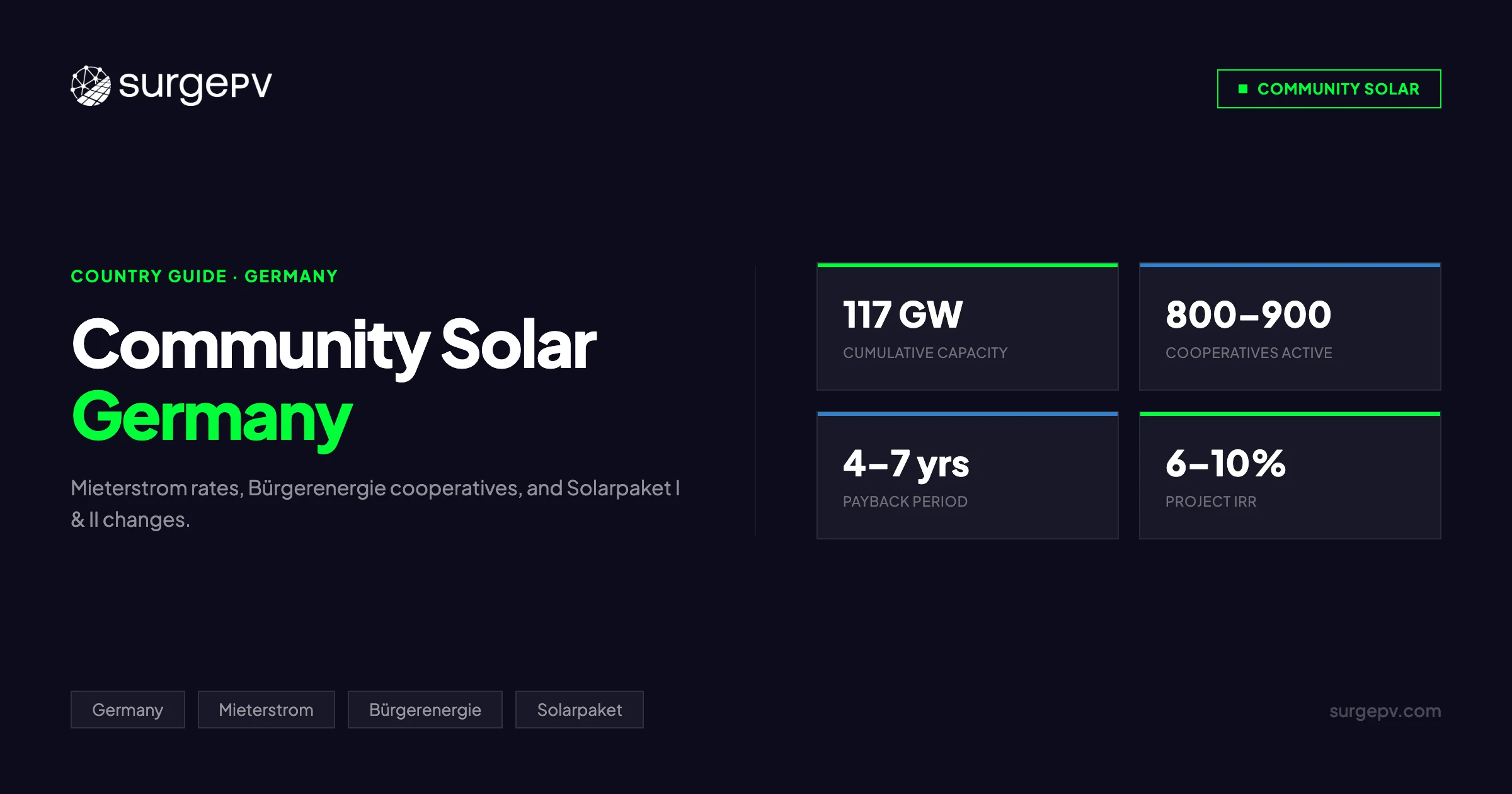

Germany’s solar market crossed 117 GW of cumulative installed capacity at the start of 2026. Wind and solar together delivered over 55% of public electricity generation in 2025 — the first time renewables held that majority. Those headline figures tend to dominate coverage. But the more consequential story is what sits beneath them: a dense and unusually democratic ownership architecture that no other major solar market has replicated at scale.

Germany’s Energiewende is not simply a story of aggregate gigawatts. It is a story of who owns the megawatts. Tenant-electricity programs (Mieterstrom) put rooftop solar economics within reach of renters in Cologne apartment blocks. Citizen energy cooperatives (Energiegenossenschaften) let a retired teacher in a Bavarian market town co-own a commercial PV plant for €250. The new Gemeinschaftliche Gebäudeversorgung model introduced by Solarpaket I lets a mixed-use building in Hamburg share a single rooftop system across flats, offices, and retail units without individual smart meters for each tenant. These are not peripheral programs. They are structurally important mechanisms for ensuring that the Energiewende delivers broad-based economic participation rather than concentrating returns in corporate balance sheets.

This guide covers every layer of that picture for 2026. Whether you are a landlord evaluating Mieterstrom economics, a citizen researching how to join or start an Energiegenossenschaft, a solar installer designing community-scale systems, or a cooperative board member assessing Solarpaket I implications — you will find current data, policy status, and actionable guidance here. All financial data reflects March 2026 conditions.

TL;DR — Germany Community Solar 2026

Germany has 800–900 active energy cooperatives, Mieterstrom supplements running €2.5–3.8 ct/kWh in 2026, and a new Gemeinschaftliche Gebäudeversorgung model from Solarpaket I that simplifies shared building supply. EEG 2023 removed the Mieterstrom expansion cap that had blocked hundreds of viable projects. Solarpaket II is in progress, targeting grid access reforms for cooperative projects. Community solar project payback typically runs 4–7 years with 6–10% IRR over a 20-year project life.

In this guide:

- Latest 2026 policy updates — Germany community solar status table (Solarpaket I/II, EEG, grid access)

- What community solar means in Germany: Energiegemeinschaft, Bürgerenergie, and Energiegenossenschaft defined

- EEG Mieterstrom 2026: how tenant electricity works, current supplement rates, and a worked financial model

- Bürgerenergie cooperative models: joining, starting, and evaluating financial health

- Solarpaket I and II: what changed and what is still in progress

- Gemeinschaftliche Gebäudeversorgung: the new shared metering model explained

- EEG feed-in vs. net metering for community projects

- Community solar project development: step-by-step process

- Financing models for German community solar

- How solar design software supports community project development

- FAQ

Latest Updates: Germany Community Solar 2026

The German solar policy environment saw significant legislative activity between mid-2024 and early 2026. Here is the current status of every program and development relevant to community solar.

