When Russia’s full-scale invasion of Ukraine began in February 2022, Europe was importing over 40% of its natural gas from a single supplier. Within weeks, that dependency transformed from an energy policy concern into a national security emergency. The European Commission’s response — REPowerEU — was published in May 2022 and represented the most ambitious reorientation of European energy policy since the creation of the internal energy market.

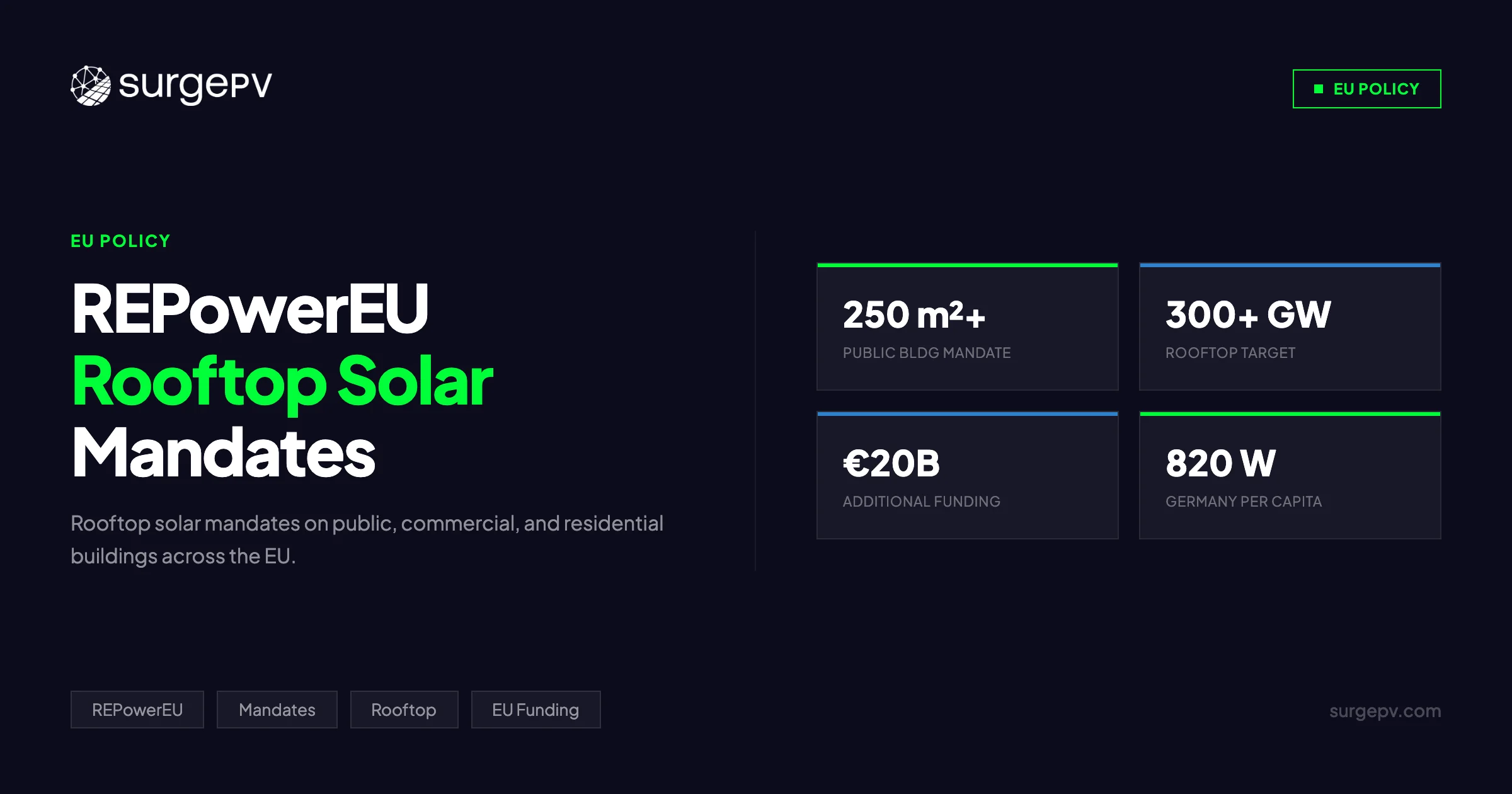

At the centre of REPowerEU’s supply-side strategy is rooftop solar. Not as a supporting measure. As a primary instrument. For the first time in EU history, the plan mandated that new buildings must be built with solar panels installed — a requirement that fundamentally changes the business environment for every solar installer, engineering firm, and property developer operating across the continent.

This guide covers what REPowerEU actually requires, the national implementation status country by country as of March 2026, how the funding mechanisms work, what the permitting reform means operationally, and what solar installers should be doing right now to position for the demand wave this mandate is creating.

TL;DR — REPowerEU Rooftop Solar 2026

REPowerEU mandates rooftop solar on all new public and commercial buildings over 250 m² from 2026, existing public buildings over 250 m² from 2027, and all new residential buildings from 2029. The EU is targeting 600 GW of total solar capacity by 2030, with over 300 GW expected to come from rooftops. A €20 billion additional funding envelope — drawn from emissions trading revenues — is channelled through national Recovery and Resilience Plans. Permitting must now be completed within three months for rooftop systems. The mandate creates a mandatory, policy-driven customer base that is unlike any demand environment European solar installers have seen before.

In this guide:

- Latest 2026 implementation updates by country — who is ahead, who is behind

- REPowerEU plan overview and the 600 GW solar target

- Rooftop solar obligation: exact building categories and timelines

- National implementation status: Germany, France, Spain, Italy, Netherlands, and Eastern Europe

- Grid connection streamlining and the one-stop-shop permit requirement

- EU Solar Energy Strategy: industrial and skills framework

- Financing mechanisms: InvestEU, RRF REPowerEU chapter, national development banks

- How the mandate creates a structural installer opportunity

- Permit process simplification: what has changed and what remains

- What installers should do now to prepare

Latest Updates: REPowerEU Solar Mandate Implementation 2026

The picture across Europe as of March 2026 is one of significant variation. The mandate framework is clear at EU level; the question in each member state is whether transposition legislation, grid infrastructure, permitting reform, and installer capacity are keeping pace.

