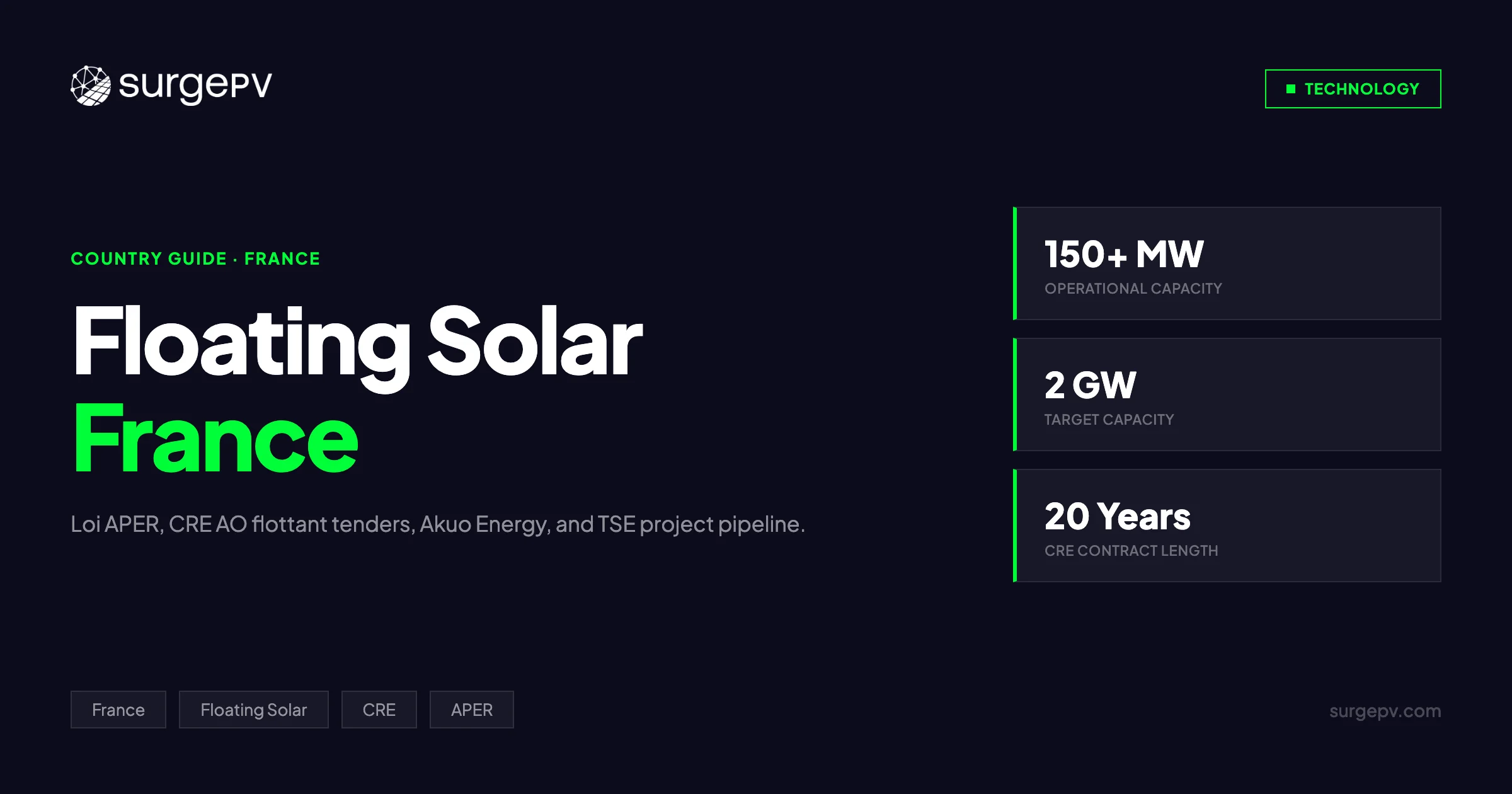

France’s floating solar sector reached an inflection point in 2023–2024. The passage of Loi APER in April 2023 gave floating and agrivoltaic installations an explicit statutory foundation for the first time, replacing an ad hoc permitting patchwork that had frustrated developers for a decade. The CRE (Commission de Régulation de l’Énergie) has since opened dedicated tender windows for flottant and agri-PV projects, and France’s installed floating solar base crossed 150 MW by late 2024 with a pipeline that could reach 2 GW by 2030.

This guide covers the complete market for developers, EPC contractors, and investors working in France’s floating solar market in 2026: the Loi APER regulatory framework, CRE AO tender mechanics, notable operational projects, the permit process for waterways versus reservoirs versus agricultural land, ENEDIS and RTE grid connection procedures, financing structures, French-specific design challenges including mooring regulations, and the forward pipeline.

TL;DR — Floating Solar France 2026

France has 150+ MW of operational floating solar capacity and a CRE-supported pipeline toward 2 GW by 2030. Loi APER (April 2023) created the first explicit legal framework for floating and agrivoltaic installations. CRE tender rounds (AO flottant/agri) award 20-year S17/S21 complément de rémunération contracts. Permitting takes 18–36 months depending on water body type. Leading developers include Akuo Energy, TSE, Urba Energy, EDF Renewables, and Ciel & Terre. Grid connection via ENEDIS (HTA/BT) or RTE (HTB) requires a PTF pre-study before CRE bid submission.

In this guide:

- Latest 2026 updates: CRE tender results, Loi APER implementation status

- The French floating solar regulatory framework: Loi APER 2023, décret agrivoltaïsme

- CRE calls for tenders: AO flottant and agri-PV mechanics, S17/S21 contracts

- Notable French floating solar projects: Urba Energy, Akuo Energy, TSE, EDF Renewables

- Permit process: waterways vs. reservoirs vs. agricultural land

- Grid connection: ENEDIS HTB/HTA procedures and RTE S3REnR obligations

- Financing structures for French floating projects

- Design challenges: mooring regulations, EDF OA tariff legacy, float standards

- Future pipeline and 2030 outlook

Latest Updates: Floating Solar France 2026

For project teams tracking the French flottant market in real time, here is the status as of March 2026.