Germany Community Solar Policy Status — March 2026

| Program / Development | Status | Key Detail |

|---|---|---|

| Solarpaket I | In force (May 2024) | Simplified Balkonkraftwerk registration; new Gemeinschaftliche Gebäudeversorgung model; expanded Mieterstrom scope |

| Solarpaket II | In legislative process (2025–2026) | Grid access reforms for community projects; prosumer rules; cooperative tender privileges under review |

| EEG Mieterstromzuschlag | Active | €2.5–3.8 ct/kWh depending on system size; no 100 kWp cap since EEG 2023 |

| Solarspitzengesetz (Solar Peak Act) | In force (Feb 2025) | Zero feed-in obligation at negative market prices; Mieterstrom projects largely unaffected as consumption is on-site |

| Gemeinschaftliche Gebäudeversorgung | Active (post-May 2024) | Shared building supply without per-unit metering; up to 500 kWp per building |

| EEG 2026 feed-in degression | In force | Rooftop tender benchmark set at €0.10/kWh for 2026; degression continues quarterly |

| Cooperative tender privileges | Under review | Bürgerenergie projects historically received tender bonuses under EEG §36g; applicability post-Solarpaket II being clarified |

| Grid access for community projects | Ongoing reform | Bundesnetzagentur rule updates expected in H2 2026 under Solarpaket II framework |

| Small-system EEG subsidy phase-out | Planned | Federal Ministry review ongoing; no enacted timeline as of March 2026 |

Pro Tip

If you are designing a new community solar system in Germany, the Gemeinschaftliche Gebäudeversorgung model introduced by Solarpaket I is often the simpler path for larger or mixed-use buildings. It does not require individual smart metering per tenant unit, which can cut metering infrastructure costs by €3,000–€8,000 on a 20-unit building. For buildings below 100 kWp with straightforward residential tenancy, classic EEG Mieterstrom with the Zuschlag supplement may still deliver better overall economics.

What Solarpaket II Means for Community Projects

Solarpaket I (May 2024) addressed the supply side of community solar: it simplified project registration, created the Gemeinschaftliche Gebäudeversorgung model, and removed Mieterstrom caps. Solarpaket II, currently working through the Bundestag legislative process, focuses primarily on the grid side — the rules that determine how community solar projects connect to and interact with the distribution network.

Key Solarpaket II proposals relevant to community solar include:

- Simplified grid access for cooperative projects below 500 kWp — reduced technical documentation requirements and faster connection timelines from Netzbetreiber

- Prosumer rights clarification — clearer rules on how community solar participants who both produce and consume can settle within EEG accounting

- Aggregator model support — allowing multiple small cooperative installations to be virtually aggregated for grid participation and market access

- Cooperative tender bonus review — the existing §36g EEG tender bonus for Bürgerenergie projects, which grants a price premium at competitive tenders for projects meeting citizen-ownership criteria, is being evaluated for expansion or modification

Until Solarpaket II is enacted (expected 2026), installers and cooperative developers should plan projects within the Solarpaket I framework, while monitoring the legislative timeline for grid-access provisions.

What Is Community Solar in Germany?

Community solar in Germany operates under several distinct legal and business frameworks. Understanding the terminology before evaluating any project is essential — these terms are frequently used interchangeably in public discussion but carry precise legal meanings that determine project structure, economics, and regulatory treatment.

Energiegemeinschaft vs. Bürgerenergie vs. Energiegenossenschaft

| Term | Meaning | Legal Form | Key Feature |

|---|---|---|---|

| Energiegemeinschaft | Energy community | Various (cooperative, GmbH, GbR, association) | Broad umbrella term for any collectively owned or managed energy project |

| Bürgerenergie | Citizen energy | Usually Genossenschaft or GmbH & Co. KG | Emphasizes citizen ownership and local economic benefit; basis for EEG §36g tender privileges |

| Energiegenossenschaft | Energy cooperative | eG (registered cooperative under GenG) | One member, one vote regardless of share size; democratic governance |

| Gemeinschaftliche Gebäudeversorgung | Shared building energy supply | New Solarpaket I model — no separate legal entity needed | Building-level shared supply without per-unit metering |

For EEG §36g tender eligibility — which gives Bürgerenergie projects a pricing advantage in competitive feed-in tenders — a project must meet specific ownership criteria: at least 51% of shares held by natural persons who are residents of the relevant municipality or an adjacent municipality, or by municipalities themselves. This is a precise legal test, not a casual description.

How German Community Solar Differs from Corporate Models

Traditional utility-scale solar in Germany concentrates ownership in corporations, institutional investors, and infrastructure funds. Community solar inverts this architecture in three important ways:

Ownership structure. Cooperative shares are held by individual citizens, typically in the range of €100–€10,000 per member. No institutional investor can accumulate voting control in a cooperative regardless of capital invested — one member, one vote is embedded in German cooperative law (Genossenschaftsgesetz, GenG).

Economic benefit distribution. Returns accrue to member-shareholders who are typically residents of the community in which the plant operates. Electricity may be sold preferentially to members at rates below the local grid tariff. This local economic recirculation is the defining Bürgerenergie value proposition and the rationale for policy preferences.

Transparency and accountability. German cooperatives must publish audited annual accounts (Prüfungsbericht), hold annual general meetings (Generalversammlung), and submit to mandatory auditing by a recognized cooperative auditing association (Prüfungsverband). This accountability structure creates the institutional trust that allows rural citizens to invest meaningful sums in local energy projects managed by neighbors rather than professionals.

Germany developed this model during the Energiewende’s early growth years, when EEG feed-in tariffs made small-scale renewable projects profitable enough to attract citizen investors at accessible share prices. Over 1,700 community energy projects of all types — solar, wind, biogas, and small hydro — currently operate across Germany. The sector manages combined assets exceeding €2 billion.

Leading Regions for Community Solar in Germany

| Region | Estimated Active Cooperatives | Notable Characteristics |

|---|---|---|

| Bavaria | 180–220 | Highest density per capita; strong rural tradition; 1,200–1,400 kWh/m²/year irradiance |

| Baden-Württemberg | 120–150 | Heidelberger Energiegenossenschaft; EWS Schönau as founding model |

| North Rhine-Westphalia | 100–130 | Urban Mieterstrom focus; dense apartment housing stock |

| Schleswig-Holstein | 80–100 | Wind-solar hybrid cooperatives; high wind share |

| Saxony | 40–60 | Emerging post-coal transition communities; growing new cooperative formations |

| Hessen | 50–70 | University towns with educated citizen investor base; Frankfurt-area urban projects |

Bavaria’s dominance reflects a combination of structural factors: high solar irradiance, a century-long tradition of Raiffeisen agricultural cooperatives providing institutional knowledge and legal templates, and a rural settlement pattern where energy cooperatives can serve a geographically coherent community with genuine shared interests.

EEG Mieterstrom: Tenant Solar in Germany

The EEG Mieterstrom program is Germany’s primary mechanism for extending solar economics to apartment renters. Over 50% of Germans rent rather than own their homes — in major cities like Berlin, Hamburg, and Cologne, the rental share exceeds 75%. Without a dedicated tenant electricity framework, grid-tied rooftop solar would benefit only property owners, excluding the majority of urban Germans from the Energiewende’s direct economic gains.

How Mieterstrom Works

Under the Mieterstromgesetz (Tenant Electricity Law, initially introduced in 2017, substantially reformed by EEG 2023 and Solarpaket I 2024), the mechanics operate as follows:

- A landlord installs a rooftop PV system on a residential building containing at least one rented flat

- The system generates solar electricity and supplies it directly to tenants in the same building at a discounted rate — legally capped at 90% of the applicable local standard grid tariff (Grundversorgungstarif)

- Surplus power not consumed by tenants exports to the grid at the standard EEG feed-in tariff

- The landlord receives an additional Mieterstromzuschlag (tenant electricity supplement) on every kWh delivered directly to tenants — paid on top of the standard feed-in tariff

The Mieterstromzuschlag is the financial mechanism that makes the landlord’s investment economically superior to simply exporting all generation to the grid. Without it, the landlord would receive €0.082/kWh for grid exports. With the Zuschlag, tenant-consumed kWh generate the feed-in tariff rate plus the supplement plus the discounted tenant electricity tariff — creating a materially better revenue stream on every kWh consumed on-site.