REPowerEU Solar Mandate — Implementation Status by Country (March 2026)

| Country | Mandate Transposed? | New Buildings Obligation | Existing Public Buildings | Permitting Reform | Primary Bottleneck |

|---|---|---|---|---|---|

| Germany | Yes (partial) | In force for public buildings; residential from 2029 | 2027 deadline | Ongoing; state-level variation | Grid connection delays |

| France | Yes | Public buildings in force; parking lots from 2023 | Legislation passed | Digital permitting piloted | Urban structural constraints |

| Spain | Yes | Public buildings mandate active | 2027 under PNIEC | Regional variation | Rooftop mapping quality |

| Italy | Partial | Regional variation; national framework pending | 2027 draft | Digital system incomplete | Bureaucratic complexity |

| Netherlands | No formal mandate | High voluntary adoption | N/A | Streamlined | Grid congestion |

| Poland | No | Voluntary incentives only | No deadline set | Not reformed | Low installer capacity |

| Romania | No | Preliminary legislation | No deadline set | Not reformed | Grid infrastructure |

| Austria | Yes | New buildings from 2025 | 2026 for federal buildings | Reformed | Limited; well-managed |

| Belgium | Partial (regional) | Flanders mandate in force | Varies by region | Regional | Wallonia lagging |

| Sweden | In progress | Legislation under consultation | No fixed deadline | Reformed | High voluntary adoption reduces urgency |

Key Developments Since January 2026

Germany’s revised Building Energy Act (GEG) update came into force in January 2026, extending rooftop solar requirements to all new non-residential buildings above 100 m² in states that have adopted the federal framework. Bavaria and Baden-Württemberg both exceeded the federal minimum.

France’s Agrivoltaïsme law (effective 2025) added a rooftop solar carve-out requiring solar on new agricultural storage and logistics buildings above 500 m² — expanding the mandate category beyond the original REPowerEU scope.

Spain’s Royal Decree 1183/2020 implementing self-consumption regulations has been extended, and the Ministry for Ecological Transition confirmed in February 2026 that all new public authority buildings must reach permitting stage for rooftop PV by Q3 2026 or face EU funding penalties.

Italy’s PNRR Chapter 6 (REPowerEU additions) allocated €1.7 billion specifically to rooftop solar on public buildings and school infrastructure. The GSE (Gestore dei Servizi Energetici) opened a new competitive application round in January 2026 targeting municipalities with fewer than 50,000 residents.

Netherlands grid congestion remains the most acute implementation constraint in Europe. Liander and Enexis — the major distribution system operators — have declared grid capacity saturation in significant portions of their service territories, creating de facto installation moratoriums for new grid-connected systems in affected postcodes.

Key Takeaway — Mandate vs. Capacity Gap

Across Europe, the gap is not between ambition and policy — the mandates exist. The gap is between installed permitting infrastructure, grid connection capacity, and trained installer workforce on one side, and the volume of buildings entering the mandatory solar obligation category on the other. Countries that resolve this gap fastest will capture the most economic benefit from the mandate.

REPowerEU: Plan Overview and the 600 GW Solar Target

REPowerEU is the European Commission’s plan to rapidly reduce dependence on Russian fossil fuels following the 2022 invasion of Ukraine. Published on 18 May 2022 — less than three months after the conflict began — it set out a combination of demand reduction measures, supply diversification across energy sources, and an accelerated renewables buildout.

For solar specifically, REPowerEU set a target of 600 GW of installed solar PV capacity by 2030 — roughly doubling the EU’s capacity within eight years. This was an upward revision of the 2021 Fit for 55 target, which had anticipated approximately 420 GW by 2030.

Why Rooftops?

The 600 GW target cannot be met from ground-mounted utility-scale solar alone. Land availability, grid connection distances, planning complexity, and agricultural land protection rules all constrain large-scale ground-mount deployment. Rooftops represent an enormous, already-connected, widely distributed resource that sits within existing grid infrastructure.

The Commission’s analysis identified approximately 25 billion m² of solar-suitable rooftop area across the EU — enough to host over 600 GW if converted to PV at a 25% utilisation rate. A 2023 mapping exercise using satellite and Copernicus data brought this into sharper focus: 320 million m² of commercial, industrial, and public building rooftops alone were classified as high-suitability surfaces, capable of hosting approximately 150–170 GW of capacity.

The 600 GW Milestone Timeline

| Year | EU Solar Installed Capacity Target | Rooftop Contribution | Key Policy Driver |

|---|---|---|---|

| 2022 | ~207 GW (actual, year-end) | ~75 GW | REPowerEU published |

| 2023 | ~263 GW (actual, year-end) | ~95 GW | Solar Rooftop Initiative in force |

| 2024 | ~320 GW (estimated actual) | ~120 GW | NRRPs updated with REPowerEU chapters |

| 2025 | ~390 GW (target) | ~150 GW | Permitting streamlining effective |

| 2026 | ~450 GW (target) | ~180 GW | New public/commercial building mandate active |

| 2027 | ~510 GW (target) | ~220 GW | Existing public building deadline |

| 2029 | ~570 GW (target) | ~270 GW | Residential new-build mandate active |

| 2030 | 600 GW (target) | 300+ GW | Full mandate in effect |

The EU was tracking at approximately 320 GW by end-2024 — ahead of the linear trajectory but still requiring significant acceleration to hit 600 GW by 2030. Annual additions need to average around 45–50 GW per year through 2030, up from the record 56 GW added in 2023.

Strategic Context: Energy Independence

The quantified energy independence rationale matters for anyone doing policy-based financial modelling. REPowerEU’s modelling projected that achieving the 600 GW solar target would allow the EU to replace approximately 170 billion cubic metres of Russian natural gas per year — equivalent to roughly two-thirds of pre-war import levels. Every gigawatt of rooftop solar capacity reduces that dependence without requiring new land, new long-distance transmission infrastructure, or new import contracts.

This is why rooftop solar moved from voluntary best practice to statutory obligation. The energy security argument gave the Commission legal and political justification to mandate it in a way that climate-only arguments had not.

The Rooftop Solar Obligation: Building Categories and Timelines

The Solar Rooftop Initiative — embedded within the revised Energy Performance of Buildings Directive (EPBD) and directly referenced in REPowerEU — establishes mandatory solar installation requirements across building categories with phased timelines. Here is exactly what is required and when.

New Public and Commercial Buildings (2026 Deadline)

All new public buildings and new commercial buildings with a floor area above 250 m² must be designed and built with rooftop solar panels installed. The obligation applies to building permit applications submitted from 1 January 2026 onward in member states that have fully transposed the requirement.

“New public buildings” covers government offices, schools, hospitals, universities, court buildings, and any structure where public authority bodies are the principal occupant. “New commercial buildings” covers retail, offices, logistics, light industrial facilities, and mixed-use developments where the primary use is commercial.