France’s floating solar policy environment stabilized considerably between 2023 and 2026. Loi APER’s implementing décrets — including the landmark décret agrivoltaïsme published in April 2024 — resolved several interpretive ambiguities that had delayed projects under construction. CRE launched its fifth dedicated floating and agrivoltaic tender window in January 2026, with results expected by Q3 2026.

CRE Tender Results and Active Rounds — March 2026

| CRE Tender Round | Technology | Capacity Awarded | Contract Type | Status |

|---|---|---|---|---|

| AO flottant/agri Round 1 (2022) | Floating + agrivoltaic | 130 MW | S17 CR | Results published; projects in permit stage |

| AO flottant/agri Round 2 (2023) | Floating + agrivoltaic | 200 MW | S17 CR | Projects under permitting/construction |

| AO flottant/agri Round 3 (2024) | Floating + agrivoltaic | 250 MW | S21 CR | Results published Q2 2024 |

| AO flottant/agri Round 4 (2025) | Floating + agrivoltaic | 300 MW | S21 CR | Results published Q1 2025 |

| AO flottant/agri Round 5 (2026) | Floating + agrivoltaic | 350 MW target | S21 CR | Open — results expected Q3 2026 |

CR = complément de rémunération. Source: CRE délibérations, ADEME project registry.

Key Policy and Market Changes Since 2024

Décret agrivoltaïsme operational (April 2024). The implementing decree for the agrivoltaic provisions of Loi APER defines legal criteria separating “agrivoltaïsme” (panels over productive agricultural land with demonstrated agronomic benefit) from “installations agri-compatibles” (ground-mount on less productive ZAIN land). Floating systems on irrigation reservoirs and farm ponds qualify as agrivoltaic if the farmer continues primary agricultural use and a designated agronomist certifies no significant yield reduction.

Zones d’accélération des énergies renouvelables (ZAER) designations underway. Under Loi APER, French communes had until January 2025 to propose ZAER designations. Projects sited within designated ZAER benefit from a presumption of regulatory compatibility — a meaningful advantage for floating proposals on municipal retention basins or industrial water bodies.

CRE S21 contract replaces S17 as standard. From Round 4 onward, CRE switched its floating and agrivoltaic tenders to the S21 complément de rémunération framework, which calculates the premium against a 30-minute market price index rather than the older annual average used under S17. This changes revenue modeling assumptions for post-2025 project finance.

Grid capacity constraints in Occitanie and PACA. France’s saturated HTA grid in southern regions — historically the best for floating solar due to irradiance — has forced some projects to wait for S3REnR (schéma régional de raccordement au réseau des énergies renouvelables) reinforcement works. ENEDIS published updated S3REnR maps in late 2024 showing new HTA capacity openings in Hérault, Gard, and Vaucluse expected by 2027.

Key Takeaway — CRE Timing

CRE Round 5 closes in mid-2026. Projects that have not yet secured a PTF (proposition technique et financière) from ENEDIS or RTE face serious risk of missing the submission window. Grid pre-study requests should be submitted no later than 12 months before the intended CRE bid date. Using solar design software with accurate yield modeling accelerates the technical dossier required for PTF applications.

The French Floating Solar Regulatory Framework

Loi APER 2023: What It Changed

Loi n° 2023-175 du 10 mars 2023 relative à l’accélération de la production d’énergies renouvelables — universally called Loi APER — is the foundational legislative text for floating solar in France. Before its passage, floating PV installations occupied a legal gray zone: they were not explicitly addressed in the Code de l’urbanisme, the Code de l’environnement, or the Code rural et de la pêche maritime, leaving prefectural administrations free to apply contradictory interpretations.

Loi APER resolved this through four key provisions directly affecting floating and agrivoltaic solar:

Article 11 — Statutory recognition of agrivoltaïsme. For the first time, French law defines agrivoltaïsme as “an installation producing electricity from solar radiation on agricultural land, provided that the panels provide a direct benefit to the agricultural activity.” Floating systems on farm irrigation reservoirs explicitly qualify under this definition, provided the farmer demonstrates continued primary agricultural use of the water body.

Article 15 — Simplified environmental authorization for artificial water bodies. Projects on plans d’eau artificiels (artificial water bodies) with no connectivity to natural aquatic ecosystems benefit from a streamlined environmental evaluation procedure. This reduced the standard EIE (évaluation d’impact environnemental) from a full étude d’impact to a simple évaluation préliminaire for qualifying sites.

Article 17 — Zones d’accélération des énergies renouvelables (ZAER). Communes must propose ZAER by deliberation of the conseil municipal. Projects sited within ZAER enjoy a presumption of compatibility with the PLU (plan local d’urbanisme) and reduced risk of mayoral opposition. Water bodies within designated ZAER receive priority treatment in prefectural instruction.

Article 22 — Refus de permis de construire motivated. Prefectural or mayoral refusals of renewable energy permits must now be substantively motivated with reference to specific environmental, heritage, or safety grounds. Blanket refusals citing aesthetic grounds alone are no longer legally sufficient — a significant change that strengthens developer recourse rights.

Le Décret Agrivoltaïsme (April 2024)

The implementing decree published on 9 April 2024 (Décret n° 2024-318) defines the operational criteria for agrivoltaic status:

- Primary use criterion: Agricultural production must remain the “activité principale” of the parcel. For floating systems, this means the water body must continue its primary function (irrigation, aquaculture, flood control).

- Reversibility requirement: Installations must be technically reversible within 18 months of decommissioning. Float systems using ballasted anchoring rather than drilled seabed anchors satisfy this requirement more readily than fixed-foundation ground-mount systems.

- Agronomic certification: An independent agronomist must certify, at installation and every 5 years thereafter, that the installation provides a direct measurable benefit (shade regulation, evaporation reduction, frost protection) or causes no significant yield reduction.

- Maximum ground coverage ratio: For land-based agrivoltaïsme, a 40% maximum coverage ratio applies. For floating systems on agricultural water bodies, the décret establishes a separate maximum surface coverage of 50% of the water body area, provided hydrological and ecological studies confirm this does not materially degrade water quality or aquatic habitat.

Code de l’environnement — Loi sur l’eau

All floating solar installations in France trigger the Loi sur l’eau procedure (articles L.214-1 et suivants of the Code de l’environnement) regardless of agrivoltaic status. The applicable IOTA (installations, ouvrages, travaux et activités) rubric determines whether a projet requires a simple déclaration or a full autorisation environnementale:

- Rubrique 3.1.1.0 (retenues and plans d’eau): Projects on water bodies exceeding 1 hectare require autorisation; smaller bodies require déclaration.