EEG Mieterstromzuschlag Rates — 2026

The supplement is degressive by system size and is updated quarterly. Approximate rates for 2026:

| System Size | Mieterstromzuschlag (approx. ct/kWh) |

|---|---|

| Up to 10 kWp | ~3.8 ct/kWh |

| 10–40 kWp | ~3.1 ct/kWh |

| 40–100 kWp | ~2.5 ct/kWh |

| Over 100 kWp | Not eligible — use Gemeinschaftliche Gebäudeversorgung model |

Rates are published quarterly by the Bundesnetzagentur and are degressive. Verify current rates at Bundesnetzagentur.de before project financial close.

Key Change: EEG 2023 Removed the Expansion Cap

Before EEG 2023, total Mieterstrom capacity eligible for the Zuschlag was capped at 500 MW nationally. Projects competed for a limited annual quota, and many viable projects on qualifying buildings were simply never built because the cap had been reached. EEG 2023 removed this national cap entirely, making the Mieterstromzuschlag available to any qualifying building at any time. This single policy change did more to open the Mieterstrom market than any other reform since the program’s inception in 2017.

Eligibility Conditions for Mieterstrom

Not every building qualifies. The key eligibility conditions under current EEG Mieterstrom rules:

- The building must be primarily residential (Wohngebäude) — commercial-first buildings should use the Gemeinschaftliche Gebäudeversorgung model

- The PV system must be located on the same building or in the immediate vicinity (räumlicher Zusammenhang) of the supplied flats

- The system capacity eligible for the Zuschlag is capped at 100 kWp per building (larger systems can export the excess under standard EEG, but only the first 100 kWp generates Zuschlag)

- The landlord must enter into a separate Mieterstromvertrag (tenant electricity contract) with each participating tenant — this contract cannot be bundled into the rental agreement and must give tenants a genuine right to opt out and purchase grid electricity instead

- Tenant tariff is legally capped at 90% of the applicable Grundversorger tariff in the supply area — this protects tenants from above-market pricing while still providing the landlord with better-than-export-tariff revenue

The opt-out provision is significant. Installers designing Mieterstrom systems must account for variable self-consumption rates based on actual tenant participation — typically 70–90% of tenants opt in, but financial models should stress-test at 50–60% participation to ensure project viability under realistic downside scenarios.

Mieterstrom Financial Model: Worked Example

Building: 20-unit apartment block in Stuttgart. Available roof area: 300 m². System: 50 kWp.

| Parameter | Value |

|---|---|

| Annual generation | ~50,000 kWh |

| Tenant direct consumption share (85% opt-in, 65% of generation consumed) | 32,500 kWh |

| Grid export share | 17,500 kWh |

| EEG feed-in tariff revenue (export) | 17,500 × €0.082 = €1,435/year |

| EEG feed-in tariff on tenant-consumed kWh | 32,500 × €0.082 = €2,665/year |

| Mieterstromzuschlag (40–100 kWp bracket, 2.5 ct/kWh) | 32,500 × €0.025 = €813/year |

| Tenant electricity tariff revenue (at €0.28/kWh, 20% below local rate) | 32,500 × €0.28 = €9,100/year |

| Total annual revenue | ~€14,013/year |

| System capex (installed, 50 kWp, including metering) | ~€57,000 |

| O&M and insurance (annual) | ~€900/year |

| Net annual income | ~€13,113/year |

| Simple payback | ~4.3 years |

This model assumes a tenant tariff approximately 20% below the local Grundversorger rate (€0.28/kWh vs. €0.35/kWh). No grid purchase costs or Netzentgelte apply to the self-consumed portion, which significantly improves the economics compared to a standard grid-tied export system. At a 4% discount rate, 20-year project IRR exceeds 8%.

Pro Tip

Run this financial model with your actual local Grundversorger tariff, not a national average. In Munich and Frankfurt, residential electricity rates in 2026 are closer to €0.38–€0.42/kWh — materially above the national average — which compresses the tenant tariff discount required to stay within the legal 90% cap and increases landlord revenue per kWh. Use SurgePV’s generation and financial tool to plug in location-specific tariff data and generate a full 20-year Mieterstrom model within minutes.

Common Mieterstrom Implementation Mistakes

Experienced Mieterstrom installers avoid several mistakes that routinely undermine project economics and create legal exposure:

1. Overestimating tenant self-consumption without accounting for household absence patterns. Tenants are not home during business hours. A residential building with working-age tenants will have its peak solar generation (10:00–14:00) occur during minimum occupancy. Direct self-consumption ratios of 65% are achievable in buildings with elderly residents, home-office workers, or shift workers — but can fall to 40–50% in standard commuter apartment blocks. Battery storage can recover 10–20 percentage points of this loss.

2. Failing to account for metering infrastructure cost. Each participating tenant unit requires a smart meter capable of recording both consumption and Mieterstrom supply in 15-minute intervals for EEG settlement purposes. At €300–€600 per unit including installation, metering can add €6,000–€12,000 to a 20-unit building project — a cost that comparisons with the Gemeinschaftliche Gebäudeversorgung model must include.

3. Bundling the Mieterstromvertrag into the rental agreement. This is legally prohibited under current EEG rules. The tenant electricity contract must be separate, with genuine opt-out rights. Bundling creates regulatory non-compliance that can trigger clawback of the Mieterstromzuschlag.

4. Using shadow analysis only for sizing, not for EEG settlement modeling. EEG Mieterstrom settlement requires precise monthly yield attribution. A solar shadow analysis software tool that models seasonal shading variation produces the monthly generation profiles needed for accurate EEG reporting — not just the annual total used for sizing.

Bürgerenergie Models: Solar Cooperatives in Germany

Germany’s energy cooperative sector is the largest in Europe by asset value and member count. The DGRV (Deutschen Genossenschafts- und Raiffeisenverband) reports approximately 800–900 active energy cooperatives, down from a peak of over 1,000 due to consolidation of smaller cooperatives formed during the 2011–2014 EEG boom. But total assets and membership are at record levels — exceeding €2 billion in combined cooperative assets.

The Cooperative Model and Its Advantages

The Genossenschaft (cooperative) legal form under German GenG provides several structural advantages that make it the natural vehicle for citizen energy projects:

Democratic governance. One member, one vote regardless of share size. A founding member with €100 invested has identical voting rights to a larger investor holding €10,000. This prevents takeover by institutional capital and preserves the community character of the project.

Limited liability. Members’ liability is limited to their share capital (unless the Satzung specifies otherwise). This makes participation accessible to citizens without significant wealth who want to invest but cannot risk personal assets.

Mandatory transparency. Cooperatives must be audited by a recognized Prüfungsverband, publish their annual accounts, and hold annual general meetings open to all members. This institutional accountability differentiates cooperatives from informal investment groups and builds the member trust required for multi-decade energy projects.

EEG tender privileges. Projects meeting the §36g Bürgerenergie criteria receive a special tariff in competitive EEG auctions — historically €0.01–€0.02/kWh above the clearing price. While this provision is under review in the Solarpaket II process, it has historically given cooperative projects a competitive advantage against larger commercial bidders in community-scale tender rounds.

Joining an Existing Cooperative

The simplest path for a citizen wanting to participate in community solar:

- Find a local cooperative — search the Bürgerwerke network, your regional Energieagentur, or the DGRV cooperative register. Bürgerwerke eG aggregates 113 local cooperatives and provides a searchable map.