The obligation does not specify a minimum system size in watts — it requires solar to be installed on all technically suitable roof surfaces, with exemptions available only where:

- Structural load-bearing capacity of the roof is insufficient

- Shading from neighbouring buildings or terrain makes the installation technically unviable (typically defined as fewer than 800 peak sun hours per year on the available surface)

- The building is classified as a heritage or protected structure under national law

Existing Public Buildings (2027 Deadline)

All existing public buildings with a floor area exceeding 250 m² must have rooftop solar installed by 2027. This is the most significant volume category in terms of building count — Europe has an enormous existing public building stock, much of it built before 1990, with rooftops that have never been assessed for solar.

The 2027 deadline is a hard policy deadline tied to REPowerEU milestone reporting to the Commission. Member states that fail to demonstrate adequate progress risk losing access to RRF funds allocated under the REPowerEU chapter of their national recovery plans.

In practical terms, reaching 2027 compliance requires that every municipality, school board, hospital authority, and government agency have either completed installation or obtained permits with a scheduled installation date by the deadline.

New Commercial/Industrial Buildings Above 500 m² (2027)

A supplementary obligation applies to new commercial and industrial buildings with a floor area above 500 m² from 2027 (some member states have adopted 2026 as the effective date in their national transpositions). This category includes logistics warehouses, manufacturing facilities, supermarkets, and retail parks — precisely the building types with the largest roof areas and the greatest capacity per installation.

A standard logistics warehouse of 10,000 m² can host 700–900 kWp of rooftop solar. The largest logistics facilities — 40,000–80,000 m² — represent multi-megawatt installations. The commercial/industrial segment may ultimately deliver more total capacity under this mandate than the public buildings segment, despite the public building headline.

New Residential Buildings (2029 Deadline)

All new residential buildings — houses, apartment blocks, mixed residential developments — must have rooftop solar installed from 2029. This is the most far-reaching element of the mandate in terms of volume: residential buildings represent by far the largest category of construction across the EU.

The 2029 date was chosen to give the construction industry, architectural profession, and national grid operators time to adapt. Solar-ready electrical design must be incorporated from the outset; retrofitting solar to a building that was not designed for it is significantly more expensive.

Major Renovations

Any renovation project that involves replacing, materially modifying, or significantly upgrading the roof structure of a building that already falls within one of the above categories also triggers the solar obligation. This prevents the simple avoidance mechanism of re-roofing without installing solar.

Pro Tip — Mandate Eligibility Assessment

When quoting a renovation project on any public, commercial, or residential building, run a quick mandate eligibility check upfront: floor area above threshold, roof structure suitable, permit date relative to mandate effective date. Presenting the compliance obligation to a building owner before they have engaged a competitor positions your firm as the knowledgeable partner — not just a price on a quote sheet. Use solar design software that can generate rapid roof suitability assessments from address-level data to make this a standard part of your sales process.

National Implementation Status: Country by Country

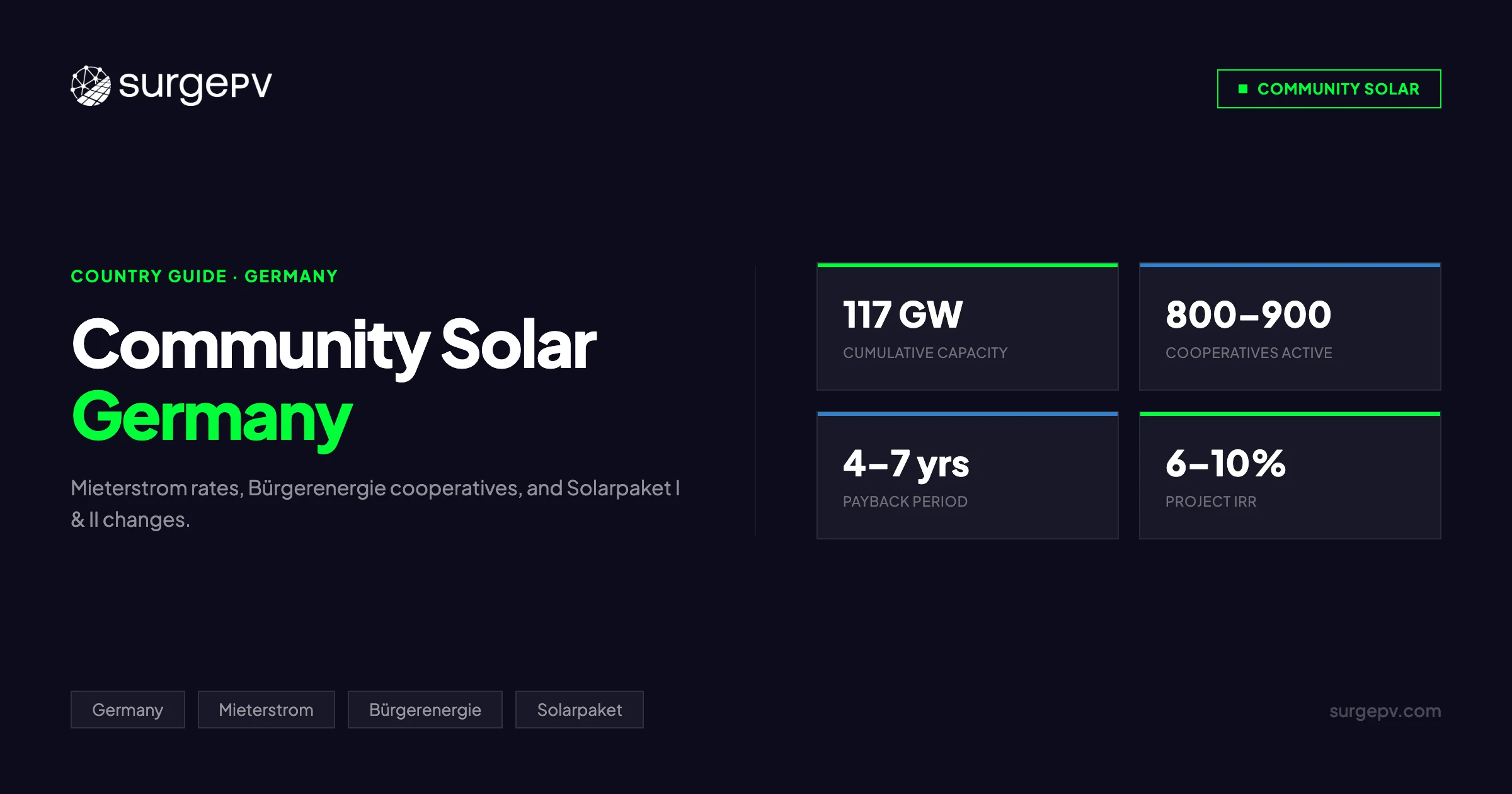

Germany

Germany entered the REPowerEU era with significant existing rooftop solar capacity — over 820 W per capita installed by end-2024, more than double the EU average — but a regulatory framework that has complicated further acceleration.