- Rubrique 3.2.5.0 (interventions in the lit mineur of a watercourse): Any floating element anchored within a watercourse bed or flood zone triggers full autorisation regardless of size.

The Agence de l’Eau (one of six regional agencies — Loire-Bretagne, Rhin-Meuse, Seine-Normandie, Rhône-Méditerranée-Corse, Adour-Garonne, Artois-Picardie) must be consulted during instruction. Their advisory opinion is not binding but is heavily weighted by the Préfecture.

Pro Tip — Classifying Your Water Body Early

The single most time-saving action at project inception is obtaining a formal classification opinion from the Agence de l’Eau on whether your target water body is classified as plan d’eau artificiel (fast track) or as connected to the milieu aquatique naturel (full EIE). Misclassification discovered mid-instruction has derailed projects by 12–18 months. Commission this opinion before site control agreements are signed.

Natura 2000 and Protected Species

France has one of Europe’s densest networks of Natura 2000 sites — 1,753 sites covering 12.8% of the national territory. Any floating solar project within or adjacent (generally within 5 km for waterbirds) to a Natura 2000 site must complete an Évaluation des Incidences Natura 2000 (EIN). A negative finding in the EIN does not automatically block the project but requires mitigation measures that must satisfy the DREAL (Direction régionale de l’environnement, de l’aménagement et du logement) before prefectural approval.

Projects in Occitanie and PACA — the regions with highest irradiance — face elevated Natura 2000 exposure due to the Camargue wetland complex and Mediterranean coastal lagoon networks. Developers in these regions routinely commission avifaunal and herpetological surveys 12 months in advance of formal permit submission.

CRE Calls for Tenders: AO Flottant and Agrivoltaic Mechanics

How CRE Tenders Work

The Commission de Régulation de l’Énergie issues periodic appels d’offres (AO) for renewable electricity under authority granted by the Code de l’énergie. For floating and agrivoltaic solar, CRE has run a dedicated tender track — distinct from the standard ground-mount and rooftop AO — since 2022.

The tender award mechanism works as follows:

-

Cahier des charges publication: CRE publishes the call specifications (cahier des charges) defining eligible technologies, minimum and maximum project capacity per lot, required permits, grid connection status, and bidding parameters.

-

Project qualification: Bidders submit technical dossiers demonstrating site control (promesse de bail emphytéotique or equivalent), a grid connection proposal (PTF) from ENEDIS or RTE, and either a permis de construire or evidence of a pending permit application at a defined stage.

-

Price bids: Winning projects are selected on the basis of bid price (€/MWh complément de rémunération) subject to minimum technical qualification scores. Lower bids win subject to not falling below a technical quality threshold on ecological and local integration criteria.

-

Contract award: Winning projects receive a Contrat d’Obligation d’Achat (COA) or Complément de Rémunération (CR) — the S17 or S21 variants — signed with EDF OA (Electricité de France Obligation d’Achat) as the designated obligated purchaser.

-

20-year contract duration: The CR pays a premium over the market reference price for 20 years from commercial operation date (COD). Under S21, the reference price is computed as a 30-minute average of the EPEX SPOT France day-ahead price.

S17 vs. S21 Contract Comparison

| Feature | S17 Complément de Rémunération | S21 Complément de Rémunération |

|---|---|---|

| Market reference price | Annual average EPEX SPOT | 30-minute EPEX SPOT average |

| Cannibalization risk | Low (annual averaging smooths peaks) | Higher (low-price periods reduce premium) |

| Revenue predictability | Higher | Moderate — requires hedging strategy |

| Applicable from | Rounds 1–3 (2022–2023) | Round 4 onward (2025–) |

| Typical bid price range | €55–€75/MWh (floating) | €60–€85/MWh (floating) |

| Merchant tail | None during 20-year term | Same |

The shift to S21 reflects CRE’s intent to expose producers to intraday price signals, incentivizing battery storage co-location and flexible dispatch. For floating-only projects without storage, S21 increases merchant risk and requires more sophisticated revenue modeling during financial close.

Eligibility Requirements for the Floating/Agrivoltaic Tender Track

Not every solar project qualifies for the dedicated floating/agrivoltaic tender. CRE’s cahier des charges specifies:

- Floating systems must be installed on a plan d’eau (lake, reservoir, retention basin, gravel pit) with the float structure covering a minimum of 70% of total installed surface.

- Agrivoltaic systems must meet the criteria of Décret n° 2024-318 — certified agronomic benefit, primary agricultural use maintained, reversibility demonstrated.

- Minimum project capacity: Typically 500 kWp per project for the floating track.

- Maximum project capacity: Set per round — recent rounds have capped individual projects at 30 MWp to maintain portfolio diversity.

- Grid connection: A PTF from ENEDIS or RTE must be in hand or at advanced pre-study stage at bid submission.

Pro Tip — Yield Modeling for CRE Submissions

CRE evaluates bid credibility partly through the P90 yield estimate submitted in the technical dossier. Projects whose P90 production estimates deviate significantly from regional irradiance benchmarks raise questions during qualification review. Using professional solar design software with bifacial modeling, water surface albedo inputs, and validated meteorological datasets strengthens the technical credibility of your CRE dossier.

EDF OA — The Obligated Purchaser

EDF OA (EDF Obligation d’Achat) acts as the contractual off-taker for all CRE-awarded complément de rémunération contracts. The state reimburses EDF OA for the above-market cost of these purchases through the Contribution au Service Public de l’Electricité (CSPE) mechanism collected from electricity consumers.

This structure means that project developers are exposed to EDF OA’s credit risk — which is sovereign-backed and effectively zero for practical financing purposes. Lenders model EDF OA contracts as investment-grade offtake, enabling project-finance structures with senior debt leverage of 70–80% of total project cost.

Notable French Floating Solar Projects

Ciel & Terre — Hydrelio Pioneer Projects

Ciel & Terre, a French company founded in 2006 and headquartered in Lille, invented the Hydrelio floating platform — the world’s most widely deployed proprietary floating PV system. While the company operates globally, France remains a core market. Early Hydrelio deployments on French irrigation reservoirs in Occitanie (2013–2015) established the technical baseline for the French regulatory debate that eventually produced Loi APER.