- Review the Geschäftsbericht (annual report) — cooperatives must publish audited accounts; examine the trailing 3-year dividend record, existing project portfolio (especially EEG contract vintage), and new project pipeline

- Purchase Geschäftsanteile (shares) — minimum investment typically €100–€500 per share; many cooperatives allow incremental additions

- Attend the Generalversammlung (annual general meeting) — one vote per member regardless of shares held; strategic decisions including new projects, tariff changes, and board elections require AGM approval

- Receive distributions — typically 3–5% annual dividend on share capital, sometimes paired with a discounted electricity tariff for participating members

Pro Tip — Evaluating a Cooperative’s Financial Health

Before purchasing shares, examine three indicators: (1) Debt-to-equity ratio — well-managed cooperatives keep this below 60%; high leverage amplifies the risk of EEG tariff degression; (2) Feed-in tariff vintage — projects commissioned on 20-year EEG contracts from 2010–2015 are locked into rates of €0.18–€0.28/kWh through 2030–2035, providing earnings certainty that newer projects at €0.08–€0.10/kWh cannot match; (3) Post-EEG project pipeline — cooperatives with a credible plan for Mieterstrom or Gemeinschaftliche Gebäudeversorgung projects have revenue growth potential after their legacy tariff contracts expire.

Starting a New Energy Cooperative

Forming a new Energiegenossenschaft requires a minimum of three founding members and registration under the Genossenschaftsgesetz. The process in practical terms:

Step 1: Draft the Satzung. The articles of association define membership rules, share structure, governance, profit distribution policy, and dissolution procedures. DGRV provides standardized Satzung templates for energy cooperatives that satisfy regulatory requirements and have established interpretive precedent.

Step 2: Establish founding capital. The legal minimum is €1 per member share, but practical minimum capital for a viable first project is €10,000–€50,000 — enough to cover legal costs, professional development fees, and a credible equity stake in an initial solar project.

Step 3: Register with the Genossenschaftsregister. Registration is filed at the Amtsgericht (local court) in the cooperative’s home district. The cooperative receives legal entity status upon registration.

Step 4: Join a Prüfungsverband. Membership in an auditing association is mandatory under §53 GenG. The Prüfungsverband conducts annual or biennial audits depending on cooperative size. Annual membership cost: €500–€2,000 for small energy cooperatives.

Step 5: Open a business bank account and begin project development. Cooperative banks (Volksbank, Raiffeisenbank) typically provide favorable terms for energy cooperatives aligned with their sector philosophy.

Total setup cost: €3,000–€8,000 in legal and registration fees. Timeline from initial planning to registered cooperative: 3–6 months. Timeline to first commissioned project: typically 12–24 months, including planning permission, EEG registration, and construction.

Notable German Energy Cooperatives

| Cooperative | Base | Members | Scale |

|---|---|---|---|

| Bürgerwerke eG | Pan-Germany (aggregator) | 50,000+ | 113 member cooperatives, 1,400+ power plants |

| BürgerEnergie Berlin eG | Berlin | 1,000+ | 40+ urban rooftop installations, €2M+ citizen investment |

| Energiegenossenschaft Starkenburg eG | Hessen | 700+ | 3.5 MW installed capacity |

| Heidelberger Energiegenossenschaft eG | Baden-Württemberg | 600+ | Multi-project Mieterstrom portfolio |

| EWS Schönau eG | Schönau, BW | 5,000+ | The original “rebel cooperative” — now a full grid-licensed regional utility |

| Greenpeace Energy eG | Hamburg | 130,000+ | Largest renewable energy cooperative by member count; operates as national electricity retailer |

The EWS Schönau case is worth understanding for its historical significance. In 1997, citizens of the Black Forest municipality of Schönau purchased the local electricity grid from Badenwerk following a grassroots campaign — creating what became Germany’s first fully citizen-owned local grid utility. EWS Schönau is now a national supplier with 130,000+ customers, demonstrating that citizen energy cooperatives can scale from village-level projects to national market participation.

Solarpaket I and II: What Changed and What Is Pending

Solarpaket I, enacted in May 2024, was the most significant German solar policy reform since EEG 2023. Solarpaket II is currently in the legislative process. Understanding both is essential for community solar project planning in 2026.

Solarpaket I: Five Changes That Matter for Community Solar

1. Gemeinschaftliche Gebäudeversorgung — a new shared building model. Solarpaket I created an entirely new legal framework for shared solar supply within a building. Unlike Mieterstrom, which requires individual smart meters per tenant unit and is restricted to primarily residential buildings, Gemeinschaftliche Gebäudeversorgung allows dynamic energy allocation across all building users using a simplified metering approach. The model works for residential, commercial, and mixed-use buildings up to 500 kWp. (Detailed explanation in the next section.)

2. Balkonkraftwerk registration simplified. Before Solarpaket I, plug-in balcony solar systems required notification to both the Marktstammdatenregister and the local Netzbetreiber. Grid operators routinely used the Netzbetreiber notification as a delay mechanism. Solarpaket I eliminated the Netzbetreiber requirement — only Bundesnetzagentur notification is now needed. Panel capacity limit was also raised from 600W to 2,000W (inverter output remains capped at 800W).

3. Mieterstrom scope expansion. Beyond the EEG 2023 removal of the national expansion cap, Solarpaket I extended Mieterstrom eligibility to systems on buildings immediately adjacent to the supply building (not just the exact rooftop being supplied). This allows ground-mounted carport systems or adjacent outbuildings to supply Mieterstrom to a main residential block — opening new design options for buildings with limited roof area.

4. Reduced bureaucracy for cooperative projects under 500 kWp. Solarpaket I streamlined grid connection application procedures for Bürgerenergie projects below 500 kWp, reducing the documentation burden on small cooperatives that lack dedicated legal and engineering teams.

5. EEG registration threshold raised. Systems below 100 kWp on residential and commercial buildings are exempt from certain EEG notification requirements, further reducing administrative friction for the community solar project sizes where Energiegenossenschaften typically operate.

Solarpaket II: Key Provisions Under Legislative Review

Solarpaket II addresses infrastructure and market access issues that Solarpaket I did not resolve. As of March 2026, the following provisions are under active legislative development:

Grid access reform for distributed generation. Community solar installers consistently report that slow Netzbetreiber grid connection timelines — averaging 6–14 months for projects above 100 kWp — are the primary bottleneck in project development. Solarpaket II proposes statutory connection timelines with financial penalties for Netzbetreiber who miss them, a reform the cooperative sector has advocated for since 2020.

Virtual net metering expansion. Currently, community solar projects can only net-meter consumption at the building level or at the individual metering point level. Solarpaket II proposes virtual net metering that would allow a cooperative’s generation from one site to be offset against member consumption at other grid-connected locations — effectively allowing smaller cooperatives to operate as virtual utility suppliers for their members without requiring physical colocation.

Aggregator market access. Community cooperatives are too small to participate directly in German electricity market mechanisms (Day-Ahead, Intraday, Balancing). Solarpaket II proposes regulatory changes to make aggregation of multiple community solar projects into a single market participant technically and legally straightforward — a provision that would significantly improve post-EEG revenue opportunities for cooperatives whose legacy contracts expire.

Key Takeaway — Planning Under Solarpaket II Uncertainty

Projects designed and permitted under Solarpaket I rules will not be invalidated by Solarpaket II changes — EEG grandfathering provisions have been consistent across reform cycles. Design community solar projects under current Solarpaket I rules now; treat Solarpaket II provisions as upside scenarios for projects whose commissioning timeline extends into late 2026 or 2027.

Gemeinschaftliche Gebäudeversorgung: Shared Metering Explained

The Gemeinschaftliche Gebäudeversorgung (GGV) model introduced by Solarpaket I is one of the most practically significant changes for urban community solar in years. It deserves detailed examination because it fundamentally changes the cost structure of solar-to-tenant supply.