The Erneuerbare-Energien-Gesetz (EEG) 2023 reform expanded feed-in tariffs for rooftop systems and introduced simplified grid connection rules for systems under 30 kW. More significantly, the reform removed the long-standing cap on rooftop solar feed-in — systems can now export 100% of generation without penalty, rather than the previous 70% cap that was a major economic disincentive.

At state (Bundesland) level, implementation varies substantially:

- Baden-Württemberg mandates solar on all new residential buildings above 50 m² from 2022 — the most aggressive residential mandate in Germany, predating the EPBD revision

- Bavaria requires solar on all new commercial buildings and new car parks from 2023

- Berlin requires solar on new buildings and major roof renovations from 2023

- Hamburg, Hesse, and Rhineland-Palatinate have adopted similar requirements

The federal government’s permitting target — standardised approval within six weeks for rooftop systems — has not been uniformly achieved. In practice, grid connection approval from local distribution system operators (Netzbetreiber) remains the primary bottleneck, with waits of four to nine months common in suburban and semi-rural areas.

Germany needs approximately 25,000–30,000 additional solar installation technicians to meet its component of the EU target. Apprenticeship programs have expanded, but the workforce gap will constrain installation pace through at least 2027.

France

France’s implementation has been notable for the depth of mandate breadth — extending the obligation beyond buildings to car parks — and for early adoption of digital permitting tools.

Mandatory solar on parking lots (installations of 80 or more spaces) took effect in July 2023, followed by a January 2024 extension to parking facilities of 500 or more spaces that must achieve 50% coverage. This alone is expected to add 6–11 GW of capacity as developers retrofit the enormous covered parking stock serving French retail parks and logistics facilities.

For buildings, France implemented the EPBD requirements through amendments to the Code de la Construction et de l’Habitation. New public buildings above 1,000 m² must have solar installed from 2023; the 250 m² threshold aligned with the REPowerEU mandate takes effect from 2026 consistent with EU requirements.

The ADEME (Agence de la Transition Écologique) manages grant distribution for rooftop solar, with residential systems eligible for a tax credit (Crédit d’Impôt) of 30% on equipment costs. Commercial and public building projects can access grants of €400–€650 per kWp through regional ADEME envelopes.

Digital permitting — the Permis en Ligne system — has reduced approval times by up to 40% in cities that have adopted it. Lyon, Marseille, Nantes, and Toulouse are leading deployments; smaller municipalities are still on manual processes.

One structural challenge in France is the concentration of solar installation capacity in southern regions (Provence-Alpes-Côte d’Azur, Occitanie) while mandate obligations apply equally to the cooler north. Installer firms in Normandy and Brittany report the lowest margins in Europe due to lower irradiance and higher heating loads making solar-only systems harder to sell without battery and heat pump integration.

Spain

Spain’s regulatory environment has undergone a transformation since 2019. The removal of the so-called “sun tax” — which had imposed grid charges on self-consumed solar generation — was followed by Royal Decree 244/2019 establishing net metering (compensación simplificada) for systems under 100 kW, and Royal Decree 1183/2020 creating a streamlined self-consumption registration process.

Under REPowerEU, Spain’s national implementation focuses on the public building mandate. The Ministerio para la Transición Ecológica y el Reto Demográfico confirmed in 2024 that all new public buildings above 250 m² require solar panel installation at permit stage. Regional governments (autonomous communities) have adopted additional requirements — Catalonia, the Basque Country, and the Balearic Islands all have rooftop solar mandates that predate the national framework.

The NextGen EU recovery funds — Spain’s RRP allocates approximately €3 billion to renewable energy self-consumption — offer subsidies of €600–€1,100 per kW for rooftop installations depending on system size and the degree of self-consumption. Community energy projects receive a supplementary incentive.

Spain’s primary implementation challenge is rooftop mapping quality in smaller municipalities. Urban centres have adequate cadastral and aerial data; rural towns frequently lack the parcel-level data needed to determine which buildings meet the mandate threshold and whether structural and shading constraints apply. Several autonomous communities are running satellite mapping programs to close this gap.

For a detailed analysis of Spanish solar incentive structures and how they interact with self-consumption economics, see our guide to European solar incentives.

Italy

Italy presents the most complex implementation picture in Western Europe. On paper, the REPowerEU framework applies fully. In practice, the implementation is fractured along regional lines, slowed by administrative complexity, and still catching up with the volume implied by the mandate.

Italy’s PNRR (Piano Nazionale di Ripresa e Resilienza) allocated €2.2 billion to solar energy measures under the REPowerEU chapter. The largest single allocation — €1.7 billion — targets public building solar installations administered through GSE. A second tranche covers residential installations in economically deprived areas.

The primary residential incentive has shifted away from the Superbonus (which is now effectively closed for standalone solar applications) toward the Detrazione Fiscale 50% — a 10-year income tax deduction covering 50% of system cost — and net metering through GSE’s Scambio sul Posto mechanism. Energy communities (Comunità Energetiche Rinnovabili) under the 2024 CER Decree offer up to €110/MWh on shared virtual self-consumption.

For public and commercial buildings, the mandate implementation is proceeding through a combination of GSE competitive tenders and direct grants to municipal governments. The complication is Italy’s dual permit system: solar installations require both a building permit (SCIA or CILA depending on system size and municipality) and a grid connection agreement from the local distribution operator. These processes run on different clocks and through different agencies, creating coordination failures that delay projects by six to eighteen months in some regions.

The south — Puglia, Sicilia, Calabria — has the best solar resource and some of the most active grant programs (Puglia’s POR FESR offers €500–€2,000 per residential installation). But it also has the weakest grid infrastructure for absorbing distributed generation, with Terna reporting saturation in several southern transmission zones.

For detailed Italian solar incentive data and ROI calculations, see our dedicated guide to solar energy policies in Europe.

Netherlands

The Netherlands has reached extraordinary rooftop solar penetration through voluntary adoption rather than mandate. With over 1,000 W per capita installed — the highest in the EU — the Dutch residential and commercial solar market is a demonstration of what strong net metering economics and straightforward permitting can achieve without binding legal obligations.

The primary 2026 challenge in the Netherlands is no longer installation demand — it is grid absorption capacity. Liander, Enexis, and Stedin have issued formal grid congestion declarations for substantial portions of their service territories. In the most affected areas, new grid connection applications for solar systems above 25 kW are being rejected or delayed by 24–36 months pending grid reinforcement.