Ciel & Terre’s French portfolio includes installations on private agricultural reservoirs in Charente-Maritime, Gironde, and Hérault. The Hydrelio system uses HDPE (high-density polyethylene) pontoons with 10–12° tilt, interconnected by stainless steel cables, anchored by polyester mooring lines weighted with concrete clump anchors on the reservoir floor.

Akuo Energy — Guadeloupe and Metropolitan France

Akuo Energy, a Paris-headquartered independent power producer, has been one of the most active floating solar developers in France and its overseas territories. The company’s flagship floating installation on the Rivière-Salée wetlands adjacent to Guadeloupe’s mangrove coast demonstrated the technology in a tropical marine environment — different from metropolitan France but generating regulatory lessons applied to mainland projects.

In metropolitan France, Akuo has secured multiple CRE-awarded contracts for floating projects in the Rhône Valley corridor and in Nouvelle-Aquitaine. The company targets 250 MW of floating and agrivoltaic capacity across Europe by 2030. Akuo’s approach emphasizes ecological co-design: their French floating projects include submerged habitat structures and floating vegetation islands to offset aquatic habitat disruption.

TSE (Transition des Systèmes Energétiques) — Canal and Reservoir Focus

TSE, founded in 2009 and based in Paris, has emerged as one of France’s most prolific agrivoltaic and floating solar developers. TSE’s portfolio leans toward agrivoltaic installations over vine and vegetable crops, but the company has also developed floating systems on agricultural irrigation reservoirs in the Garonne basin.

TSE was among the early winners of the CRE agrivoltaic tender rounds, securing contracts for projects in Occitanie and Centre-Val de Loire. Their floating projects typically range from 1–5 MWp, sized to fit within a single irrigation reservoir footprint and connected to the local ENEDIS HTA network at 20 kV.

Urba Energy — Canopy Systems

Urba Energy, a developer active in the Loire and Bretagne regions, has pioneered a canopy-style floating system deployed primarily on retention basins and municipal water treatment ponds. Unlike fully floating raft systems, Urba Energy’s canopy approach uses fixed-point piling at basin edges to support a partially elevated panel array that shades the water surface while allowing recreational or functional water body use beneath.

This configuration positions Urba Energy’s projects closer to the “agri-compatible” classification in some regulatory interpretations, though the company also pursues full agrivoltaic certification where qualifying agricultural activity can be demonstrated.

EDF Renewables — Piolenc

EDF Renewables’ Piolenc project in Vaucluse (Provence-Alpes-Côte d’Azur) became one of France’s first large-scale floating solar installations and the most-cited case study in policy discussions. Installed on a former gravel extraction pit lake (plan d’eau de carrière) covering approximately 17 hectares, Piolenc reached approximately 17 MWp and demonstrated the economic viability of floating PV on inactive mining water bodies — a category that Loi APER subsequently designated as eligible for simplified permitting.

The Piolenc project generated significant community engagement data. EDF Renewables reported an 82% local approval rate in resident surveys conducted 12 months post-commissioning, attributed to a consultation process that began 24 months before permit submission and included local employment commitments and a community benefit fund.

VSB Energies Nouvelles — Northern France

VSB Energies Nouvelles, a Franco-German developer active across France, has pursued floating solar opportunities in northern France — a region with lower irradiance (1,100–1,300 kWh/m²/year) than the south but significant available water body infrastructure from legacy mining and industrial operations in Hauts-de-France and Grand Est.

Northern projects face a tougher economic case per kWh given lower irradiance, making CRE tender selection critical. VSB has argued that northern floating projects provide complementary generation to the French nuclear base — adding summer peak capacity in regions where nuclear plants along the Rhine and Seine occasionally curtail due to river temperature constraints.

Key Takeaway — Project Scale in France

Most operational French floating solar projects fall in the 1–20 MWp range, constrained by the size of available water bodies and the CRE tender per-project capacity caps. Larger consolidated sites are emerging where multiple adjacent water bodies can be aggregated under a single CRE contract. Accurate multi-body layout optimization using solar design software that handles irregular polygon water surfaces is essential for these aggregated configurations.

Permit Process: Waterways vs. Reservoirs vs. Agricultural Land

The permitting pathway for a French floating solar project depends fundamentally on three variables: the legal classification of the water body, whether the project qualifies as agrivoltaïsme under Décret n° 2024-318, and whether the site falls within a ZAER designated by the commune. These variables interact to produce dramatically different timelines and instruction pathways.

Category 1: Private Artificial Water Bodies (Plans d’eau Artificiels Privés)

Typical examples: Gravel pit lakes, agricultural irrigation reservoirs privately owned, retention basins on industrial property, fish farm ponds.

Regulatory pathway:

- Urbanisme: Permis de construire filed with the commune (instruction 3 months, extendable to 5 months for EIE-requiring projects).

- Loi sur l’eau: Déclaration (for water bodies under 1 ha) or Autorisation environnementale (above 1 ha), filed with the Préfecture DDTM.

- Agence de l’Eau: Consultation during instruction — advisory opinion on hydrological and ecological impact.

- INAO consultation: If the water body is within an AOP (appellation d’origine protégée) agricultural zone, INAO (Institut National de l’Origine et de la Qualité) must be consulted.

Typical timeline: 12–24 months from deposit to permis de construire. Faster if the commune has designated a ZAER covering the site.

Key risks: Recours contentieux (third-party legal challenges to the permit). Neighboring communes or environmental associations may file recours up to 4 months after permit publication. Developers typically wait out the délai de recours before commencing civil works.

Category 2: Public Reservoirs and Retention Basins

Typical examples: EDF/CNR (Compagnie Nationale du Rhône) hydroelectric reservoirs, municipal drinking water reservoirs, SNCF or VNF retention infrastructure.

Regulatory pathway:

- Concession agreement with the public body owning or operating the reservoir (EDF, CNR, the relevant municipal authority). This is often the longest step — EDF and CNR have strategic processes for evaluating third-party solar proposals on their reservoir infrastructure.

- Autorisation environnementale from the Préfecture — full procedure including EIE, public inquiry (enquête publique), and Agence de l’Eau opinion.

