy — Maximum Stack:

- 10% IVA (reduced VAT already in effect — not 0%, but reduced)

- Detrazione Fiscale 50% on net installation cost

- CER energy community incentive (up to €110/MWh for 20 years on shared self-consumption)

- Scambio sul Posto net metering compensation from GSE

- Regional grant (e.g., Puglia POR grant of €500–€2,000)

The Puglia grant reduces the base for the 50% deduction. If the grant is €1,500 and installation cost is €9,000, the deductible base is €7,500. The 50% deduction then yields €3,750 over 10 years rather than €4,500. CER incentives are independent — they are operational revenue, not a capital subsidy. Net stack: significant but requires precise calculation.

UK — Maximum Stack:

- 0% VAT on installation

- Smart Export Guarantee (revenue — not a capital incentive)

- Boiler Upgrade Scheme (BUS) — if including heat pump (£7,500 grant for air source heat pumps; can be combined with solar)

- Local authority grants (varies — some councils offer additional support via ECO4 or similar)

- Possible Warm Home Discount interaction for lower-income households

Poland — Maximum Stack:

- 8% VAT (reduced, not zero — no interaction with deduction)

- Mój Prąd grant (deducted from termomodernizacja base)

- Termomodernizacja PIT deduction (on net cost after grant)

- Regional WFOŚiGW co-financing (varies by voivodeship)

Worked Example: Net Cost After Tax Credits — 8 kWp Residential System

To make the cross-country comparison concrete, here is a worked financial example for an identical 8 kWp residential rooftop PV system with 6 kWh battery storage across four countries, based on Q1 2026 cost and incentive parameters.

Base System Specification:

- 8 kWp monocrystalline PV (20 × 400W panels, TOPCon)

- 8 kW string/hybrid inverter

- 6 kWh LFP battery storage

- Standard residential rooftop installation (pitched, south-facing, 30°)

- No complex shading or structural issues

Gross Installation Cost by Country (Before Incentives)

| Country | Gross Cost (incl. local VAT) | VAT Included | Net Hardware + Labor |

|---|---|---|---|

| Germany | €12,376 | €0 (0% MwSt) | €12,376 |

| Italy | €13,200 | €1,200 (10% IVA) | €12,000 |

| France | €12,680 | €680 (5.5% TVA) | €12,000 |

| Spain | €14,520 | €2,520 (21% IVA) | €12,000 |

| Netherlands | €12,000 | €0 (0% BTW) | €12,000 |

| UK | £12,000 | £0 (0% VAT) | £12,000 |

| Poland | €12,960 | €960 (8% VAT) | €12,000 |

Gross hardware + labor base assumed identical at €12,000/£12,000 across all markets for comparability. Actual country costs differ due to labor markets and supply chain.

Net Cost After Primary Tax Incentive (Year 1)

| Country | Gross Cost | Primary Tax Incentive | Net Cost (Year 1) | Effective Savings |

|---|---|---|---|---|

| Germany | €12,376 | 0% VAT (€2,352 saving vs. 19%) + tax-exempt income | €12,376 | VAT: €2,352 saved + ongoing EEG income |

| Italy | €13,200 | 50% Detrazione (€6,600 over 10 yrs) | €13,200 nominal / €6,600 net over 10 yrs | €6,600 over 10 years |

| France | €12,680 | 5.5% TVA (€680 saving vs. 20%) | €12,680 | VAT: €1,760 saved vs. 20% |

| Spain | €14,520 | ~20% regional deduction on IRPF portion | €14,520 nominal / ~€12,916 net after deduction | ~€1,600 depending on region |

| Netherlands | €12,000 | 0% BTW (€2,520 saving vs. 21%) | €12,000 | VAT: €2,520 saved |

| UK | £12,000 | 0% VAT (£2,400 saving vs. 20%) | £12,000 | VAT: £2,400 saved |

| Poland | €12,960 | Mój Prąd €1,600 grant + PIT deduction ~€1,440 | ~€9,920 net | ~€3,040 total |