The Dutch government’s response — the Energy System Act (Energiewet), which came into force in 2024 — establishes new rules for demand flexibility, smart charging, and storage integration. It also streamlines the cable pooling process that allows multiple solar installations to share a single grid connection point, which is the primary workaround for congestion constraints in industrial areas.

The Netherlands has not formally adopted the REPowerEU rooftop mandate in national legislation, since its existing voluntary market penetration already exceeds what the mandate would require for new buildings. However, the existing public building stock — schools, municipal offices, sports halls — still represents a significant addition potential, and several municipalities are running retrofit programs using RRF funding.

Eastern Europe: The Implementation Gap

Poland, Romania, Bulgaria, Hungary, and Slovakia collectively represent a significant implementation gap. Their National Recovery Plans include REPowerEU chapters with solar targets, but on-the-ground progress is substantially slower than in Western Europe.

Poland is the most significant case: the third-largest EU economy by GDP, with a coal-heavy energy mix and relatively weak solar resource compared to the south. Poland’s Mój Prąd (My Power) grant program has driven residential solar growth — Poland is now one of the top ten solar markets globally — but the commercial and public building mandate framework has not been formally adopted. Grid connection reform is ongoing but not complete.

Romania has significant renewable energy potential and substantial EU cohesion funding available for energy transition, but administrative capacity to manage grant distribution is limited. The rooftop solar market remains dominated by residential self-consumption systems funded through EU rural development grants.

Bulgaria faces both administrative and grid infrastructure constraints. The country’s electricity transmission system requires significant reinforcement before large-scale distributed rooftop solar can be accommodated, and the regulatory framework for prosumers (consumers who also generate electricity) was only clarified in 2023.

The Eastern European implementation gap matters for pan-European installers: it represents future demand that will eventually materialise once regulatory frameworks catch up, but the timeline is uncertain and the market entry barriers — language, regulatory complexity, grid limitations — are higher than in established markets.

Grid Connection Streamlining: The One-Stop-Shop Mandate

One of the most operationally significant elements of REPowerEU for installers is the mandate to streamline permitting. The EU Solar Energy Strategy required member states to establish one-stop-shop permitting processes for rooftop solar, with a maximum approval timeline of three months for residential and small commercial installations.

What the One-Stop-Shop Requires

The one-stop-shop concept means a single administrative contact point — whether a physical office, digital portal, or designated agency — that receives all documentation, coordinates with grid operators, building authorities, and heritage bodies, and issues a single decision. No sequential processing through separate agencies with independent timelines.

The three-month clock starts when a complete application is submitted. If additional documentation is requested, the clock pauses only for the duration of the information gap — not for internal processing time. If no decision is issued within three months, the application is deemed approved by default (a provision known as “silence is consent” in administrative law).

In practice, implementation of these rules across 27 member states has been uneven:

- France and Austria have the most functional one-stop-shop implementations, with digital portals that integrate building permit and grid connection workflows

- Germany has a functioning system at federal level, but state and municipal variations mean that the three-month target is not consistently met

- Italy and Spain have the one-stop-shop requirement on the statute books, but operational integration between building permit authorities and DSO grid connection processes has not been achieved in most jurisdictions

- Eastern EU member states have generally not operationalised the requirement

Pro Tip — Permitting Timelines in Your Bid

The three-month permitting target is a legal requirement, but your installation business runs on actual timelines. When building project schedules, use your current average permitting time rather than the regulatory target — and build in contingency for grid connection confirmation separately from building permit approval. Good solar design software that integrates permit workflow tracking lets you flag when a project’s grid connection approval is running past the statutory deadline, giving you grounds to escalate to the DSO formally.

Grid Connection Reform

Parallel to the permitting reform, REPowerEU required member states to reform grid connection procedures for rooftop solar. Key requirements include:

Net metering and simplified export agreements. Systems under 10.8 kW (3-phase, 50 A) must be granted grid connection without a formal power purchase agreement, using a standard simplified procedure. This removes a major bureaucratic step for residential systems.

Digital meter installation. All grid-connected solar installations must have a smart meter capable of recording bidirectional energy flows. Most member states had existing smart meter rollout programs; REPowerEU accelerated the timeline for solar-connected meters.

DSO transparency. Distribution system operators must publish grid capacity maps showing available connection capacity by geographic area. This is now operational in Germany, France, the Netherlands, and Austria; partial in Spain and Italy; not yet delivered in most Eastern EU states.

Cable pooling. New rules allow multiple generation assets (solar, battery, wind) to share a single grid connection point, reducing connection cost for industrial and commercial rooftop projects that previously needed separate DSO agreements for each technology.

EU Solar Energy Strategy: The Industrial Framework

The EU Solar Energy Strategy, published alongside REPowerEU, addresses the supply-side requirements for achieving the 600 GW target. It operates on three tracks: manufacturing, skills, and finance.

EU Solar PV Industry Alliance

The EU Solar PV Industry Alliance — a public-private partnership — was established to coordinate European solar panel manufacturing capacity. The goal: ensure that at least 30 GW per year of solar panel manufacturing capacity exists within the EU by 2030, reducing dependence on Asian supply chains.

As of 2025, this target is being missed. European manufacturing capacity sits at approximately 10–15 GW per year, with module costs from EU manufacturers running 20–35% above equivalent Asian-sourced products. The European Solar Manufacturing Council has lobbied for a local content requirement in public procurement — similar to the US Inflation Reduction Act’s domestic content provisions — but no binding EU requirement has been adopted.

The practical implication for installers is that EU-manufactured panels cost more. For public building projects funded through RRF grants, some national programs specify EU-manufactured equipment; verify this in tender documentation before specifying panels.

Solar Skills Partnership

The Solar Skills Partnership coordinates training and workforce development across member states to address the installer workforce gap. The Commission’s estimate is that the EU needs approximately 1 million additional skilled solar installation workers by 2030 to meet the 600 GW target — a number that dwarfs current apprenticeship intake rates.

National programs are accelerating:

- Germany’s ZVEH (Central Association of Electrical Trades) has expanded solar certification programs and reduced the training duration for qualified electricians adding a solar specialisation from 12 months to 4 months

- France’s QualiSol and Qualifelec certifications have streamlined accreditation for new entrants

- Spain’s IDAE (Institute for Energy Diversification and Saving) runs subsidised solar installation training through regional employment agencies

- Italy’s GSE requires installer certification for grant-funded projects; the certification program was expanded in 2023 to increase throughput

For installers, the skills shortage creates two simultaneous pressures: difficulty hiring qualified staff to scale operations, and pricing power due to limited local supply. In markets with strong mandate-driven demand and constrained installer capacity, margins are materially higher than in saturated markets.