- Permis de construire — coordinated with or sequential to autorisation environnementale.

- DGALN/DRIEAT coordination for projects on public water bodies of national interest.

Typical timeline: 24–48 months. The concession negotiation phase alone can take 12–18 months before formal permit instruction begins.

Key risks: Concession terms may require revenue sharing with the host public body, reducing project economics. EDF and CNR both have standard concession templates that allocate 2–5% of annual revenue to the host as land rent equivalent.

Category 3: Public Waterways (Voies Navigables)

Typical examples: Canals managed by VNF (Voies Navigables de France), rivers classified as domaine public fluvial.

Regulatory pathway:

- Authorization from VNF as gestionnaire du domaine public fluvial — a specific administrative authorization process distinct from the standard permitting chain.

- Autorisation d’Occupation Temporaire (AOT) or Convention d’occupation — typically 20 years, renewable, subject to VNF approval of technical specifications.

- Autorisation environnementale — full EIE required; waterway installations almost always classify as having connectivity to natural aquatic ecosystems, triggering the most demanding ecological assessment requirements.

- Navigation impact study — VNF requires demonstration that floating elements do not obstruct navigable passage, create wake hazards for commercial or pleasure navigation, or affect lock operations.

Typical timeline: 30–54 months. Canal-based projects are the most complex floating solar category in France and have historically had the highest abandonment rate at permit stage.

Key risks: Navigation conflict, heritage and landscape objections (many French canals are classified as paysages remarquables), and VNF’s right to terminate the AOT early on public interest grounds with limited developer compensation.

Category 4: Agricultural Land — Agrivoltaïsme Ground and Water

Typical examples: Panels elevated over crops (ground-based agrivoltaic), floating systems on farm irrigation ponds qualifying as agrivoltaïsme under Décret n° 2024-318.

Regulatory pathway:

- SAFER (Société d’Aménagement Foncier et d’Établissement Rural) notification if agricultural land or water body is involved — SAFER has preemption rights on agricultural land sales and may scrutinize long-term bail emphytéotique agreements with developers.

- CDPENAF (Commission Départementale de Préservation des Espaces Naturels, Agricoles et Forestiers) advisory opinion — mandatory for agrivoltaic projects. A negative CDPENAF opinion can be overridden by the Préfet but creates political and legal risk.

- Agronomist certification — independent report confirming primary agricultural use and measurable agronomic benefit, as required by Décret n° 2024-318.

- Permis de construire — with agrivoltaïsme status attached, providing access to the simplified EIE procedure under Loi APER Article 15 where applicable.

Typical timeline: 18–30 months. CDPENAF instruction adds 3–6 months but is predictable in calendar. Projects within ZAER may be fast-tracked.

Key Takeaway — Water Body Classification Is Determinative

The permit pathway — and therefore the project timeline, financing risk, and IRR — is determined primarily by water body classification, not by project size or technology. Commissioning a formal classification opinion from the Agence de l’Eau before entering site control agreements is the most important risk-reduction step a French floating solar developer can take. A misclassified site that enters the wrong permit track loses 12–24 months minimum.

Grid Connection: ENEDIS and RTE Procedures

Network Architecture

French floating solar projects connect to one of two grid operators:

- ENEDIS (Électricité Réseau Distribution France): manages the distribution network at HTA (20 kV, occasionally 63 kV) and BT levels. Projects below approximately 36 MW typically connect through ENEDIS.

- RTE (Réseau de Transport d’Électricité): manages the transmission network at HTB (63 kV, 90 kV, 225 kV, 400 kV). Projects above 36 MW, or projects in areas where HTA capacity is exhausted, connect directly to RTE.

The vast majority of French floating solar projects — given the 1–20 MWp typical range — connect to ENEDIS HTA at 20 kV.

The PTF (Proposition Technique et Financière)

The grid connection process in France begins with a demande de raccordement submitted to ENEDIS or RTE. ENEDIS has a statutory obligation to respond with a PTF within:

- 3 months for simple connections (nearby HTA line with available capacity)

- 6 months for complex connections requiring network reinforcement studies

The PTF specifies:

- The technical connection point (poste source HTA/HTB)

- Required network reinforcement works (travaux d’extension)

- Connection cost allocation between the developer and the network operator (under the tarif de raccordement applicable in the relevant S3REnR zone)

- Construction timeline for network works

The PTF is valid for 6 months. Developers must accept (convention de raccordement) within this window or request a PTF extension. The PTF is a prerequisite for CRE tender submission — CRE will not validate a bid lacking at minimum a pending PTF application.

S3REnR Obligations

France operates a Schéma Régional de Raccordement au Réseau des Énergies Renouvelables (S3REnR) — a regional grid reinforcement plan that allocates connection capacity across renewable energy projects. Under the S3REnR system:

- Projects that connect within reserved S3REnR capacity pay a lower connection cost (shared infrastructure cost pooling).

- Projects that exhaust S3REnR capacity must either wait for the next S3REnR revision (typically every 3–5 years) or pay the full cost of dedicated reinforcement.

Occitanie and PACA — the primary floating solar regions — have the most constrained S3REnR capacity due to the volume of ground-mount solar applications. RTE published updated S3REnR maps for these regions in late 2024, showing new HTA capacity openings expected by 2027 following transformer upgrades at key postes sources in Gard, Hérault, and Var.

Injection Contract and Smart Metering

Once the PTF is accepted and network works are complete, the developer signs a Convention de Raccordement with ENEDIS/RTE and a Contrat d’Injection (CI) covering metering terms, imbalance responsibility, and curtailment protocols. French floating solar projects over 1 MWp are required to participate in the mécanisme d’ajustement — submitting production forecasts to RTE’s balancing market. This requires investment in a SCADA system with RTE-compatible data communication.

Pro Tip — Grid Pre-Study Before Land Acquisition

ENEDIS offers a free preliminary grid study (étude préliminaire de raccordement) for projects at conceptual stage, before formal demande de raccordement. Request this study using the site coordinates and estimated project capacity before signing any land option agreement. The preliminary study reveals whether the nearest poste source has available HTA capacity or is saturated — information that can make or break a site’s economics before significant development costs are committed. Solar design software outputs (peak power, load curve) feed directly into the étude préliminaire request form.