The Core Problem GGV Solves

Classic EEG Mieterstrom requires individual smart meters for every participating tenant unit. On a 20-unit building, that means 20 smart meters plus the generating system meter — total smart meter capex of €6,000–€12,000, plus ongoing monthly data management costs. For older Gründerzeit-era apartments where electrical risers don’t neatly separate per-flat metering, installation cost can be higher still.

For many multi-family buildings — particularly those with small flat sizes, complex electrical configurations, or mixed residential-commercial layouts — the metering infrastructure cost under classic Mieterstrom makes the economics marginal or negative.

Gemeinschaftliche Gebäudeversorgung resolves this with a dynamic allocation model. Instead of measuring individual unit consumption in real time and attributing specific kWh of solar generation to each flat, GGV uses pre-agreed allocation keys (Verteilschlüsseln) to distribute the building’s total solar generation across participants. These allocation keys can be based on:

- Floor area (most common for residential) — a 70 m² flat receives a proportionally larger share than a 40 m² flat

- Number of residents — allocation proportional to declared household size

- Fixed fraction — equal shares regardless of unit size

- Historical consumption — allocation based on trailing 12-month consumption data

The grid operator settles each participant’s account monthly based on their allocated share of solar generation, without needing to measure real-time per-unit solar consumption.

GGV vs. Classic EEG Mieterstrom: Comparison

| Feature | EEG Mieterstrom | Gemeinschaftliche Gebäudeversorgung |

|---|---|---|

| Individual smart meters required | Yes — one per tenant unit | No — building-level meter plus allocation key |

| Eligible building type | Residential only | Residential and mixed-use |

| Maximum system size | 100 kWp for Zuschlag; larger systems use standard EEG | Up to 500 kWp per building |

| Mieterstromzuschlag supplement | Yes (€2.5–3.8 ct/kWh on tenant-consumed share) | No supplement — offset by lower metering infrastructure |

| Tenant tariff cap | 90% of local Grundversorger rate | Market-rate billing — no statutory cap (tenants billed for allocated share at agreed rate) |

| Implementation complexity | Medium-high (individual metering, separate contracts per tenant) | Lower (building-level settlement, allocation-key based) |

| Regulatory maturity | Established since 2017; extensive case law | Post-May 2024; limited operational precedent and limited case law |

| Grid operator settlement | Per-metering-point monthly | Monthly allocation statement to grid operator |

When to Choose GGV Over Classic Mieterstrom

GGV is the better framework when:

- The building has more than 15–20 tenant units, making metering infrastructure cost prohibitive under Mieterstrom

- The building is mixed-use (residential + retail + office) — classic Mieterstrom applies only to residential supply

- The system is above 100 kWp — classic Mieterstrom’s Zuschlag does not apply above 100 kWp; GGV scales to 500 kWp

- The building’s electrical infrastructure makes per-unit smart meter installation impractical or very expensive

- The project developer wants a faster path to market without the per-unit contracting overhead of Mieterstrom

Classic Mieterstrom remains the better framework when:

- The building is small (under 10 units) where metering costs are manageable

- The project size is under 40 kWp, where the highest Mieterstromzuschlag rates (3.1–3.8 ct/kWh) provide significant additional revenue

- The landlord wants maximum financial optimization per kWh and is willing to invest in the more complex structure

Key Takeaway — GGV Is Still New

The Gemeinschaftliche Gebäudeversorgung model has been legally available since May 2024 but has limited operational track record. Grid operators are still implementing the settlement systems required for dynamic allocation billing. Early adopters report varying timelines for grid operator GGV contract execution — from 3 months to 9 months. Factor this uncertainty into project timeline planning, and ensure your grid operator has confirmed GGV settlement capability before project financial close.

EEG Feed-In vs. Net Metering for Community Projects

Community solar projects in Germany interact with the EEG financial framework through three distinct mechanisms, and understanding the differences between them is prerequisite to accurate financial modeling.

Mechanism 1: EEG Einspeisevergütung (Feed-in Tariff)

The standard EEG Einspeisevergütung (feed-in tariff) is available to all eligible rooftop systems as a guaranteed fixed rate on every kWh exported to the grid, paid by the assigned grid operator and settled quarterly. For community solar projects:

- Applicable to: All EEG-registered systems that export surplus generation to the grid

- Rate (2026): Approximately €0.082–€0.090/kWh for rooftop systems under 10 kWp; lower for larger systems; rates are set quarterly and decrease quarterly (degression)

- Duration: 20 years from commissioning

- Relevance for community solar: All Mieterstrom and GGV systems export surplus generation at this rate; it forms the baseline revenue floor for all community solar financial models

Mechanism 2: Mieterstromzuschlag (Tenant Electricity Supplement)

As described in detail above, the Mieterstromzuschlag is an additional payment on top of the feed-in tariff specifically for kWh consumed directly by tenants in the same building. This supplements the standard feed-in tariff — it does not replace it. The landlord receives both: the standard EEG rate on tenant-consumed kWh, plus the Zuschlag on top.

- Rate range (2026): €0.025–0.038/kWh depending on system size

- Eligibility: Classic EEG Mieterstrom model only; not available under GGV

- Key restriction: Only applies to residential buildings; system must be on the same building (or immediately adjacent under Solarpaket I)

Mechanism 3: Kaufmännisch-bilanzielle Weitergabe (Commercial Balance Transfer)

For cooperative projects that supply electricity to members at different grid locations — not the same building — a commercial balance transfer mechanism allows the cooperative’s feed-in to be set against member consumption in the grid settlement system. This is effectively a virtual net metering mechanism available to licensed electricity suppliers.

- Applicable to: Cooperatives with electricity supply licenses (Stromlieferlizenz) supplying members across multiple grid connection points

- Settlement: Monthly via the market premium model or direct supply contract

- Practical relevance: Currently limited to larger, established cooperatives (Bürgerwerke, Greenpeace Energy); Solarpaket II proposes simplified access for smaller cooperatives

The Solarspitzengesetz Complication

The Solarspitzengesetz (Solar Peak Act, February 2025) introduced a zero-feed-in obligation at negative market prices. When the market price goes negative, EEG-registered systems must either curtail or receive zero compensation for exports during the negative-price period.

For community solar, the practical impact is limited but important:

- Mieterstrom systems are largely insulated: negative market prices tend to occur at midday in summer, when tenant consumption is low — but the on-site consumption of the Mieterstrom portion is not affected by the zero-feed-in rule (that rule applies only to grid exports)

- Cooperative ground-mount projects with high export ratios face more exposure — a summer midday negative price event can eliminate several hours of feed-in revenue per occurrence

- Battery-integrated projects can shift generation to avoid negative-price export by charging batteries during the negative-price period and discharging into the evening demand peak

Accurate modeling of negative-price exposure requires hourly generation simulation matched against historical market price data — a capability available in professional solar design software platforms that integrate market price data alongside generation modeling.

Community Solar Project Development: Step-by-Step

Developing a German community solar project from initial concept to commissioned operation involves eight distinct stages. The timeline from concept to commissioning typically runs 12–30 months depending on project size, planning complexity, and grid operator responsiveness.

Stage 1: Site Assessment and Opportunity Identification

The first step is identifying whether a building or land parcel presents a viable community solar opportunity. Key assessment criteria:

- Roof area and orientation: South-facing rooftops with tilt angles of 25–40° are optimal; east-west split systems are increasingly common for higher self-consumption profiles

- Shading assessment: Use solar shadow analysis software to model near-shading from adjacent buildings, chimneys, dormer windows, and vegetation — urban shading can reduce yield by 15–30% versus unshaded equivalent

- Building structure: Structural engineering assessment of roof load capacity; older German buildings (pre-1950) often require reinforcement for modern panel weights

- Tenant/member interest: Initial canvassing of tenant or community interest; Mieterstrom participation rates are critical inputs to financial viability

- Grid connection feasibility: Preliminary inquiry to Netzbetreiber on available grid capacity and estimated connection cost and timeline

This stage typically takes 4–8 weeks and should produce a preliminary yield estimate, rough financial model, and go/no-go recommendation before significant capital is committed.