Net Cost After Full Incentive Stack (Including Grants + Tariffs, 10-Year View)

| Country | Total Incentive Value (10 yr, NPV) | Net Cost After All Incentives | Payback Estimate |

|---|---|---|---|

| Germany | €5,800–€8,200 (EEG revenue + VAT saving) | €4,200–€6,600 | 5–7 years |

| Italy | €6,600 deduction + €3,200 net metering | €3,400–€4,800 | 5–7 years |

| France | €1,760 VAT saving + €3,400 export/savings | €7,500–€8,700 | 8–10 years (north) / 6–7 years (south) |

| Spain | €1,600 deduction + self-consumption savings | €9,000–€11,000 | 8–11 years (north) / 6–8 years (south) |

| Netherlands | €2,520 VAT saving + net metering (phasing out) | €7,200–€9,000 | 8–10 years |

| UK | £2,400 VAT saving + SEG £800–£2,000 | £8,000–£9,800 | 9–12 years |

| Poland | €3,040 total grants/deductions + electricity savings | €7,200–€9,000 | 7–9 years |

Payback periods incorporate electricity price assumptions: Germany €0.28–€0.32/kWh, Italy €0.28–€0.35/kWh, France €0.23–€0.27/kWh, Spain €0.22–€0.30/kWh, Netherlands €0.28–€0.35/kWh, UK £0.24–£0.29/kWh, Poland €0.15–€0.20/kWh. Self-consumption assumed at 35–50% without battery, 60–75% with battery.

Key Takeaway — Incentive Stack Analysis

Germany and Italy offer the most generous combined incentive stacks for residential solar in 2026 among major European markets. Germany delivers immediate VAT elimination plus ongoing tax-exempt EEG revenue. Italy delivers 50% of capital cost back over 10 years plus net metering. The critical difference: Germany’s benefits are immediate and certain; Italy’s are spread over a decade and require annual IRPEF liability to absorb. For financial planning purposes, always calculate the NPV of multi-year deductions — a 50% deduction taken over 10 years at a 5% discount rate is worth approximately 43% of cost in present value terms, not 50%.

Using SurgePV’s generation and financial modeling tool allows you to run this full incentive stack analysis for any European project — entering the country-specific VAT rate, deduction percentage, grant amounts, feed-in tariff rates, and electricity price assumptions to produce a bankable, client-ready financial projection.

European Solar Market Outlook: Policy Trajectory to 2030

Tax and VAT policy is not static. Understanding the direction of travel is as important as the current rules for anyone making 10–25 year solar investment decisions.

EU Green Deal and REPowerEU: The Policy Backdrop

The European Green Deal targets climate neutrality by 2050, with a 55% reduction in net greenhouse gas emissions by 2030 (Fit for 55 package). Solar PV is one of the cornerstones of this transition: the European Commission’s REPowerEU plan (published 2022, updated 2023) targets 600 GW of solar PV capacity across the EU by 2030, up from approximately 260 GW installed at end-2024.

REPowerEU solar-specific measures:

- Solar Rooftop Initiative: mandatory solar on new commercial buildings by 2026 and new residential buildings by 2029 (implementation varies by member state)

- EU Solar Industry Alliance: supporting domestic manufacturing capacity

- Permitting acceleration: member states required to simplify and accelerate solar permitting under the revised Renewable Energy Directive (RED III)

- Net metering and self-consumption rules: RED III explicitly supports the right to self-consume and collectively self-consume renewable energy

Tax Incentive Trends to Watch

More 0% VAT adoptions likely. Romania, Bulgaria, and Greece have not yet adopted 0% VAT for solar. With EU pressure intensifying and installation rates lagging, it is likely at least one of these markets moves to 0% during 2026–2027. For installers considering market expansion, these are the markets to watch.

Italy’s deduction may reduce to 36% post-2026. The Italian government has signaled that the Detrazione Fiscale may be restructured, with a possible reduction from 50% to 36% for general energy efficiency measures from 2027. Solar-specific preservation at 50% is not guaranteed. Clients considering Italian installations should act while the 50% rate is confirmed.

Germany’s Vereinfachungsregelung is embedded. There is no political appetite to reverse Germany’s 0% VAT or the income tax simplification — both enjoy cross-party support and are administratively embedded. Long-term planning certainty for Germany is high.

Poland’s Mój Prąd will continue in some form. Each iteration of Mój Prąd has been oversubscribed and renewed. The exact grant amounts shift with each round, but Poland’s strong political commitment to energy independence (driven by geopolitical context) makes continuing subsidy support very likely through at least 2027.