Financing Structure for French Floating Solar Projects

Project Finance Framework

French floating solar projects above approximately 5 MWp typically use non-recourse or limited-recourse project finance. The CRE complément de rémunération contract — effectively a 20-year state-backed off-take — is the foundational bankability element. French lenders (BNP Paribas, Société Générale, Crédit Agricole CIB, and Banque Publique d’Investissement / BpiFrance) are familiar with the CRE CR structure and price floating solar senior debt at margins of 150–250 bps over EURIBOR for investment-grade SPVs.

A typical French floating solar project finance stack looks as follows:

| Tranche | Share of Total Capex | Term | Security |

|---|---|---|---|

| Senior debt (BNP/SG/CA CIB) | 65–75% | 18–20 years | First-ranking pledge on SPV shares, CRE contract assignment, DSRA |

| BpiFrance green loan (optional) | 5–10% | 15 years | Subordinated; BpiFrance takes pari passu position |

| Equity (developer + co-investors) | 15–25% | — | Last-in, first-out |

BpiFrance’s green loan product — targeting renewable energy, energy efficiency, and circular economy projects — provides subordinated lending at below-market rates (typically 80–120 bps below equivalent senior debt pricing) for projects meeting environmental additionality criteria. Floating solar qualifies under BpiFrance’s energy transition priority sector.

CAPEX Structure for Floating Solar in France

French floating solar costs vary by water body type, mooring complexity, and distance to grid connection point. Representative all-in CAPEX ranges for 2025–2026:

| Project Type | CAPEX Range (€/Wp) | Key Drivers |

|---|---|---|

| Simple private reservoir, <5 MWp | €0.90 – €1.15/Wp | Float system + standard mooring + ENEDIS HTA |

| Complex public reservoir, 5–15 MWp | €1.05 – €1.35/Wp | Concession costs, complex anchoring, longer cable runs |

| Canal/navigable waterway | €1.20 – €1.60/Wp | VNF AOT fees, navigation compliance, heritage mitigation |

| Agricultural pond, agrivoltaic | €0.85 – €1.10/Wp | Smaller scale, simpler mooring, partial agri cost sharing |

Float system CAPEX (pontoons, mooring, waterproof interconnects, and onshore inverter shelter) typically represents 25–35% of total project CAPEX, compared to 8–12% for mounting systems on equivalent ground-mount projects. This float premium is partially offset by lower land acquisition cost (water body lease rates are typically lower per hectare than agricultural or industrial land) and by the 12–15% energy yield premium from water-surface cooling.

Revenue Modeling Under S21

Post-Round 4 projects operating under S21 contracts require more sophisticated revenue modeling than the simpler S17 structure:

- Merchant revenue component: During hours when EPEX SPOT France prices exceed the S21 reference price, no premium is paid and the generator receives full market price. During hours below the reference price, the premium tops up the generator to the contracted level (subject to the “clawback” provision that reduces premium payments when annual market prices are high).

- Cannibalization: Floating solar, like all solar, generates predominantly during midday hours — the same hours when French solar output is highest and spot prices are lowest. S21’s 30-minute granularity means floating projects experience cannibalization risk on peak solar production hours.

- Battery co-location: CRE’s AO cahier des charges increasingly incentivizes battery storage co-location through bonus scoring on the technical qualification criteria. A 1–2 hour battery buffer shifts some production to shoulder hours, reducing cannibalization exposure and improving S21 revenue outcomes.

Using solar proposal software that integrates French EPEX SPOT price distributions and S21 contract mechanics allows developers to stress-test project economics across price scenarios before financial close.

Design Challenges for French Floating Solar

Mooring Regulations

France does not have a single national standard for floating solar mooring systems. Mooring design must satisfy three overlapping frameworks:

Loi sur l’eau / IOTA: The autorisation environnementale or déclaration specifies mooring restrictions to protect the water body floor from soil disturbance, sediment resuspension, and contamination from anchor materials. Concrete clump anchors are universally accepted. Drilled helical anchors are accepted for hard substrates with geological certification. Chain anchors are restricted on sites with sensitive benthic habitats identified in the EIE.

Eurocode 1 — Wind Loads: French permis de construire require structural calculations per Eurocode 1 (NF EN 1991-1-4) for wind loading on the float array. Southern French sites in the Rhône Valley corridor must account for Mistral wind events with sustained gusts exceeding 120 km/h. Float systems must demonstrate survival of a 50-year return period wind event without anchor failure or panel loss.

Assurances and guarantees: French insurance markets (AXA, SCOR, Generali France) require mooring system certification by an approved bureau de contrôle (Bureau Veritas or Apave) before issuing operational all-risk policies. Bureau Veritas has developed a specific inspection protocol for floating solar mooring systems published in 2022 — compliance with this protocol significantly simplifies insurance placement.

Float System Standards

No French or European harmonized standard for floating solar pontoon materials and design existed as of 2026. CRE’s cahier des charges references the DNV (Det Norske Veritas) standard DNV-ST-0584 (Design of Floating Solar Power Plants, 2021 edition) as the applicable technical reference. Projects must demonstrate compliance with DNV-ST-0584 or provide an equivalence argument reviewed by an approved tiers-expert.

Key DNV-ST-0584 requirements affecting French project design:

- Material durability: HDPE float components must have a minimum 25-year service life, demonstrated through UV resistance testing to ISO 4892-2.

- Electrical isolation: All submerged electrical components (junction boxes, cable penetrations) must achieve IP68 protection per IEC 60529 with a 1.5-meter depth rating.

- Grounding: The floating array must be bonded and grounded per IEC 60364-7-709 (electrical installations of marinas and similar locations) — the closest applicable IEC standard to floating solar.

Water Surface Albedo and Bifacial Modeling

Floating solar installations on French inland water bodies benefit from water surface albedo, which varies seasonally:

- Clear water on calm days: albedo 0.05–0.07

- Turbid or eutrophic water: albedo 0.03–0.05

- White-painted concrete reservoir walls (common on agricultural ponds): albedo 0.20–0.35 in reflected components reaching bifacial rear surfaces

Bifacial panels — now standard on French floating projects — capture an additional 8–15% rear-side production depending on albedo and tilt angle. At the 10–12° tilt typical of Hydrelio-type platforms, rear-side irradiance is relatively modest. Some developers are trialing 20–25° tilt with alternative pontoon geometries to increase bifacial gain at the cost of higher wind loading.