Stage 2: Regulatory Framework Selection

Based on the Stage 1 assessment, select the appropriate regulatory model:

- Classic EEG Mieterstrom (residential, under 100 kWp, high Zuschlag value)

- Gemeinschaftliche Gebäudeversorgung (larger, mixed-use, or complex buildings)

- Cooperative EEG feed-in (ground-mount or large rooftop for cooperative member benefit)

- Direct supply with electricity license (for established cooperatives with market access)

This selection drives the legal structure, contracting approach, metering specification, and financial model — all downstream decisions depend on it.

Stage 3: Detailed Technical Design

With the regulatory framework confirmed, produce detailed technical design using solar design software capable of modeling the specific community solar configuration:

- Panel layout optimization accounting for shading, orientation, and structural constraints

- String configuration for multi-roof, multi-orientation systems

- Inverter selection and configuration

- Metering architecture (Mieterstrom per-unit, GGV building-level, or cooperative export metering)

- Generation simulation with monthly and hourly profiles for EEG settlement and financial modeling

- Battery storage integration assessment if self-consumption optimization is a project objective

The output of this stage is a detailed technical specification suitable for equipment procurement and a yield model with monthly granularity that feeds directly into the Stage 4 financial model.

Stage 4: Financial Modeling and Stakeholder Presentation

For cooperative projects, the financial model must satisfy the scrutiny of an AGM vote. For Mieterstrom projects, it must convince building owners and property managers. For both, investor-grade rigor is the standard.

A complete community solar financial model includes:

- 20-year annual revenue projections broken down by EEG feed-in, Mieterstromzuschlag, and tenant tariff streams (for Mieterstrom) or EEG feed-in and cooperative member tariff (for cooperative models)

- Capital cost breakdown by component

- O&M cost assumptions with inflation escalation

- Sensitivity analysis: electricity price (bear/base/bull), self-consumption rate, system performance ratio

- IRR, NPV, and payback period at each sensitivity scenario

- Post-EEG revenue scenario (for projects whose 20-year EEG contract will expire before the end of the economic model period)

SurgePV’s generation and financial tool produces these outputs automatically from the technical design — integrating actual yield simulation with EEG rate structures, German electricity price data, and customizable cost assumptions. For installers targeting the cooperative market, this capability is a material competitive differentiator: cooperative boards have encountered too many optimistic yield estimates from installers who built financial models in spreadsheets without rigorous yield simulation backing.

Stage 5: Permitting and EEG Registration

German community solar projects require two parallel permitting tracks:

Building permit (Baugenehmigung or Freistellungsverfahren): Requirements vary by Bundesland. Most rooftop installations under 100 kWp on existing buildings fall within Verfahrensfreiheit (permit-free) provisions in most Bundesländer — confirm the applicable Landesbauordnung for the project location. Ground-mount installations and systems on listed buildings (denkmalgeschützte Gebäude) require full Baugenehmigung.

EEG registration: All EEG-eligible systems must register in the Marktstammdatenregister (MaStR) before commissioning. Mieterstrom projects additionally require notification to the assigned Netzbetreiber with the Mieterstrom designation. GGV projects require a GGV contract with the Netzbetreiber establishing the allocation key methodology and settlement process.

Stage 6: Grid Connection Application

Grid connection application to the Netzbetreiber (distribution network operator) is typically the longest-lead-time item in community solar project development. Application must include:

- Single-line diagram with protection concept

- System size, inverter specifications, and proposed grid injection point

- For Mieterstrom: metering concept document

- For GGV: proposed allocation key methodology

Bundesnetzagentur regulations require Netzbetreiber to process connection applications within 8 weeks (simplified procedure) or 3 months (standard). In practice, urban network operators frequently exceed these timelines, particularly for novel models like GGV. Escalation procedures exist under §18 EnWG but are underutilized by small cooperative developers.

Stage 7: Installation and Commissioning

Standard community solar installation follows conventional PV commissioning procedures plus community-model-specific steps:

- Individual meter installation per unit (Mieterstrom) or building-level GGV meter configuration

- Grid operator inspection and formal commissioning approval (Inbetriebnahmeprotokoll)

- EEG registration update in MaStR with commissioning date

- For Mieterstrom: execution of individual Mieterstromverträge with participating tenants

- For cooperatives: member notification of project commissioning and initial production reporting

Stage 8: Ongoing Operations and EEG Settlement

Community solar projects have ongoing operational requirements beyond a standard residential installation:

- Monthly EEG settlement data submission to Netzbetreiber

- Annual yield reporting to the Bundesnetzagentur via MaStR

- For Mieterstrom: monthly billing of participating tenants and management of opt-out/opt-in changes

- For cooperatives: annual Prüfung by the Prüfungsverband, annual accounts preparation, AGM organization

- System performance monitoring with deviation analysis against the yield model

Financing Models for German Community Solar

Community solar projects in Germany use several financing structures, often in combination. The choice of financing model affects project economics, risk allocation, and citizen participation structure.

Model 1: Pure Cooperative Equity Financing

The simplest model: the cooperative raises all project capital from member share purchases, with no external debt.

| Parameter | Typical Range |

|---|---|

| Cooperative share size | €100–€10,000 per member |

| Number of members required for 500 kWp project at €800/kWp | ~100 members at €4,000 average investment |

| Expected dividend (annual) | 3–5% on share capital |

| Time to raise capital | 6–18 months |

| Advantage | No interest cost; simple legal structure; full member control |

| Disadvantage | Capital raising is slow; limits project scale to member base depth |

Model 2: Cooperative Equity + Bank Debt

The most common structure for mid-scale cooperative projects (200 kWp – 5 MWp):

| Parameter | Typical Range |

|---|---|

| Equity ratio | 30–50% (cooperative member shares) |

| Debt ratio | 50–70% (cooperative bank loan) |

| Debt interest rate (2026) | 4.5–6.5% (cooperative bank; project finance terms) |

| Lenders | Volksbank, Raiffeisenbank, KfW for qualifying projects |

| Loan term | 15–20 years (matched to EEG contract period) |

| KfW IKK 270 relevance | KfW’s renewable energy loan program at favorable rates; available to cooperatives |

| Project IRR (levered) | 6–12% depending on debt cost and project yield |

KfW’s Erneuerbare Energien Standard program (IKK 270) provides low-interest loans for renewable energy projects at rates currently 50–100 basis points below market. Cooperative borrowers with strong Prüfungsverband audit history and established financial records are well-positioned for KfW financing.

Model 3: Landlord Direct Investment (Mieterstrom)

For Mieterstrom projects, the most common financing structure is direct landlord investment, often combined with a soft loan from KfW or a regional development bank (Landesbank):

| Parameter | Typical Value |

|---|---|

| Landlord equity | 20–40% of capex |

| KfW 270 / regional bank loan | 60–80% of capex |

| Interest rate (2026) | 4.0–5.5% |

| Loan term | 10–15 years |

| Property value impact | Positive — solar Mieterstrom systems increase building income and energy performance rating |

| EPC contractor financing | Some larger EPC contractors offer lease/PPA structures to reduce landlord upfront cost |

Pro Tip — EPC Lease vs. Landlord Ownership

Several German EPC companies now offer Mieterstrom-as-a-service models where the EPC contractor owns and operates the system while sharing tenant electricity revenue with the landlord. This eliminates landlord upfront capital outlay but reduces long-term returns significantly — the EPC contractor captures the majority of the economics. Landlords with access to KfW 270 financing should generally own the system directly; the only scenario where EPC lease makes sense is when the landlord has exhausted debt capacity or has a very short planning horizon.