Carbon Border Adjustment Mechanism (CBAM): While primarily affecting industrial sectors, CBAM signals a continuing EU trajectory of putting a price on carbon — making renewable energy economics progressively more attractive relative to fossil fuel alternatives. This is a long-term structural tailwind for solar across all European markets.

Installer and Developer Implications

The European solar incentive environment in 2026 rewards those who build financial sophistication into their client engagement process. A customer who understands that their effective net cost after Germany’s 0% VAT plus 20-year EEG revenue is €4,200–€6,600 for an 8 kWp system is a fundamentally different conversation from a customer presented with a €12,376 sticker price.

The installers and developers who are winning market share across European markets in 2026 are those who:

- Present incentive-integrated financial models at the first meeting — not as a follow-up

- Know the documentation requirements before the install, not after

- Help customers navigate grant applications as part of the service offering

- Use solar design software that generates accurate, site-specific production estimates that can be audited and defended

The financial analysis layer — correctly calculating system output, applying the right incentive framework, and producing a credible NPV projection — is where good solar proposal software creates a measurable competitive advantage. Learn more about European incentive programs in our comprehensive European solar incentives guide.

FAQ

Which European countries offer solar tax credits in 2026?

In 2026, the most significant solar tax incentives are active in Germany (0% VAT on residential PV under 30 kWp, plus income tax exemption for small systems), Italy (50% income tax deduction over 10 years via Detrazione Fiscale), France (TVA 5.5% reduced VAT for residential PV), Spain (regional deductions of 15–50% in multiple autonomous communities), the Netherlands (0% BTW since 2023), the UK (0% VAT on energy-saving materials), and Poland (termomodernizacja PIT relief and Mój Prąd grants). Austria and Czech Republic also adopted 0% VAT in 2024.

Is there VAT relief on solar panels in Europe?

Yes — VAT relief on solar panels is widespread across Europe in 2026. The EU amended its VAT Directive in April 2022 to allow member states to apply 0% VAT to residential solar panels. Germany implemented 0% MwSt from January 2023, the Netherlands followed with 0% BTW, Belgium adopted 0% from April 2023, and Austria and Czech Republic moved to 0% in 2024. France applies a reduced 5.5% TVA. The UK applies 0% VAT on solar under its energy-saving materials exemption. Spain remains at 21% IVA at the national level.

Can you stack solar tax credits with grants in Europe?

Stacking is possible in most European countries but subject to de minimis and cumulation rules. In Germany, 0% VAT can be combined with KfW financing and Länder grants. In Italy, the 50% Detrazione Fiscale can be stacked with CER energy community incentives and regional grants, but the grant amount is excluded from the deduction base. In France, MaPrimeRénov’ grants and TVA 5.5% can be combined. Always disclose all sources of public support during applications — undisclosed stacking can trigger clawbacks.

How do I claim solar tax relief in Germany in 2026?

German solar tax relief operates through two routes. For VAT (MwSt): any residential property owner installing a PV system up to 30 kWp simply pays 0% VAT — the rate is applied automatically by certified installers. For income tax: systems up to 30 kWp are fully exempt from income tax under the Vereinfachungsregelung — no separate application is required. For KfW low-interest loans, apply through your Hausbank before project commissioning.

What is the Italy Detrazione Fiscale 50% and how do I claim it?

The Italian Detrazione Fiscale 50% allows homeowners to deduct 50% of qualifying solar installation costs (capped at €48,000 per property unit) from their IRPEF income tax liability, spread equally over 10 consecutive years. The maximum annual deduction is €2,400 (10% × 50% × €48,000 cap). To claim: pay by bank transfer with the correct causale wording, obtain a certified installer invoice, submit an ENEA comunicazione within 90 days of installation completion, and claim the annual installment in Quadro E of your 730 IRPEF return each year.

Will European solar tax incentives continue after 2026?

The general policy direction across Europe is toward continued or expanded incentives for solar, driven by the EU Green Deal, REPowerEU 600 GW target, and energy security imperatives. Germany’s 0% VAT and income tax simplification appear stable with no sunset date. The UK confirmed its 0% VAT is permanent. Italy’s 50% deduction is at risk of reduction to 36% from 2027 — watch the 2026 Legge di Bilancio. Poland’s Mój Prąd program continues to be funded in successive rounds. The overall trajectory is positive for solar economics, but monitoring annual budget laws in each country is essential for precise investment planning.