Accurate bifacial yield modeling requires meteorological datasets that include diffuse horizontal irradiance (DHI) components — not all standard French irradiance datasets (e.g., Météo-France gridded data, PVGIS satellite datasets) provide DHI at the resolution needed for precise bifacial simulation on irregular water body shapes.

EDF OA Legacy Tariff Interactions

Projects that received CRE awards under pre-2022 mechanisms — particularly those operating under the older Tarif d’Obligation d’Achat (T14 or T15 tariffs) issued before the complément de rémunération era — face a different set of operational considerations. Under historic OA tariffs, EDF OA purchases 100% of production at a fixed rate, eliminating merchant revenue but also eliminating cannibalization risk. These legacy tariff projects are fully amortized or approaching end-of-contract and now face a critical question: whether to seek a new CRE CR contract, switch to merchant operation, or add storage and repower.

For legacy OA tariff projects reaching contract end (20 years from commissioning), the typical decision framework considers:

- Remaining module degradation budget (typical annual degradation 0.4–0.5%/year; 20-year-old modules may retain 85–90% original capacity)

- Float system condition (HDPE service life typically extends to 25–30 years if UV oxidation has been within spec)

- New CRE tender eligibility (repowered projects with significantly upgraded modules and invertors can qualify as new projects for CRE purposes)

Key Takeaway — Design Standards Are Converging

The absence of a French national floating solar design standard has been a persistent challenge, but DNV-ST-0584 (2021) combined with CRE’s cahier des charges requirements is functioning as a de facto standard. Bureau Veritas certification to this framework is now effectively mandatory for insurance and lender technical due diligence in France. Design teams using solar proposal software should confirm that their yield modeling tools support DNV-aligned bifacial irradiance inputs and water surface albedo parameterization.

The Floating Solar Design and Simulation Workflow

Floating solar projects in France require a more complex design workflow than standard ground-mount or rooftop systems. The irregular geometry of water body surfaces, variable mooring layouts, bifacial rear-side modeling, and the need to produce CRE-grade P50/P90 yield estimates all impose demands that exceed what basic solar design software tools handle.

A professional floating solar design workflow for a French project typically involves:

-

Site boundary digitization: Drawing the water body polygon from cadastral data (Géoportail / cadastre.gouv.fr) and drone survey, accounting for setback requirements from banks (typically 3–5 meters from water’s edge per local PPRI flood risk plan).

-

Irradiance modeling: Importing Météo-France or PVGIS satellite irradiance data for the site coordinates, with TMY (typical meteorological year) generation. For sites in the Rhône-Alpes or Occitanie regions, local meteorological station data should be cross-validated against satellite datasets to identify orographic shading effects.

-

Layout optimization: Packing the float array within the water body polygon at the chosen inter-row spacing, accounting for CRE maximum 50% water surface coverage limit for agrivoltaic designations and maintaining navigation corridors for maintenance vessels.

-

Bifacial yield simulation: Running hourly bifacial simulation incorporating water surface albedo estimates, pontoon shading on rear cells, and tilt angle sensitivity.

-

P50/P90 estimation: Applying inter-annual variability correction (typically ±5% for French Atlantic-influenced sites, ±4% for Mediterranean-influenced sites) to derive bankable P90 estimates.

-

Electrical design: Sizing inverters, DC string layout across pontoon rows, AC cable routing from the float array to the onshore inverter shelter, and transformer sizing for ENEDIS HTA connection.

Solar software that integrates these steps — from polygon digitization through bankable yield output — reduces design cycle time from weeks to days and produces deliverables formatted for both CRE technical dossiers and ENEDIS PTF applications.

Design French Floating Solar Projects Faster

SurgePV’s solar design tools handle irregular water body geometries, bifacial floating simulation, and bankable P50/P90 output — everything your CRE technical dossier needs.

Book a DemoNo commitment required · 20 minutes · Live project walkthrough

France’s Floating Solar Future Pipeline: 2026–2030

National Targets and the PPE

France’s Programme Pluriannuel de l’Énergie (PPE) — currently under revision for the 2024–2033 period — sets a total solar target of 100 GW by 2050, with an intermediate target of 44 GW by 2028. The PPE does not set a specific floating solar sub-target, but ADEME (Agence de la Transition Écologique) and the Ministry of Energy have cited a 1.5–2 GW floating and agrivoltaic capacity objective by 2030 as consistent with the overall PPE trajectory.

The CRE tender volume trajectory — 130 MW awarded in 2022, rising to 350 MW targeted in 2026 — implies approximately 2 GW of cumulative award capacity by 2028 if the trajectory holds. Not all awarded capacity will reach commercial operation on schedule, as permitting delays and grid connection backlogs typically mean 15–25% of awarded projects slip by 1–2 years.

Priority Regions and Water Body Inventory

ADEME published a preliminary national inventory of water bodies suitable for floating solar in 2023, covering plans d’eau exceeding 1 hectare in area that are not classified within Natura 2000 sites and are not within paysages remarquables zones. The inventory identified:

- ~12,000 ha of private agricultural irrigation reservoirs nationally

- ~8,500 ha of gravel pit and quarry lakes on inactive extraction sites

- ~4,200 ha of industrial retention basins and effluent treatment ponds

- ~2,100 ha of non-navigable canal sections managed by VNF

Applying the CRE 50% maximum coverage ratio to the most accessible category (agricultural irrigation reservoirs), the theoretical maximum floating capacity from this category alone exceeds 3 GW — sufficient to meet the 2030 objective from private reservoirs without requiring the more complex public waterway permit pathway.

Emerging Technologies in France’s Pipeline

Hydro-solar hybrid systems. EDF and CNR are evaluating floating PV installations on their existing large hydroelectric reservoirs — particularly on Lac de Serre-Ponçon (Hautes-Alpes), Lac du Bourget (Savoie), and reservoirs on the Durance and Rhône systems. A hydro-solar hybrid generates complementary production curves: hydro peaks in winter and spring, solar in summer, reducing seasonal imbalance. CNR has issued a call for expressions of interest from floating solar developers for installations on Rhône-managed water bodies.