EU Solar Standard

REPowerEU also mandated the development of a harmonised EU Solar Standard — a unified technical specification for rooftop solar installations that would replace the current patchwork of 27 national standards. A unified standard would allow installers to quote cross-border without re-engineering specifications, allow equipment manufacturers to optimise for a single market, and enable cross-border recognition of installer certifications.

Progress has been slow. CENELEC (the European Committee for Electrotechnical Standardisation) published a draft harmonised standard for low-voltage PV systems in 2024. Full adoption requires member state ratification, which is expected to complete by 2027.

Financing Mechanisms: How REPowerEU Solar Gets Funded

The financial architecture supporting REPowerEU solar is multilayered. Understanding which instrument applies to which project type is essential for positioning proposals correctly — and for clients assessing financing options before they commit to installation.

Recovery and Resilience Facility — REPowerEU Chapter

The most significant funding envelope is the REPowerEU chapter added to each member state’s Recovery and Resilience Plan (RRP). This was enabled by Regulation (EU) 2023/435, which allowed member states to amend their existing RRPs to add a dedicated REPowerEU chapter focused on energy independence measures.

The additional funding for the REPowerEU chapters — approximately €20 billion — was sourced primarily from emissions trading system (ETS) revenues, supplemented by existing unallocated RRF loans. Member states submitted their amended RRPs to the Commission for approval; as of end-2024, 18 of 27 member states had approved REPowerEU chapters.

The total RRF envelope across all member states — including both the original recovery chapters and the REPowerEU additions — exceeds €650 billion in grants and loans. Solar energy measures are embedded throughout, not only in the REPowerEU chapter, as solar is also counted toward climate and green transition targets that apply to a minimum 37% of total RRF spending.

For installers and project developers: RRF funds flow through national grant programs, subsidised loan facilities at development banks, and direct public procurement for public building installations. They do not flow directly to private installers without an intervening grant application by the end user (building owner, municipality, housing association).

InvestEU

InvestEU is the EU’s main investment mobilisation instrument for 2021–2027, providing EU budget guarantees to attract private capital into strategic sectors. The Clean Energy window of InvestEU supports:

- Rooftop solar on residential buildings — loans through national promotional banks at preferential rates, typically 50–150 basis points below market

- Commercial rooftop solar — project finance and bond guarantees for portfolios above €10 million

- Solar energy communities — financing for community solar structures that aggregate multiple small producers

InvestEU financing reaches end users through implementing partners — primarily national development banks (KfW in Germany, Cassa Depositi e Prestiti in Italy, ICO in Spain, BPI France) that offer branded loan programs. A homeowner accessing KfW’s solar loan is ultimately drawing on InvestEU guarantee capacity, even if the KfW marketing materials do not reference InvestEU by name.

Innovation Fund

The Innovation Fund — financed through EU ETS revenues — targets innovative low-carbon technologies including advanced PV applications: building-integrated photovoltaics (BIPV), agrivoltaics, floating solar, and co-located solar-storage systems. Innovation Fund grants are competitive and require a minimum project scale of approximately €7.5 million for the general scheme. There is a smaller-scale scheme (below €7.5 million) administered at member state level.

For specialist installers working in BIPV or solar-plus-storage for commercial and industrial clients, Innovation Fund grants can cover 30–60% of capital cost for qualifying projects.

National Development Bank Programs

Beyond EU-level instruments, the national development bank programs are where most installer clients will actually access financing:

Germany — KfW: The KfW 270 Energy Transition Loan offers 10–30 year terms at rates currently running 1.5–2.5% below commercial market rates for rooftop solar. KfW also offers the KfW 294 Home Energy Renovation program for solar combined with insulation and heat pump upgrades.

France — BPI France and ADEME: BPI France provides direct loans and partial guarantees for commercial rooftop solar projects above €500,000. ADEME administers grant programs for public and private building solar; grant rates vary by region and building category.

Italy — Cassa Depositi e Prestiti (CDP): CDP’s energy transition platform provides subsidised loans to municipalities and public entities for public building solar. CDP also co-finances energy service company (ESCo) structures — where the installer retains ownership and sells energy to the building owner — allowing installation without upfront capital from the building owner.

Spain — ICO: The Instituto de Crédito Oficial provides the ICO Empresas y Emprendedores line, which includes an energy efficiency and renewables variant offering 12-year terms for commercial rooftop solar. The ICO facility is accessed through commercial banks, which originate and service the loans under ICO guarantee.

Key Takeaway — Financing as a Sales Tool

The financing options for REPowerEU solar are deeper than most building owners realise. A commercial building owner who believes they need to fund a rooftop solar installation from cash reserves may not know that a subsidised ICO or KfW loan brings the effective financing cost below the return generated by the system — making the project cash-flow positive from day one. Presenting the financing option alongside the technical proposal is one of the most powerful conversions in solar sales. Solar proposal software that integrates financing scenarios alongside generation and savings data makes this a repeatable part of every client conversation.

How the REPowerEU Mandate Creates a Structural Installer Opportunity

The distinction between policy-driven demand and market-driven demand matters for how solar installation businesses should plan. Market-driven demand is cyclical: it responds to electricity prices, incentive availability, and consumer sentiment. Policy-driven demand — demand created by a legal obligation — is more predictable, less elastic to short-term pricing changes, and ultimately non-deferrable.

REPowerEU’s rooftop solar mandate creates exactly this type of demand. From the effective date onward, every building permit application for a qualifying building that does not include solar panel installation is legally non-compliant. Building owners, developers, architects, and municipalities are not choosing whether to install solar — they are choosing who installs it and when.

The Volume Calculation

Estimating the mandate-driven installation volume requires translating building permit statistics into installation demand. The calculation is approximate but directionally clear:

- The EU issues approximately 2.5–3 million building permits per year for commercial, public, and residential new construction combined

- Of these, the public and commercial segments (subject to the 2026/2027 mandatory deadlines) represent roughly 400,000–600,000 permits per year

- A conservative average rooftop system size of 100 kWp per commercial/public building implies 40–60 GW per year of mandate-obligated installation capacity in the commercial/public segment alone

The residential mandate kicks in from 2029. EU residential construction has been running at approximately 1.2–1.5 million new dwelling starts per year. At an average of 5–8 kWp per dwelling, the residential mandate adds a further 6–12 GW per year of policy-obligated demand.