Model 4: Crowdfunding and Digital Share Issuance

A growing number of German energy cooperatives are using digital investment platforms to raise citizen equity beyond their immediate geographic catchment. Platforms such as Bettervest, Wiwin, and Econeers operate under the German crowdfunding regulation (§2a VermAnlG), which allows platforms to facilitate cooperative share offers up to €6 million without a full BaFin-regulated prospectus.

This model allows geographically dispersed citizen investors to participate in community solar projects beyond their immediate region — expanding the potential investor base from a local village to a national audience.

ROI Comparison Across Community Solar Models

| Model | System Size | Investment | Annual Return | Simple Payback | 20-Year IRR |

|---|---|---|---|---|---|

| Mieterstrom (50 kWp) | Apartment rooftop | €57,000 | ~€13,000/yr | 4–5 years | 7–10% |

| Cooperative ground-mount (500 kWp) | Rural ground-mount | €400,000 | ~€30,000/yr (member distributions) | 12–15 years for equity | 4–7% |

| GGV (150 kWp, mixed-use) | Commercial/residential | €135,000 | ~€18,000/yr | 7–8 years | 6–9% |

| Cooperative rooftop EEG (100 kWp) | Industrial rooftop | €85,000 | ~€8,500/yr | 9–11 years | 4–6% |

Returns are pre-tax. Mieterstrom and GGV returns reflect all revenue streams. Cooperative ground-mount return reflects EEG feed-in at 2026 rates. Individual project economics vary materially by location, shading, electricity price, and financing cost.

Electricity Price Sensitivity

The single most important long-run variable for German community solar ROI is the future trajectory of residential electricity prices. With Germany’s grid fees (Netzentgelte) subject to ongoing reform discussions and the planned phase-out of small-system EEG subsidies, uncertainty around the electricity price that solar displaces is the primary risk factor for 20-year financial models.

| Electricity Price (€/kWh) | 50 kWp Mieterstrom Payback | 20-Year IRR |

|---|---|---|

| €0.25 (bear case) | 7.5 years | 5.2% |

| €0.32 (base case, 2026 level) | 5.8 years | 7.8% |

| €0.40 (moderate growth) | 4.6 years | 10.4% |

| €0.45 (high-price scenario) | 4.1 years | 12.1% |

Germany’s residential electricity prices have averaged €0.30–€0.38/kWh in 2025–2026. The Netzentgeltreform currently under discussion in the Bundesministerium für Wirtschaft und Klimaschutz could reduce grid fees by 2–4 ct/kWh — a potential headwind for community solar economics that financial models should include as a bear-case scenario.

How SurgePV Supports Community Solar Project Design

Community solar projects — whether Mieterstrom installations on apartment blocks, cooperative ground-mount arrays, or multi-building GGV systems — involve significantly more design complexity than a standard residential installation. A single-home PV system requires one roof, one meter, one irradiance dataset, and one financial model. A 50-unit Mieterstrom project requires multiple roof planes with different orientations and tilt angles, variable shading from adjacent urban buildings, a shared metering configuration, per-tenant revenue attribution logic, and a financial model that can distinguish between EEG feed-in, Mieterstromzuschlag, and tenant tariff revenue streams.

Standard residential design tools are not built for this complexity. Professional solar design software purpose-built for European markets provides the capabilities community solar projects require: multi-roof modeling, accurate 3D shadow analysis, EEG parameter integration, and investor-grade financial proposal output — all within a single workflow.

Multi-Roof and Multi-Orientation Design

Urban Mieterstrom buildings rarely present a single flat south-facing roof. Gründerzeit apartment blocks in Berlin, Hamburg, and Leipzig typically have complex roof geometries — multiple pitches, dormers, chimneys, and elevator shafts interrupting otherwise usable area. A 20-unit building might have four distinct roof sections at different orientations and tilt angles, each requiring separate string optimization and yield modeling.

Solar design software that handles multi-roof, multi-orientation layouts — with per-string yield simulation rather than simple average-irradiance scaling — produces fundamentally more accurate yield estimates for these buildings. A 10% yield overestimate on a €57,000 Mieterstrom system represents €5,700 in missing revenue relative to financial projections — enough to shift payback from 4.3 years to 5+ years and cause genuine financial model failure.

Shadow Analysis for Urban Community Solar

Urban Mieterstrom projects face acute shading challenges. Multi-story buildings in dense German cities are closely spaced — particularly in Gründerzeit-era blocks — and a rooftop can receive shade from adjacent buildings for several hours daily, especially in winter when solar angles are low.

Solar shadow analysis software that models near-shading from 3D building datasets is the essential quality control tool for urban community solar yield estimates. Overestimating annual yield by 15–20% due to unaccounted shading is the single most common cause of Mieterstrom project underperformance — and the most common source of legal disputes between landlords and installers. A thorough shadow analysis conducted before financial close eliminates this risk at a fraction of the cost of the dispute it prevents.

For GGV projects, accurate monthly yield profiles are additionally needed to populate the allocation key settlement model submitted to the Netzbetreiber. Monthly yield data from a shading-corrected simulation is substantially more accurate than monthly data derived from annual yield divided by 12 using an average monthly irradiance curve.

Design Community Solar Projects Faster with SurgePV

Model multi-roof Mieterstrom systems, run accurate shade analysis for urban buildings, and generate cooperative-ready financial proposals — all in one platform built for European solar markets.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

Proposal Generation for Cooperative Boards and Building Owners

An Energiegenossenschaft AGM vote on a new solar project requires substantially more than a back-of-envelope yield estimate. Cooperative members — ranging from farmers and retirees to local businesspeople and university lecturers — need a clear, credible financial model: annual yield projection with monthly breakdown, revenue attribution across EEG feed-in and Mieterstromzuschlag streams, payback period, IRR across the 20-year project life, and sensitivity analysis on electricity price assumptions.

Solar proposal software purpose-built for European markets outputs investor-grade documents suitable for AGM distribution and filing with the cooperative’s Prüfungsverband. For installers targeting the cooperative sector, proposal quality is a material competitive differentiator. Cooperative boards have encountered too many optimistic projections from installers using back-of-envelope methods — a professionally modeled proposal with transparent assumptions commands credibility that generic PDF proposals cannot match.

For Mieterstrom landlord presentations, solar proposal software that automatically segments revenue by EEG feed-in, Mieterstromzuschlag, and tenant tariff — and presents sensitivity to tenant participation rate and electricity price — provides the financial clarity that building owners need to make investment decisions with confidence.

Battery Storage Integration for Community Projects

Battery storage integration into community solar projects requires design beyond standard residential battery sizing. Community Mieterstrom systems benefit from battery storage in three ways:

- Self-consumption increase: shifting midday generation surplus to evening peak tenant demand raises the tenant-consumed share from a typical 55–65% to 70–85%, directly increasing Mieterstromzuschlag-eligible kWh

- Negative-price protection: the Solarspitzengesetz zero-feed-in rule during negative market prices is mitigated by a battery that absorbs generation during negative-price periods and discharges during positive-price periods

- Partial autarky: for buildings in GGV projects seeking a higher Autarkgrad, battery storage can meaningfully reduce residual grid imports

Battery capex has fallen to €400–€600/kWh installed for LFP systems at community scale. For Mieterstrom projects above 30 kWp, battery integration typically improves project IRR by 1–2 percentage points — a meaningful improvement on a 20-year financial model.