Agrivoltaic floating for aquaculture. Several pilot projects are exploring floating PV over fish farming ponds in Bretagne and Normandie. Shade from the panels reduces algae proliferation and thermal stress on fish stocks during summer heat events — providing a measurable agronomic benefit that satisfies the Décret n° 2024-318 agrivoltaic certification criteria.

High-concentration floating. Research programs at INRAE (Institut national de recherche pour l’agriculture, l’alimentation et l’environnement) and at CEA-INES in Chambéry are evaluating concentrated PV (CPV) and high-efficiency heterojunction modules on water surfaces. Water cooling enables sustained high-efficiency operation of these temperature-sensitive technologies in a way that ground-mount installations cannot match.

Offshore freshwater floating (large lakes). Preliminary studies are assessing floating solar on Lac Léman (Lake Geneva — shared with Switzerland) and Lac du Bourget, France’s largest natural lake. These large natural water bodies present the most complex ecological and regulatory challenges but also the largest individual site capacity potential (hundreds of MWp per site). Any project on Lac Léman requires bilateral French-Swiss regulatory coordination, which has no precedent in the floating solar sector.

Investment Pipeline

France’s floating solar investment pipeline for 2026–2030 is estimated at €2.5–€4 billion in total project CAPEX, based on the volume of CRE-awarded contracts and projects in advanced permitting. Key investors and developers active across the pipeline include:

- Akuo Energy: Building out CRE Round 2–3 awarded projects, targeting commissioning of 100+ MW in France by 2027.

- TSE: Commissioning first large-scale agrivoltaic floating projects in Occitanie (2026–2027).

- Hydro-Solar (EDF CNR joint venture): Exploring 50–100 MW pilot installations on CNR Rhône reservoirs.

- BayWa r.e.: Active across multiple CRE rounds with mid-size (5–15 MWp) floating projects in Nouvelle-Aquitaine.

- Infrastructure funds: Meridiam, Ardian Infrastructure, and Vauban Infrastructure Partners have all established French renewable energy platforms that include floating solar exposure through equity co-investment in CRE-awarded projects.

Pro Tip — Following the CRE Pipeline

CRE publishes all tender délibérations, results, and award lists on its website (cre.fr). Filtering the délibérations registry by “énergie solaire” and “flottant” gives you real-time visibility into which projects have won contracts, at what price, and in which region. Cross-referencing CRE award data with ENEDIS PTF application volumes (published quarterly in ENEDIS S3REnR reports) gives a leading indicator of where grid congestion is building relative to the floating solar development pipeline.

Related Reading

For further context on the French regulatory and energy market environment:

- France feed-in tariffs and complément de rémunération history

- France’s green energy transition: PPE, SNBC, and sector targets

- Floating solar farms and clean energy: global context

FAQ

Are floating solar farms legal in France?

Yes, floating solar farms are legal in France. The legal framework was consolidated by Loi APER (April 2023), which created explicit authorization pathways for installations on artificial water bodies, irrigation reservoirs, and agricultural land. Projects require permitting from the Préfecture, DDT(M) for land use, and the relevant Agence de l’Eau for water body classification. Natura 2000 sites require full environmental impact assessments, but artificial bodies such as gravel pit lakes, retention basins, and industrial ponds follow a streamlined permit track since 2023.

What is the CRE tender process for floating solar in France?

The Commission de Régulation de l’Énergie (CRE) runs periodic calls for tenders specifically targeting floating and agrivoltaic projects under its AO (appel d’offres) series. Winning projects receive an S17 or S21 complément de rémunération — a market-premium contract valid for 20 years layered on top of electricity market revenues. Floating-specific tender windows have been opened since 2022 with capacity targets rising each round. Projects must secure a permis de construire and ENEDIS/RTE grid connection proposal (PTF) before their CRE submission is fully validated, making early grid pre-study requests critical to meeting bid deadlines.

What is Loi APER and how does it affect floating solar in France?

Loi APER (Loi relative à l’accélération de la production d’énergies renouvelables), enacted in April 2023, is France’s landmark renewable acceleration law. For floating solar, it created statutory recognition of agrivoltaïsme, simplified EIE requirements for installations on artificial water bodies, and required communes to designate renewable acceleration zones (ZAER). Developers on pre-identified zones benefit from a presumption of compatibility with local planning rules, significantly reducing prefectural opposition risk.

How long does permitting take for a floating solar project in France?

Permitting for a floating solar project in France typically takes 18–36 months from initial site identification to permis de construire delivery. The timeline depends heavily on water body classification (private pond vs. public waterway vs. public reservoir), proximity to Natura 2000 zones, and whether the commune has designated a renewable acceleration zone under Loi APER. Projects on artificial bodies classified as private can move faster — sometimes 12–18 months. Public waterway projects overseen by VNF (Voies navigables de France) routinely take 30–48 months.

How does grid connection work for floating solar in France?

Floating solar projects in France connect to the ENEDIS distribution network (HTA at 20 kV) for projects below approximately 36 MW, or to the RTE transmission network (HTB) for larger installations. The process begins with a demande de raccordement, which triggers ENEDIS’s obligation to deliver a PTF (proposition technique et financière) within 3–6 months. The PTF specifies connection costs, network reinforcement works, and timeline. Developers must accept the PTF within 6 months. The PTF is a prerequisite for CRE tender submission — projects without a validated grid connection proposal cannot fully qualify their bid.

Who are the leading floating solar developers in France?

The leading floating solar developers active in France as of 2026 include Akuo Energy (targeting 250 MW across Europe), TSE (Transition des Systèmes Energétiques), Urba Energy, EDF Renewables, VSB Energies Nouvelles, and Ciel & Terre (inventor of the Hydrelio platform). International players such as BayWa r.e. and infrastructure funds including Meridiam and Ardian Infrastructure are also active through equity co-investment in CRE-awarded projects.

What is the 2030 floating solar target for France?

France does not have a statutory standalone floating solar capacity target. However, ADEME and the Ministry of Energy have cited 1.5–2 GW of floating and agrivoltaic capacity by 2030 as consistent with the PPE (Programme Pluriannuel de l’Énergie) overall solar trajectory toward 44 GW by 2028 and 100 GW by 2050. CRE tender volumes — rising from 130 MW in 2022 to 350 MW targeted in 2026 — are the primary policy instrument driving this build-out.