This does not mean all of this will be installed on schedule — permitting delays, grid constraints, and workforce shortages will create backlogs. But it does mean that the demand is structurally guaranteed in a way that voluntary market demand is not.

The Competitive Advantage of Early Positioning

In a mandate-driven market, the businesses that will capture disproportionate market share are those that:

-

Establish public sector procurement relationships before mandates take effect. Municipalities and public agency facilities managers are currently planning their 2026–2027 public building solar programs. Framework agreements and preferred supplier registrations entered now lock in relationships before competitive pressure peaks.

-

Develop commercial developer partnerships. Property developers building new commercial buildings above 250 m² from 2026 need a reliable solar installation partner with experience integrating solar into construction projects — a different service model from retrofit. Developers want a single point of accountability, not a subcontractor who needs to be coordinated.

-

Build permit and financing expertise as a differentiator. The complexity of EU and national funding programs — which combination of RRF grants, InvestEU loans, and national development bank financing applies to a specific building type in a specific country — is overwhelming for most building owners. An installer who can present a complete financing and permitting roadmap alongside a technical proposal is offering a fundamentally different product.

-

Use professional solar design software and solar proposal software to accelerate the sales cycle. In a high-volume mandate-driven market, installers who can generate technically accurate designs and compelling proposals in hours rather than days will win more contracts per sales resource than competitors working on manual processes.

For a comprehensive overview of the financial incentives available across European markets that complement the mandate framework, see our analysis of solar energy policies in Europe and European solar tax credits.

Permit Process Simplification: What Has Changed and What Remains

The REPowerEU permitting reforms represent a genuine shift in regulatory intent, but the distance between regulatory intent and operational reality varies substantially by country and by municipality within countries.

What Has Actually Changed

Statutory timelines. The three-month maximum for rooftop solar permit approval is now law in all member states that have transposed the EPBD revision. This gives installers and project developers a legal basis to follow up, escalate, and — in some cases — deem approved where authorities miss the deadline.

Documentation simplification. Many member states have reduced the documentation required for systems under 10 kWp to a simple notification rather than a full permit application. Germany’s Marktstammdatenregister (MaStR) system allows residential systems below 30 kWp to be registered online in under 30 minutes. France has a similar simplified declaration process for systems under 3 kWp.

Grid connection standardisation. Standard technical requirements for grid connection of systems under 10.8 kW are now harmonised across most member states, eliminating the previously common situation where a DSO would require bespoke technical studies for standard residential installations.

Pre-approved installation zones. Several member states — including Denmark, the Netherlands, and Austria — have designated “go-to zones” for solar development where accelerated permitting applies automatically, without individual assessment. These zones are typically identified through national rooftop suitability mapping.

What Remains Problematic

Municipal variation. Even where national frameworks have been reformed, local implementation is inconsistent. A large German city may process rooftop solar permits in four weeks; a rural municipality in the same Bundesland may take six months. The national three-month rule is legally binding, but enforcement mechanisms are weak.

Heritage and conservation area complexity. Approximately 20–25% of European building stock in older city centres is subject to some form of heritage or conservation designation that can complicate or block solar installation. The EPBD revision includes a requirement to streamline heritage exemption procedures, but most member states have not yet translated this into operational guidance.

Sequential rather than parallel processing. In Italy, Spain, and several Eastern EU states, building permit and grid connection applications are still processed sequentially rather than in parallel. A project cannot submit its grid connection application until the building permit is approved, adding months to total project timelines even when each individual process is within its statutory limit.

DSO response time gaps. DSOs are required to respond to grid connection applications within defined timelines, but capacity constraints — both physical grid capacity and administrative processing capacity — mean that these timelines are frequently missed without the enforcement mechanisms that apply to building permit authorities.

Pro Tip — Parallel Track Permitting

Where national rules allow — and increasingly they do — submit grid connection pre-application documentation in parallel with your building permit application rather than waiting for permit approval first. Even where formal parallel submission is not permitted, establishing early communication with the DSO technical team reduces the clock-start-to-decision gap significantly. Log all DSO communications with timestamps; if the statutory response deadline is missed, a formal written escalation citing the specific regulation often resolves delays within two weeks.

What Installers Should Do Now to Prepare

The REPowerEU mandate implementation timeline creates a specific preparation window. The largest volume of mandate-obligated installations — public buildings and new commercial buildings — comes due between 2026 and 2028. Installers who are positioned to serve this demand by early 2026 will capture a disproportionate share.

1. Qualify for Public Procurement

Public building solar installations above certain value thresholds must go through formal public procurement — EU tender procedures for large projects, simplified national procedures for smaller ones. Qualification requirements typically include:

- Installer certification under national solar standards (QualiSol in France, MCS in the UK, GSE certification in Italy, equivalent in each country)

- Minimum financial standing (turnover, insurance coverage, financial references)

- Track record of comparable projects (number of installations above a certain size, total kWp installed)

- Quality management certification (ISO 9001 in many jurisdictions)

Begin qualification processes now if your firm is not already on public procurement frameworks in the countries where you operate.

2. Develop Relationships with Architects and Developers

The commercial building mandate means solar is no longer an afterthought added during fit-out — it is a design requirement from the first planning application. Architects and structural engineers designing buildings that will require planning permission after January 2026 need to specify solar from concept stage.

Establishing yourself as the recommended solar design partner for a handful of commercial architects or developers creates a pipeline of mandate-obligated projects that flows to you without a competitive tender process for each individual building.

3. Build Financial Proposal Capability

The financing environment is complex, but explaining it clearly is a competitive differentiator. Invest in building internal capability to:

- Identify which EU, national, and regional funding programs apply to a specific building type and location

- Model the financing cost of different structures (outright purchase with grant, subsidised loan, ESCo/PPA)

- Present total cost of ownership and return on investment over a 20-year horizon

Our generation and financial modelling tool is built specifically to support this type of client-facing financial analysis, integrating irradiance data, system output modelling, tariff scenarios, and incentive structures into a single client-ready output.

4. Invest in System Design Quality

The mandate creates volume, but quality is what creates reputation in a newly mandated market. Public bodies and commercial developers commissioning solar installations for the first time are risk-averse. A professionally produced design package — showing shading analysis, structural load assessment, yield simulation, and compliance documentation — signals competence in a way that a simple price quote does not.

Professional solar software with automatic shading analysis, string layout optimisation, and building-integrated design tools allows your firm to produce these packages efficiently. For clients reviewing multiple proposals, the quality of the design documentation is often the differentiating factor.