For Solar Professionals: Targeting the German Community Solar Market

Germany’s community solar market in 2026 is underserved by installers with genuine community model expertise. Most residential solar installers in Germany focus on standard owner-occupied installations where EEG registration is straightforward, financial modeling is simple, and the customer is a homeowner with direct decision-making authority.

Community solar projects — with their cooperative governance structures, Mieterstrom legal requirements, GGV settlement complexity, and multi-stakeholder decision processes — require a different commercial and technical approach. For installers willing to invest in that expertise, the commercial opportunity is substantially larger:

- A 50 kWp Mieterstrom project generates 5–8x the revenue of a 10 kWp residential installation

- Cooperative clients commission recurring projects across their portfolio, providing predictable project pipeline rather than one-off homeowner leads

- Community solar references build credibility in adjacent commercial and industrial segments where multi-roof, multi-tenant complexity is also the norm

For additional context on the broader German solar market environment in which community projects operate, see our guides to solar incentives and subsidies Germany, solar subsidies Germany, and solar software Germany.

For European solar policy context, the solar panel ROI Italy analysis provides a useful comparison of how different regulatory architectures shape community solar economics across European markets.

Conclusion

Germany’s community solar market in 2026 is more legally sophisticated, more economically compelling, and more broadly accessible than at any point in the Energiewende’s history. Solarpaket I resolved the metering infrastructure barrier with the Gemeinschaftliche Gebäudeversorgung model. EEG 2023 removed the Mieterstrom national capacity cap. Germany’s 800–900 active energy cooperatives manage over €2 billion in citizen-owned renewable assets. And Solarpaket II, when enacted, will address the grid access bottlenecks that currently extend community project timelines by months.

Three actions for solar professionals targeting Germany’s community solar market in 2026:

1. Master the framework choice between Mieterstrom and GGV. These are not competing programs — they are complementary tools for different building types and sizes. Installers who can accurately assess which model delivers better economics for a specific building, and explain that analysis clearly to a building owner or cooperative board, are positioned to win projects that competitors cannot even properly scope.

2. Invest in professional financial modeling. The 4–7 year payback and 6–10% IRR available from well-designed Mieterstrom projects are highly competitive returns for property owners and cooperative members. But achieving those outcomes depends on accurate yield modeling, proper accounting of all revenue streams, and credible sensitivity analysis. Generic proposal tools built for simple residential systems produce neither the accuracy nor the presentation quality these projects require.

3. Build cooperative sector relationships deliberately. Germany’s 800+ active energy cooperatives represent a predictable, high-value project pipeline for installers who earn their trust. Cooperatives commission multiple projects over their operational life, provide referrals within cooperative networks, and — crucially — make procurement decisions based on technical credibility and proposal quality rather than lowest price. Winning one Energiegenossenschaft as a long-term partner can be worth more than dozens of one-off residential installations.

Frequently Asked Questions

How does Mieterstrom work in Germany?

Mieterstrom (tenant electricity) allows a landlord to install rooftop solar on an apartment building and supply power directly to tenants at a discounted rate — legally capped at 90% of the applicable local standard grid tariff. The landlord receives an EEG Mieterstromzuschlag supplement on every kWh delivered directly to tenants, paid on top of the standard feed-in tariff for grid exports. Since EEG 2023 removed the 100 kWp system-size cap and the national 500 MW expansion cap, virtually any qualifying multi-family building can access the program. In 2026, the supplement runs approximately €2.5–3.8 ct/kWh depending on system size. Tenants typically pay 10–20% below the local Grundversorger rate.

What is Bürgerenergie in Germany?

Bürgerenergie (citizen energy) refers to community-owned renewable energy projects where local residents are the investors, operators, and primary beneficiaries. Most Bürgerenergie projects are structured as Energiegenossenschaften — registered cooperatives under German cooperative law (GenG) — where each member holds one vote regardless of share size. Members typically invest €100–€500 per share and receive annual dividends of 3–5%, sometimes paired with discounted electricity tariffs. Germany has approximately 800–900 active energy cooperatives, with Bürgerwerke eG aggregating 113 of them and over 50,000 members nationwide.

What did Solarpaket I change for community solar projects in Germany?

Solarpaket I (enacted May 2024) made five changes directly relevant to community solar: (1) It introduced the Gemeinschaftliche Gebäudeversorgung model, allowing shared solar supply within multi-unit buildings without per-unit smart metering; (2) It simplified Balkonkraftwerk registration to Bundesnetzagentur notification only, removing the Netzbetreiber consent requirement; (3) It expanded Mieterstrom eligibility to include systems on buildings immediately adjacent to the supply building; (4) It reduced bureaucratic requirements for cooperative projects under 500 kWp; and (5) It raised the EEG registration exemption threshold for small systems. Together, these changes made urban community solar substantially more accessible than at any previous point in the Energiewende.

What is Gemeinschaftliche Gebäudeversorgung and how does it differ from Mieterstrom?

Gemeinschaftliche Gebäudeversorgung (GGV) is a new shared building energy supply model introduced by Solarpaket I. Unlike classic EEG Mieterstrom, which requires individual smart meters for each participating tenant unit, GGV uses pre-agreed allocation keys (based on floor area, resident count, or historical consumption) to distribute a building’s total solar generation across participants without per-unit real-time metering. GGV applies to both residential and mixed-use buildings up to 500 kWp — larger than the 100 kWp Mieterstromzuschlag eligibility limit. The trade-off: GGV does not qualify for the Mieterstromzuschlag supplement, but it saves €3,000–€12,000 in metering infrastructure on larger buildings, often improving overall project economics.

How do I join or start an energy cooperative in Germany?

To join an existing Energiegenossenschaft, search the Bürgerwerke network (buergerwerke.de), your regional Energieagentur, or the DGRV cooperative register. Review the cooperative’s annual Prüfungsbericht before investing, then purchase Geschäftsanteile (shares) at the minimum investment threshold (typically €100–€500). To start a new cooperative, you need at least three founding members, a Satzung (articles of association) — DGRV provides standard templates — and registration at the Amtsgericht. Mandatory membership in a Prüfungsverband (auditing association) follows registration. Total setup cost runs €3,000–€8,000; timeline from planning to registered cooperative is 3–6 months.

What are current EEG Mieterstromzuschlag rates in Germany?

The EEG Mieterstromzuschlag rates in 2026 run approximately €3.8 ct/kWh for systems up to 10 kWp, €3.1 ct/kWh for systems between 10–40 kWp, and €2.5 ct/kWh for systems between 40–100 kWp. Systems above 100 kWp are not eligible for the Zuschlag — projects at that scale should use the Gemeinschaftliche Gebäudeversorgung model instead. Rates are set quarterly by the Bundesnetzagentur and are subject to degression; always verify current rates at bundesnetzagentur.de before project financial close.

How does Solarpaket II affect community solar grid access?

Solarpaket II, currently in the German legislative process as of March 2026, targets the grid access barriers that have slowed community solar project development under the Solarpaket I framework. Key proposed changes include statutory grid connection timelines with financial penalties for Netzbetreiber who miss them, simplified virtual net metering for cooperative projects supplying members at multiple grid locations, and regulatory support for aggregating multiple small cooperative installations into a single market participant. Until Solarpaket II is enacted, project developers should plan under current Solarpaket I grid access rules while monitoring legislative progress through the Bundestag.