5. Prepare for Cross-Border Opportunity

The mandate applies across all 27 member states simultaneously. Installers who can operate across borders — whether directly or through sub-contractor networks — have access to demand that country-only firms cannot reach. The harmonised EU Solar Standard (expected to be ratified by 2027) will reduce technical variation across borders; the InvestEU framework supports cross-border project finance structures.

If your firm has capacity to expand geographically, the 2025–2027 window is the time to build those relationships and registrations.

6. Monitor Grid Capacity in Your Target Markets

In the Netherlands and parts of Germany, Italy, and France, grid congestion is already creating de facto installation moratoriums for systems above certain sizes. Before taking on commercial or industrial rooftop projects, verify that grid connection capacity is available in the relevant distribution zone.

DSO grid capacity maps — now legally required to be public — are the starting point. For projects that fall in constrained zones, explore cable pooling (sharing a connection with another asset), battery storage to smooth peak export, or demand-side flexibility agreements with the DSO.

The Bigger Picture: REPowerEU Solar in the EU’s Energy Transition

REPowerEU’s rooftop solar mandate is a significant component of, but not the totality of, the EU’s clean energy transition framework. Understanding how it connects to the broader policy architecture helps installers explain the durability and urgency of the opportunity to clients.

Fit for 55 — the EU’s package of legislation to achieve a 55% reduction in greenhouse gas emissions by 2030 — set the overarching climate target that REPowerEU accelerates. Solar is the single fastest-growing source of clean electricity in the EU and the most cost-effective new generation technology in most EU markets.

The European Green Deal frames the industrial and investment context — solar is part of a broader transition that also includes heat pumps, building renovation, clean transport, and hydrogen production. These adjacent technologies create cross-selling opportunities: building owners making a mandatory solar investment are also candidates for heat pump proposals, EV charging infrastructure, and battery storage.

The Critical Raw Materials Act and Net-Zero Industry Act — both adopted in 2024 — create the regulatory framework for securing solar panel supply chains within the EU. For installers, the immediate implication is that EU procurement specifications increasingly require documentation of supply chain origin, and that panels with EU-manufactured cells may attract preferential treatment in public tenders.

Electricity Market Reform — adopted in 2024 — strengthens the framework for long-term power purchase agreements (PPAs) and contracts for difference (CfDs) that provide revenue certainty for larger commercial and industrial rooftop solar projects. For commercial installers, this creates the contractual foundation for offering multi-year energy supply contracts alongside the hardware installation.

The convergence of these policy instruments creates a durable framework for solar demand that extends well beyond the REPowerEU mandate deadlines. The 300+ GW of rooftop solar targeted by 2030 is the beginning, not the end — the EU’s 2040 and 2050 climate targets require continued solar deployment at scale.

Turn Europe’s Solar Mandate into Your Next Major Project

SurgePV gives solar installers the design, simulation, and proposal tools to win public building and commercial mandate-driven projects across Europe — fast, accurate, and client-ready.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

Frequently Asked Questions

What does REPowerEU require for rooftop solar?

REPowerEU mandates that all new public and commercial buildings over 250 m² must install rooftop solar panels by 2026, all existing public buildings over 250 m² by 2027, and all new residential buildings by 2029. The plan targets over 300 GW of rooftop solar capacity by 2030 as part of the broader 600 GW EU solar target. Member states must transpose these obligations into national building codes and permitting frameworks. Major roof renovations also trigger the installation obligation.

Which EU buildings must have solar panels under REPowerEU?

Under the REPowerEU Solar Rooftop Initiative, mandatory solar panels apply to: all new public buildings over 250 m² from 2026; all existing public buildings over 250 m² from 2027; all new commercial and industrial buildings over 500 m² from 2027; and all new residential buildings from 2029. Exemptions apply for structurally unsuitable rooftops, buildings with insufficient peak sun hours, and heritage-listed structures. Major renovations involving roof replacement also trigger the obligation.

How is REPowerEU solar funded?

REPowerEU solar is funded through the REPowerEU chapter added to national Recovery and Resilience Plans (unlocking €20 billion from emissions trading revenues), the InvestEU programme (EU guarantees channelled through national development banks), the Innovation Fund for advanced applications, and national co-financing through development banks. Residential and commercial installers typically access funding via national grant portals and subsidised loan schemes offered through KfW, BPI France, CDP, ICO, and equivalent institutions.

Which countries are ahead in REPowerEU rooftop solar implementation?

Germany and the Netherlands lead in installed rooftop capacity, with Germany exceeding 820 W per capita and the Netherlands surpassing 1,000 W per capita as of 2024. France leads in mandate breadth, having extended obligations to parking lots and agricultural buildings. Spain and Austria have strong national frameworks. Italy is catching up through PNRR-backed programs but faces permitting complexity. Eastern European states including Poland and Romania lag significantly on both mandate transposition and installed capacity.

What is the EU Solar Energy Strategy?

The EU Solar Energy Strategy, published alongside REPowerEU in May 2022, is the policy framework giving REPowerEU its solar-specific implementation tools. It introduced the Solar Rooftop Initiative with mandatory timelines, the EU Solar PV Industry Alliance to secure European manufacturing, streamlined permitting requiring one-stop-shop approvals within three months, and the Solar Skills Partnership to train the approximately one million additional workers needed by 2030. REPowerEU provides the funding; the Solar Energy Strategy provides the regulatory and industrial architecture.

What is the REPowerEU 600 GW solar target?

REPowerEU set a target of 600 GW of total EU solar PV capacity by 2030, up from approximately 207 GW at end-2022. Over 300 GW of this is expected to come from rooftop installations. The EU had reached approximately 320 GW by end-2024, requiring annual additions of 45–50 GW through 2030. Rooftop solar is the primary vehicle for achieving the target because it uses existing structures, avoids land use conflicts, and connects into existing grid infrastructure.

How does the rooftop solar mandate affect solar installers?

The mandate creates policy-driven demand that is non-deferrable — building owners do not choose whether to install solar, only who installs it and when. This is fundamentally different from voluntary market demand. For installers, the mandate creates a structural opportunity if they position early: qualifying for public procurement frameworks, building relationships with commercial developers, developing financing proposal capability, and investing in professional solar design and proposal software to win at scale in a high-volume market.

What permitting reforms has REPowerEU introduced for solar?

REPowerEU requires member states to establish one-stop-shop permitting for rooftop solar with a maximum three-month approval timeline, silence-is-consent provisions where authorities miss deadlines, simplified notification processes for small systems (typically below 10 kWp), standardised grid connection technical requirements for systems below 10.8 kW, and mandatory public DSO grid capacity maps. Implementation quality varies significantly: France and Austria are most advanced; Italy, Spain, and Eastern EU states have the framework in law but limited operational implementation.